Mike Kwatinetz is a Founding General Partner at Azure Capital Partners and a Venture Capitalist investing in application software (SaaS), ecommerce, consumer web and infrastructure technology companies. Successful exits include: Bill Me Later, VMware, TripIt and Top Tier.

A friend called me the other day and inquired as to whether I was ok, as I had not posted in several months. While my goal has been to do about 10 blog posts per year, my frequency has always been erratic, and this year has really been sparse. To make things up, I am going to try for 2 new posts in the next 3 weeks or so that stem from the Azure Marketing Day, held each year for our portfolio companies to gain exposure to advanced techniques across multiple marketing areas. Since the speakers are truly knowledgeable of their arena, using one or two talks as a basis of a post makes me look good!

This post will focus on branding and how to measure whether it is working. The next will delve into direct (snail mail) marketing and how some companies are finding it quite effective.

How to measure the efficacy of brand campaign spend

Spending on branding is quite different than spending for customer acquisition. While many ads serve both purposes, the difference is based on whether there is a direct call for action…usually to buy something. For simplicity, I assume that if there is a call for action, the ad is for customer acquisition, if there is no call for action the ad is for branding.

By improving their brand, a company can experience:

Higher conversion rates on its customer acquisition spend

An increase in the number of people who visit their site

An increase in the LTV (lifetime value) of customers

One method of measuring whether a branding campaign is effective is to determine whether people in the geography where the marketing takes place become more aware of the brand. This is done by measuring the awareness of the brand both before and after the campaign. The most common measure for younger companies is called “Aided Brand Awareness”. Aided brand awareness is determined by conducting a survey of a statistically significant random sample of the population of the geography. In the survey, each person is asked to say which of a list of products/companies they recognize. The percentage that picks the product or company as one they know of is designated as the Aided Brand Awareness. Most TV ads are for improving brand awareness, whereas a large proportion of online ads are for customer acquisition.

While it may seem surprising now, when I was on Wall Street covering Microsoft (and others), Bob Herbold, Microsoft COO, believed a lack of universal brand awareness was limiting the company. So, Microsoft engaged in a significant spend to raise its brand awareness from well below 50% (as I recall) before the campaign. It was one of the many smart strategies the company used to become what they are today. An improved brand helped drive a massive gain in market share for Microsoft productivity applications.

At the Azure Marketing Day, Chris Bruzzo, EVP Marketing and Commercial at Electronic Arts, provided a session on the importance of branding. He outlined one method of testing the potential effectiveness of a branding campaign without breaking the bank. He suggested, if possible, to start by picking matched geographies for a test. You then conduct the branding campaign in the test location and compare results to the control (the second location). By limiting the test to a few geographies, the cost can be kept reasonable while acquiring information on how much impact a branding campaign could have on your company. EA found advertising to improve its brand was quite effective. While I can’t cite EA data due to a public company’s need for confidentiality, I can say it led to higher customer Life Time Value and an increase in the success of customer acquisition campaigns in the test geographies. I have been given permission to review a similar test conducted by Azure portfolio company Chairish.

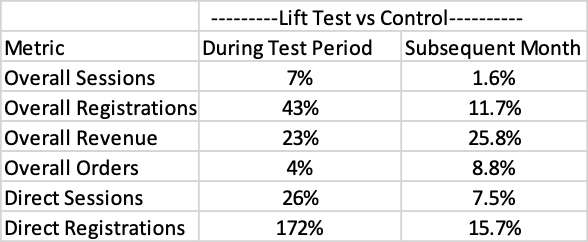

Chairish recently conducted a test of whether spending on branding would prove beneficial. They decided to select 3 cities for the test. For confidentiality, I’ll refer to them as Test Cities 1, 2 and 3. Each was measured against a control city where no branding spend was done. The paired cities, control cities 1, 2 and 3, respectively, each had similar population demographics to the test city it was paired with. The first measurement of benefit was the change in Aided Brand Awareness. Pre-campaign the test cities averaged 6% awareness and the control cities 8%. Post campaign the test cities increased to 13% awareness and the control cities to 9%. So, the lift for the test cities was 7% and for the control cities 1%. I believe that the control cities represented the natural gain the company was getting without a branding campaign, while the branding campaign added an additional 6% of the population to those aware of its brand.

