When I was on Wall Street I became very boring by having the same three strong buy recommendations for many years until I downgraded Compaq in 1998 (it was about 30X the original price at that point). The other two, Microsoft and Dell, remained strong recommendations until I left in 2000. At the time, they were each well over 100X the price of my original recommendation. I mention this because my favorite stocks for this blog include Facebook and Tesla for the 4th year in a row. They are both over 5X what I paid for them in 2013 (23 and 45, respectively) and I continue to own both. Will they get to 100X or more? This is not likely, as companies like them have had much higher valuations when going public compared with Microsoft or Dell, but I believe they continue to offer strong upside, as explained below.

In each of my stock picks, I’m expecting the stocks to outperform the market. I don’t have a forecast of how the market will perform, so in a steeply declining market, out-performance might occur with the stock itself being down (but less than the market). Given the recent rise in the market subsequent to the election of Donald Trump, on top of several years of a substantial bull market, this risk is real. While I have had solid success at predicting certain individual stocks’ performance, I do not pride myself in being able to predict the market itself. So, consider yourself forewarned regarding potential market volatility.

This top ten is unusual in having three picks that are negative forecasts as last year there were no negatives and in 2015 only one.

We’ll start with the stock picks (with prices of stocks valid as of writing this post, January 10, all higher than the beginning of the year) and then move on to the remainder of my 10 predictions.

- Tesla stock appreciation will continue to outpace the market (it is currently at $229/share). Tesla expected to ship 50,000 vehicles in the second half of 2016 and Q3 revenue came in at $2.3 billion. This equates to 100,000 vehicles and a $9.2 billion annualized run rate. The model 3 has over 400,000 units on back order and Tesla is ramping capacity to produce 500,000 vehicles in total in 2018. If the company stays on track, from a production point of view, this amounts to 5X the vehicle unit sales rate and about 3X the revenue run rate. While the model 3 is unlikely to have the same gross margins as the current products, tripling revenue should still lead to substantially more than tripling profits. Tesla remains the clear leader in electric vehicles and fully integrated automated features in an automobile. While others are looking towards 2020/2021 to deliver automated cars, Tesla is already delivering most of the functionality required. Between now and 2020 Tesla is likely to install numerous improvements and should remain the leader. Tesla also continues to have the strongest business model as it sells directly to the consumer, eliminating dealers. I also believe that the Solar City acquisition will prove more favorable than anticipated. Given these factors, I expect Tesla stock to have solid outperformance in 2017. The biggest risk is product delay and/or delivering a faulty product, but competitors are trailing by quite a bit so there is some headroom if this happens.

2. Facebook stock appreciation will continue to outpace the market (it is currently at $123/share). While the core Facebook user base growth has slowed considerably, Facebook has a product portfolio that also includes Instagram, WhatsApp and Oculus. This gives Facebook multiple opportunities for revenue growth: Improve the revenue per DAU (daily active user) on Facebook itself; begin to monetize Instagram and WhatsApp in more meaningful ways; and build the install base of Oculus. We have seen Facebook advertising rates increase steadily as more and more mainstream companies shift budget from traditional advertising to Facebook. This, combined with modest growth in DAUs, should lead to continued strong revenue growth from the Facebook platform itself. The opportunity to increase monetization on its other platforms should become more real during 2017, providing Facebook with additional revenue streams. And while the Oculus did not get out of the gate as fast as expected, it is still viewed as the premier product in VR. We believe the company will need to produce a lower priced version to drive sales into the millions of units annually. The wild card here is the “killer app”; if a product becomes a must have and is only available on the Oculus, sales would jump substantially in a short time.