Comparing Test Cities to Control Cities for Branding Campaign

The table shows the average benefit of the marketing campaign across the test cities when compared to their matched control. For example, during the test period the increase in average overall revenue was 23% greater in the test cities than in their paired control locations. A month later, the difference in gain had improved to 25.8%. The reason for such large revenue gains stems from some of the other metrics measured, especially the massive gain in registrations because of the branding campaign.

Given these results, Chairish will be increasing its spend on branding. For those of you who decide to try a branding campaign, it is important to make sure you can measure results. Once the results are in hand, the next step is to compare revenue and gross margin dollar gains to the cost of the campaign. This allows a company conducting a branding campaign to understand the initial incremental cost and the time to recover the investment. Having that in hand allows for a reasonable forecast of the cash flow implications of increasing the spend for branding. One caveat is, while hard to forecast, there is also often the benefit of an increase in customer LTV (life-time value) as greater awareness of the brand also spurs more visits (and spend) from existing customers but this is more difficult to measure in the short run.

While mature companies typically spend a portion of advertising on branding and conduct these types of Aided Brand Awareness measures many younger companies do not consider this. As companies cross the $20-30 million threshold, we believe they should consider experimenting with a brand spend in the manner discussed in this post. Many will find that it is another valuable tool to use as part of marketing spend.

“Much of the public dialogue concerning the economic effect of Covid19 has centered around the large number of people who have lost income, with the conclusion that the US will potentially experience a continued recession going forward. What seems to be lost in the discussion is that the 90% of the labor force that is employed is saving money at an unprecedented rate. This has occurred partly through fear of future loss of income but mostly by a reduction in spending caused by the virus.”

We estimated that consumers would save trillions of incremental dollars if Covid lasted through year end. And that a large portion of it would subsequently be spent on furniture, luxury items, vacations and more. This is now occurring, leading to substantial increased demand for many goods and services and inflationary pressure.

The pressure of this increased spend coupled with continued supply chain issues due to Covid provides the opportunity to keep prices firm (or even increase them) as demand will outstrip supply in many sectors, possibly through year end.

I wanted to start this post by repeating something I discussed in my top ten lists in 2017, 2018 and 2020 which I learned while at Sanford Bernstein in my Wall Street days: “Owning companies that have strong competitive advantages and a great business model in a potentially mega-sized market can create the largest performance gains over time (assuming one is correct).” It does make my stock predictions somewhat boring (as they were on Wall Street where my top picks, Dell and Microsoft each appreciated over 100X over the ten years I was recommending them).

In the seven years we have been offering stock picks on this blog this strategy has worked quite well as the cumulative gains for my picks now exceeds 21X and the 7-year IRR is 55%. The two stocks that have been on the list every year, Tesla and Facebook, were at the end of 2020 at 77X and 11X, respectively, of the price I bought them in mid-2013. They both have been on our recommended list every year since but this is about to change.

In last year’s Top 10 list I pointed out that my target is to produce long-term returns at or above 26%. At that rate one would double their money every 3 years. Since the S&P has had compound growth of 10.88%/year for the past 7 years, and Soundbytes has been at 55%, I thought you might find it interesting to see how long a double takes at various levels of IRR and what multiple you would have after 10 years for each one.

Table: Compound Returns at Various Rates

The wonder of compounding is quite apparent in the table, but it also shows that patience is a virtue as holding the stocks of great companies longer can multiply your money significantly over time, while too many investors become inpatient and sell prematurely. In our last post of 2020 we outlined the thinking process to select great companies, but even great companies can have some periods where their returns are below par. Given that our picks were up an average of 259% last year, I’m back to a fearful mode that 2021 might be that period. Of course, I’m always fearful but sticking with great companies has worked out so far and trying to time when to sell and buy back those companies often leads to sub-optimization.

To some extent, over a 5-year period or longer, stock appreciation is correlated with a company’s growth. So, as I go through each of my 6 stock picks, I will discuss what that might mean for each company. With that in mind, as is my tendency (and was stated in my last post), I am continuing to recommend 5 of the 6 stocks from last year: Tesla, Zoom, Amazon, Stitch Fix and DocuSign. I am removing Facebook from the list and adding CrowdStrike. To be clear, I still believe Facebook will outperform the S&P (see Pick 7 below) but I also believe that over the next few years CrowdStrike and the 5 continuing stocks will experience greater appreciation.

2021 Stock Recommendations:

1. Tesla stock appreciation will continue to outperform the market (it closed last year at $706/share)

Tesla is the one stock in the group that is not trading in synch with revenue growth for a variety of reasons. This means it is likely to continue to be an extremely volatile stock, but it has so many positives in front of it that I believe it wise to continue to own it. The upward trend in units and revenue should be strong in 2021 because, in addition to continued high demand for the model 3:

China Expansion: Tesla continues to ramp up production in China, the world’s largest market. In 2020 the company sold about 120,000 cars (which placed it a dominant number 1 in battery powered cars) there as its Giga Factory in Shanghai ramped up production. Trade Group China Passenger Car Association predicts that Tesla will sell as many as 280,000 vehicles there in 2021…an increase of about 133%. While that is significant growth it only would represent 20% of the number of battery powered vehicles forecast to be sold. The limitation appears to be production as the Shanghai factory is just nearing a volume of 5,000 vehicles per week. Tesla believes it can double that during this year. The Model Y has just been introduced in China and early press is calling it a major hit. Together with the Model 3, I believe this positions Tesla to be supply constrained. Should the company increase production earlier in the year, it has the opportunity to sell more than the forecast 280,000 vehicles. What is also important to note, is Tesla seems to be making greater profits on sales of its cars in China than in the U.S so as China becomes a larger portion of the mix Gross Margin could increase.

European Factory: Tesla has a cost disadvantage in Europe as its cars are not currently built there. So, while it established an early lead in market share, as others have launched battery powered vehicles at lower prices Tesla lost market share. That should all change when its Berlin Giga Factory begins production in July, 2021. This coupled with the Model Y introduction (it will be built in the Berlin factory) should mean a notable increase in sales as Europe returns to more normal times.

Model Y introduction: The Model Y, launched in early 2020 in the U.S., is already selling about 12,000 units a month here. This exceeds sales of crossover vehicles from every major brand (per GCBC which uses VIN reporting to calculate its numbers). It is expected to start being delivered in China in February.

Cybertruck: The Cybertruck (see our graphic here) was introduced to extremely mixed reactions. Traditionalists tended to hate it due to its radical departure from what they have come to expect for a pickup truck from companies like Ford, Toyota, etc. But it rang a cord with many and pre-orders are now up to 650,000 units according to Finbold. To give perspective on what this means, it is 30% higher than the total number of vehicles Tesla sold in 2020. While a portion of these orders could be cancelled as they only required a $100 deposit, the magnitude does imply significant incremental demand when Tesla launches in this category. The launch is expected late this year.

Roadster: Tesla has plans to re-introduce a Roadster in 2021. You may recall that the first Tesla’s were sports cars and are now collectors’ cars mostly valued between $50,000 and $70,000 but now the last one built, having about 200 miles on it is up for sale at $1.5 million. This time around it will make it an ultra-premium vehicle in specifications and in price. The base price Tesla has indicated starts at $200,000. A “Founders Series” will be $50,000 higher (with only 1,000 of those available). At those prices, gross margins should be quite high. The range Tesla initially indicated for this car was 620 miles and the speed from 0 to 60 of 1.9 seconds which would be much quicker than the McLaren 570S gas powered auto.