3. Amazon stock appreciation will outpace the market (it is currently at $795/share). I had Amazon as a recommended stock in 2015 but omitted it in 2016 after the stock appreciated 137% in 2015 while revenue grew less than 20%. That meant my 2015 recommendation worked extremely well. But while I still believed in Amazon fundamentals at the beginning of 2016, I felt the stock might have reached a level that needed to be absorbed for a year or so. In fact, 2016 Amazon fundamentals continued to be quite strong with revenue growth accelerating to 26% (to get to this number, I assumed it would have its usual seasonally strong Q4). At the same time, the stock was only up 10% for the year. While it has already appreciated a bit since year end, it seems to be more fairly valued than a year ago, and I am putting it back on our recommended list as we expect it to continue to gain share in retail, have continued success with its cloud offering (strong growth and increased margin), leverage their best in class AI and voice recognition with Echo (see pick 10), and add more physical outlets that drive increased adoption.

4. Both Online and Offline Retailers will increasingly use an Omnichannel Approach. The line between online and offline retailers will become blurred over the next five years. But despite the continued increase in online’s share of the total, physical stores will be the majority of sales for many years. This means that many online retailers will decide to have some form of physical outlets. The most common will be “guide stores” like those from Warby Parker, Bonobos and Tesla where samples of product are in the store but the order is still placed online for subsequent delivery. We believe Amazon may begin to create several such physical locations over the next year or two. I expect brick and mortar retailers to up their game online as they struggle to maintain share. But currently, they continue to struggle to optimize their online presence, so much so that Walmart paid what I believe to be an extremely overpriced valuation for Jet to access better technology and skills. Others may follow suit. One retailer that appears to have done a reasonable job online is William Sonoma.

5. A giant piloted robot will be demo’d as the next form of Entertainment. Since the company producing it, MegaBots, is an Azure portfolio company, this is one of my easier predictions, assuming good execution. The robot will be 16 feet high, weigh 20,000 pounds and be able to lift a car in one hand (a link to the proto-type was in my last post). It will be able to shoot a paint ball at a speed that pierces armor. If all goes well, we will also be able to experience the first combat between two such robots in 2017. Actual giant robots as a new form of entertainment will emerge as a new category over the next few years.

6. Virtual and Augmented reality products will escalate. If 2016 was the big launch year for VR (with every major platform launching), 2017 will be the year where these platforms are more broadly evaluated by millions of consumers. The race to supplement them with a plethora of software applications, follow on devices, VR enabled laptops and 360 degree cameras will escalate the number of VR enabled products on the market. For every high-tech, expensive VR technology platform release, there will be a handful of apps that will expand VR’s reach outside of gaming (and into viewing homes, room design, travel, education etc.), allowing anyone with simple VR glasses connected to a smartphone to experience VR in a variety of settings. For AR, we see 2017 as the year where AR applicability to retail, healthcare, agriculture and manufacturing will start to be tested, and initial use cases will emerge.

7. Magic Leap will disappoint in 2017. Magic Leap has been one of the “aha” stories in technology for the past few years as it promised to build its technology into a pair of glasses that will create virtual objects and blend them with the real world. At the Fortune Brainstorm conference in 2016, I heard CEO Rony Abovitz speak about the technology. I was struck by the fact that there was no demo shown despite the fact that the company had raised about $1.4 billion starting in early 2014 (with a last post-money at $4.5 billion). The problem for this company is that while it may have been conceptually ahead in 2014, others, like Microsoft, now appear further along and it remains unclear when Magic Leap will actually deliver a marketable product.

8. Cable companies will see slide in adoption. Despite many thinking to the contrary, the number of US cable subscribers has barely changed over the past two years, going down from 49.9 million in Q2 2014 to 48.9 million in Q2 2016 (a 2% loss). During the same period, Broadband services subscribers (video on demand for Netflix, Hulu and others) increased about 12% to 57.0 million. Given the extremely high price of cable, more people (especially millennials) are shifting to paying for what they want at considerably less cost so that the rate of erosion of the subscriber base should continue and may even accelerate over the next few years. I expect to see further erosion of traditional TV usage as well, despite the fact that overall media usage per day is rising. The reason for lower TV usage is the shift people are making to consuming media on their smart phones. This shift is much broader than millennials as every age group is increasing their media consumption through their phones.