Tesla Semi: of all the vehicle categories that would benefit from being battery powered I believe the Semi is on top. That is because cost of ownership is one of the highest priorities for vehicles used in commerce. And Tesla claims that their semi will offer the lowest cost of ownership due to economic cost of fuel, less maintenance required as it has fewer parts, and easier repairs. According to Green Car Reports Musk has said it will begin being produced in 2021. Even assuming that Elon’s optimism is off, it appears that it could hit the market in early 2022. Once a definite date and specs are public, sales forecasts for Tesla could rise in 2022.

I’ve taken more time than usual to review my thoughts on Tesla as its astounding stock appreciation in 2020 make it vulnerable to stock pullbacks of some magnitude from time to time. But, its potential to achieve meaningful share of overall auto sales as various geographies shift to battery powered vehicles gives it the potential to achieve high growth in revenue for many years to come.

2. DocuSign stock appreciation will continue to outperform the market (it closed last year at $222/share)

DocuSign is the runaway leader in e-signatures facilitating multiple parties signing documents in a secure, reliable way for board resolutions, mortgages, investment documents, etc. Being the early leader creates a network effect, as hundreds of millions of people are in the DocuSign e-signature database. The company has worked hard to expand its scope of usage for both enterprise and smaller companies by adding software for full life-cycle management of agreements. This includes the process of generating, redlining, and negotiating agreements in a multi-user environment, all under secure conditions. On the small business side, the DocuSign product is called DocuSign Negotiate and is integrated with Salesforce.

DocuSign was another beneficiary of the pandemic as it helped speed the use of eSignature technology. The acceleration boosted revenue growth to 53% YoY in Q3, 2021 (the quarter ended on October 31, 2020) from 39% in Fiscal 2020. Total customers expanded by 46% to 822,000. At the same time Net Retention (dollars spent by year-ago customers in Q3 FY21 vs dollars spent by the same customers a year earlier) was 122% in the quarter. Non-GAAP gross margin remained at 79% as increased usage per customer (due to the pandemic) had minimal impact on cost. Given DocuSign’s strong Contribution Margin, operating profits increase faster than revenue and were up to $49 million from $17 million in the year ago quarter. What has happened represents an acceleration of the migration to eSignature technology which will be the base for DocuSign going forward. Once a company becomes a customer, they are likely to increase their spend, as evidenced by 122% Net Revenue growth. Finally, competition appeared to weaken as its biggest competitor, Adobe, lost considerable ground. This all led to a sizable stock gain of 200% to $222/share at year end. In my view, the primary risk is around valuation but at 50% growth this gets mitigated as earnings should grow much faster than revenue. I continue to believe the stock will appreciate faster than the S&P.

3. Stitch Fix Stock appreciation will continue to outperform the market (it closed last year at $58.72/share)

Stitch Fix offers customers, who are primarily women (although its sales in Men’s clothing is rising), the ability to shop from home by sending them a box with several items selected based on sophisticated analysis of their profile and prior purchases. The customer pays a $20 “styling fee” for the box which can be applied towards purchasing anything in the box. The company is the strong leader in the space with revenue at nearly a $2 billion run rate. The stock had a strong finish to 2020 after declining substantially earlier in the year due to Covid negatively impacting performance. This occurred despite gaining market share as people simply weren’t buying a normal amount of clothes at the onset of the pandemic. When revenue growth rebounded in the October quarter to 10% YoY and 7% sequentially the stock gained significant ground and closed the year up 129%.

Stitch Fix continues to add higher-end brands and to increase its reach into men, plus sizes and kids. Its algorithms to personalize each box of clothes it ships keeps improving. It appears to be beyond the worst days of the pandemic and expects revenue growth to return to a more normal 20-25% for fiscal 2021 (ending in July). This is partially due to easy comps in Q3 and Q4 and partly due to clothing purchase behavior improving. The company will also be a beneficiary of a number of closures of retail stores.

Assuming it is a 20-25% growth company that is slightly profitable, it still appears under-valued at roughly 3X expected Q2 annualized revenue. As a result, I continue to recommend it.

4. Amazon stock will outpace the market (it closed last year at $3257/share).

Amazon shares increased by 76% last year while revenue in Q3 was up 37% year over year (versus 21% in 2019). This meant the stock performance exceeded revenue growth as its multiple of revenue expanded in concert with the increased revenue growth rate. Net Income grew 197% YoY in the quarter as the leverage in Amazon’s model became apparent despite the company continuing to have “above normal” expenditures related to Covid. We expect the company to continue at elevated revenue and earnings growth rates in Q4 and Q1 before reaching comps with last year’s Covid quarters. Once that happens growth will begin to decline towards the 20-25% level in the latter half of 2021.

What will remain in place post-Covid is Amazon’s dominance in retail, leading share in Web Services and control of the book industry. Additionally, Amazon now has a much larger number of customers for its Food Services than prior to the pandemic. All in all, it will likely mean that the company will have another strong year in 2021 with overall growth in the 25-30% range for the year and earnings growing much faster. But remember, the degree earnings grow is completely under Amazon’s control as they often increase spend at faster rates than expected, especially in R&D.

5. Zoom Video Communications will continue to outperform the market (it closed last year at $337/share)

When I began highlighting Zoom in my post on June 24, 2019, it was a relatively unknown company. Now, it is a household name. I’d like to be able to say I predicted that, but it came as a surprise. It was the pandemic that accelerated the move to video conferencing as people wanted more “personal contact” than a normal phone call and businesses found it enhanced communications in a “work at home world”. Let me remind you what I saw in Zoom when I added it to the list last year, while adding some updated comments in bold:

At the time, Revenue retention of business customers with at least 10 employees was about 140%. In Q3, FY 2021 revenue retention of business customers was still 130% despite pandemic caused layoffs.

It acquires customers very efficiently with a payback period of 7 months as the host of a Zoom call invites various people to participate in the call and those who are not already Zoom users can be readily targeted by the company at little cost. Now that Zoom is a household name, acquiring customers should be even less costly.

At the time, Gross Margins were over 80% and I believed they could increase. In Q3, GM had declined to 68% as usage increased dramatically and Zoom made its products available to K-12 schools for free. Given that students were all mostly attending school virtually, this is a major increase in COGs without associated revenue. When the pandemic ends gross margins should return close to historic levels – adding to Zoom profits.

The product has been rated best in class numerous times

Its compression technology (the key ingredient in making video high quality) appears to have a multi-year lead over the competition

Adding to those reasons I noted at the time that ZM was improving earnings and was slightly profitable in its then most recent reported quarter. With the enormous growth Zoom experienced it has moved to significant profitability and multiplied its positive cash flow.

While ZM stock appreciated 369% in 2020, it actually was about equal to its revenue growth rate in Q3 2020, meaning that the price to revenue was the same as a year earlier before despite:

Moving to significant profitability

Becoming a Household name

Having a huge built-in multiplier of earnings as schools re-open

6. CrowdStrike will outperform the market (it closed 2020 at $211/share and is now at 217.93)

When I evaluate companies, one of the first criteria is whether their sector has the wind behind its back. I expect the online security industry to not only grow at an accelerated pace but also face an upheaval as more modern technology will be used to detect increased attacks from those deploying viruses, spam, intrusions and identity theft. I suspect all of you have become increasingly aware of this as virus after virus makes the news and company after company reports “breaches” into their data on customers/users.

The U.S. cyber security market was about $67 billion in 2019 and is forecast to grow to about $111 billion by 2025 (per the Business Research Company’s report). Yet Cloud Security spend remains at only about 1.1% of total Cloud IT spend (per IDC who expects that percent to more than double). CrowdStrike is the player poised to take the most advantage of the shift to the cloud and the accompanying need for best-in-class cloud security. It is the first Cloud-Native Endpoint Security platform. As such it is able to monitor over 4 trillion signals across its base of over 8500 subscription customers. The companies leading technology for modern corporate systems has led to substantial growth (86% YoY in its October quarter). It now counts among its customers 49 of the Fortune 100 and 40 of the top global 100 companies.