9. Spotify will either postpone its IPO or have a disappointing one. In theory, valuation of a company should be calculated based on future earnings flows. The problem for evaluating companies that are losing money is that we can only use proxies for such flows and often wind up using them to determine a multiple of revenue that appears appropriate. To do this I first consider gross margin, cost of customer acquisition and operating cost to determine a “theoretic potential operating profit percentage” that a company can reach when it matures. I believe the higher this is, the higher the multiple and similarly the higher the revenue growth rate, the higher the multiple. When I look at Spotify numbers for 2015 (2016 financials won’t be released for several months) it strikes me (and many others) that this is a difficult business to make profitable as gross margins were a thin 16% based on hosting and royalty cost. Sales and marketing (both of which are variable costs that ramp with revenue) was an additional 12.6% leaving only 3.4% before G&A and R&D (which in 2015 were over 13% of revenue). This combination has meant that scaling revenue has not improved earnings. In fact, the 80% increase in revenue over the prior year still led to higher dollars in operating loss (about 9.5% of revenue). Unless the record labels agree to lower royalties substantially (which seems unlikely) its appears that even strong growth would not result in positive operating margins. If I give them the benefit of the doubt and assume they somehow get to 2% positive operating margin, the company’s value ($8 billion post) would still be over 175X this percent of 2015 revenue. If Spotify grew another 50% in 2016, the same calculation would bring the multiple of theoretical 2016 operating margin to about 120X. I believe it will be tough for them to get an IPO valuation as high as their last post if they went public in Q2 of this year as has been rumored.

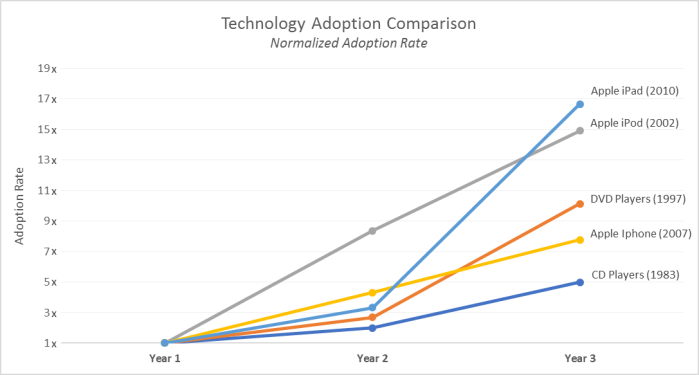

10. Amazon’s Echo will gain considerable traction in 2017. The Echo is Amazon’s voice-enabled device that has built-in artificial intelligence and voice recognition. It has a variety of functions like controlling smart devices, answering questions, telling jokes, playing music through Sonos and other smart devices and more. Essentially an app for it is called a “skill”. There are now over 3,000 of these apps and this is growing at a rapid rate. In the first 12 months of sales, a consulting firm, Activate, estimated that about 4.4 million were sold. If we assume an average price of about $150, this would amount to over $650 million to Amazon. The chart below shows the adoption curve for five popular devices launched in the past. Year 1 unit sales for each is set at 1.0 and subsequent years show the multiple of year 1 volume that occurred in that year. As can be seen from the chart, the second year ranged from 2x to over 8X the first year’s volume and in the third year every one of them was at least 5 times the first year’s volume. Should the Echo continue to ramp in a similar way to these devices, its unit sales could increase by 2-3X in 2017 placing the device sales at $1.5-2.0 billion. But the device itself is only one part of the equation for Amazon as the Echo also facilitates ordering products, and while skills are free today, some future skills could entail payments with Amazon taking a cut.

[…] for drivers of Teslas who deploy Autopilot driver-assistance. Recall that Tesla was one of our stock picks for 2017 and this only reinforces our belief that the stock will continue to […]