Tactically, the company continues to add modules to its suite of products and 61% of its customers pay for 4 or more, driving solid revenue retention. The company targets exceeding 120% of the prior year’s revenue from last year’s cohort of customers. They have succeeded in this for 8 quarters in a row through upselling customers combined with retaining 97% – 98% of them. Because of its cloud approach, growing also has helped gross margins grow from 55% in FY 18 to 66% in FY 19 to 72% in FY 20 and further up to 76% in its most recent quarter. This, combined with substantial improvement in the cost of sales and marketing (as a % of revenue) has in turn led to the company going from a -100% operating margin in Fiscal 2018 to +8% in Q3, FY21. It seems clear to me that the profit percentage will increase dramatically in FY22 given the leverage in its model.

Non-Stock Picks for 2021

7. Online Advertising Companies will Experience a Spike in Growth in the Second Half of 2021

The pandemic hit was devastating for the travel industry, in-person events and associated ticket sellers, brick and mortar retailers and clothing brands. Rational behavior necessitated a dramatic reduction of advertising spend for all those impacted. U.S. advertising revenue declined by 4.3% to $213 billion, or around 17% according to MagnaGlobal, if one excludes the jump in political advertising (discussed in our last post), with Global spend down 7.2%. That firm believes digital formats grew revenue about 1% in 2020 (with TV, radio and print declining more than average). Digital formats would normally be up substantially as they continue to gain share, so the way to think about this is that they experienced 10-20% less revenue than would have occurred without Covid.

Assuming things return to normal in H2 2021, digital advertising will continue to gain share, total industry revenue will be higher than it would have been without Covid (even without the increased political spending in 2020) and comps will be easy ones in H2 of 2021. While there will not be major political spending there could be Olympic games which typically boost ad spend. So, while we removed Facebook from our 6 stock picks, it and other online players should be beneficiaries.

8. Real Estate will Show Surprising Resiliency in 2021

The story lines for Real Estate during the pandemic have been:

The flight to larger outside space has caved urban pricing while driving up suburban values

Commercial real estate pricing (and profits) is collapsing, creating permanent impairment in their value for property owners with post-pandemic demand expected to continue to fall

My son Matthew is a real estate guru who has consulted to cities like New York and Austin, to entities like Burning Man and is also a Professor of Real Estate Economics at NYU. I asked him to share his thoughts on the real estate market.

Both Matthew (quoted below) and I disagree with the story lines. I believe a portion of the thinking regarding commercial real estate pricing relates to the collapse of WeWork. That company, once the darling of the temporary rental space, had a broken IPO followed by a decline in value of nearly 95%. But the truth is that WeWork had a model of committing to long term leases (or purchasing property without regard to obtaining lowest cost possible) and renting monthly. Such a company has extreme risk as it is exposed to downturns in the business cycle where much of their business can disappear. Traditional commercial property owners lease for terms of 5 to 25 years, with 10-15 years being most common, thus reducing or even eliminating that risk as leases tend to be across business cycles. The one area where both Matthew and I do believe real estate could be impacted, at least temporarily, is in Suburban Malls and retail outlets where Covid has already led to acceleration of bankruptcies of retailers a trend I expect to continue (see prediction 10).

The rest of this prediction is a direct quote from Matthew (which I agree with).

“Real estate in 2021 will go down as the year that those who do not study history will be doomed to repeat it. The vastly overblown sentiments of the “death of the city” and the flight to the suburbs of households and firms will be overshadowed by the facts.

In the residential world, while the market for rentals may have somewhat softened, no urban owners have been quick to give up their places, in fact, they turned to rent them even as they buy or rent roomier locations within the city or additional places outside the cities, driving up suburban prices more quickly. In fact, even in markets such as NYC, per square foot housing sale prices are stable or rising. US homebuilding sentiment is the highest in 35 years, with several Y/Y growth statistics breaking decades long records leading up to a recent temporary fizzle due to political turmoil.

The commercial office world, which many decry as imminently bust due to the work at home boom, has seen a slowdown of new leases signed in some areas. But because most commercial office leases are of a 10–15-year term, a single bad year has little effect. While some landlords will give concessions today for an extended term tomorrow, their overall NPV may remain stable or even rise. In the meantime, tech giants like Amazon are gobbling up available space in the Seattle and Bellevue markets, and Facebook announced a 730,000 square foot lease in midtown Manhattan late in the year. In the end, the persistence of cities as clusters of activity that provide productivity advantages to firms and exceptional quality of life, entertainment options, restaurants and mating markets to individuals will not diminish. The story of cities is the story of pandemic after pandemic, each predicting the death of the city and each resulting in a larger, denser, more successful one.

The big story of real estate in 2021 will be the meteoric rise of industrial, which began pre-COVID and was super charged as former in-person sales moved to online and an entire holiday season was run from “dark stores” and warehouses. The continual build out of the last mile supply chain will continue to lower the cost of entry for retailers to accelerate cheaper delivery options. This rising demand for industrial will continue the trend of the creation of “dark stores” which exist solely as shopping locations for couriers, Instacart, Whole Foods and Amazon. Industrial is on the rise and the vaccine distribution problems will only accelerate that in 2021.”

9. Large Brick and Mortar Retailers will continue their downward trend with numerous bankruptcies and acquisitions by PE Firms as consumer behavior has permanently shifted

While bankruptcies are commonplace in the retail world, 2020 saw an acceleration and there was a notable demise of several iconic B&M (Brick & Mortar) brands, including:

It is important to understand that a bankruptcy does not necessarily mean the elimination of the entity, but instead often is a reorganization that allows it to try to survive. Remember many airlines and auto manufacturers went through a bankruptcy process and then returned stronger than before. Often, as part of the process, a PE firm will buy the company out of bankruptcy or buy the brand during the bankruptcy process. For example, JC Penny filed for bankruptcy protection in May, 2020 and was later acquired by the Simon Property Group and Brookfield Property Partners in September, 2020. Nieman Marcus was able to emerge from bankruptcy protection without being acquired. However, in both cases, reorganizing meant closing numerous stores.

There are many who believe things will: “go back to normal” once the pandemic ends. I believe this could not be further from the truth as consumer behavior has been permanently impacted. During the pandemic, 150 million consumers shopped online for the first time and learned that it should now be part of how they buy. But, even more importantly, those who had shopped online previously became much more frequent purchasers as they came to rely on its advantages:

Immediate accessibility to what you want (unlike out of stock issues in Brick and Mortar retail)

Fast and Free shipping in most cases

A more personalized experience than in store purchasing

As older Brick & Mortar brands add online shopping to their distribution strategy, most are unable to offer the same experience as online brands. For example, when you receive a package from Peloton the unboxing experience is an absolute delight, when you receive one from Amazon it is perfectly wrapped. On the other hand, I have bought products online from Nieman Marcus, an extremely high-end retailer, and the clothes seemed to be tossed into the box, were creased and somewhat unappealing when I opened the box. Additionally, a company like Amazon completely understands the importance of customer retention and its support is extraordinary, while those like Best Buy that offer online purchasing fall far of the bar set by Amazon.

What that all means is that many Brick and Mortar retailers will not solve their issues:

Adding more of an online push will not be enough

Customers that have experienced the benefits of online purchasing will continue to use it in much greater amounts than before the pandemic

Ecommerce will continue to take share from Brick and Mortar stores

As a result, we believe that in 2021 the strain on physical retail will continue, resulting in many more well-known (and lesser known) store chains and manufacturing brands filing for bankruptcy as the dual issues of eCommerce and of the pandemic keeping stores closed and/or operating at greatly diminished customer traction throughout most of the year. Coming on the heels of a disastrous 2020 it will be harder for many of them to even emerge from bankruptcy after reorganizing (including closing many stores).

10. The Warriors will make the playoffs this Year

I couldn’t resist including one fun pick. We did speak about this in our last post but wanted to include it as an actual 2021 pick. Many pundits had the Warriors as dead before this season began once Klay Thompson was injured. And, of course, more piled on when the team lost its first 2 games by large margins. But they were mis-analyzing several significant factors:

Steph Curry is still Steph Curry at his peak no matter who the supporting cast

Andrew Wiggins is a superior talent who has the ability to shine on both offense and defense now that he is no longer in a sub-optimal Minnesota environment

Kelly Oubre Jr is also talented enough to be a great defender. His offense, while poor so far, is well above average and over the course of the season that should show well

Draymond Green is in his prime and remains one of the top defenders in the league. He is also a great facilitator on the offensive end of the floor.

James Wiseman is a phenomenon with the talent to be a star. As the season progresses, I expect him to continue to get better and become a major factor in Warrior success

Eric Pascal was on the all-rookie team last year and has gotten better

It is clear that the team needs more games to get Curry and Green back into peak playing condition, Wiseman to gain experience and the Warriors to become acclimated to playing together. They have started to show improved defense but still need time to develop offensive rhythm. I expect them to be a major surprise this year and make the playoffs.

SoundBytes

Please Wear A Mask: I recently read a terrific book describing the 1918 flu pandemic called The Great Influenzaby John Barry. That pandemic was much deadlier than the current one, with estimates of the number of people it killed ranging from 35 million to 100 million when the world population was less than 25% of what it is today. What is so interesting is how much the current situation has replicated the progress of that one. One of the most important conclusions Barry draws from his extensive study of the past is that wearing a mask is a key weapon for reducing the spread.

As hard as it would have been to believe back in the olden days (like in February) my wife and I are now in the 7th week of “Sheltering in Place” and it has just been extended another 4 weeks. The questions constantly being discussed among my colleagues, friends and family are:

How long will this last?

What will life be like at the beginning of the end of this initiative?

When will things go back to normal?

Who will the Warriors draft with their high pick this year (OK not everyone brings this one up)?

I’m not going to try to answer any of these as I’m sure you are all bombarded with potential answers and there are many who know more than I do regarding a pandemic. In this post I’ll try to grapple with 3 different questions, each of which deserves a section below.

Question 1: How will the long-term ramifications of Covid-19 impact success for companies and what can they do to enhance their opportunity?

This is a long-winded question and will get a long-winded answer. To begin, I believe this will only accelerate several trends that are already in place: online commerce gaining share, the use of video conferencing and the virtual workplace, as well as increased emphasis of companies being economically efficient. The pandemic has forced most people to be much more cautious at venturing out to accomplish such everyday tasks as shopping, eating in restaurants and going to the movies. Instead, they are learning that almost everything can be bought online (including food from some top restaurants), conferencing with Zoom provides a great experience at a low cost, and business efficiency will be correlated with survival.

My wife and I have long been online shoppers but as we shelter at home, we have increased the volume of purchases quite significantly. Department stores that were previously experiencing loss of share to online merchants but were resistant to devoting sufficient effort to their own online stores are in deep trouble. It appears likely that a number of well-known and not so well-known retailers will file for bankruptcy within the next few months. The combination of people becoming more comfortable with buying just about everything online and a major reduction in the number of physical outlets will open up more share for online players and for the online stores of multi-channel merchants.

During the current environment my board meetings (as well as everyone else’s) are being held as Zoom conference calls. For many companies, having such a meeting eliminates travel and hotel expenses for employees, board members and advisors. Replacing this with a Zoom conference call can mean lowering the cost to hundreds of dollars, from tens to hundreds of thousands of dollars, per meeting. While I am a big fan of the value of face to face, many companies will be re-evaluating whether having more of their meetings through video conferencing makes sense in an era when the technology has emerged as very viable and extremely cost effective. I’m not suggesting that all board meeting will be executed as video conference calls as face-face remains important, but perhaps companies will decide to do half of their meetings as a Zoom call. An interesting example is the NFL draft, where it was conducted through use of Zoom instead of renting a large stadium and paying for travel expenses. Reviews have suggested that it was actually a better event than the prior year. I suspect the cost savings between all parties involved ran into the millions of dollars.

For many companies the pandemic has weakened revenue, putting pressure on survival. The government “bailout” PPP program helps, but by itself can prove insufficient to prop up companies with weak business models unless they have a very large cash reserve. The investment community was already shifting to focus more on efficient business models prior to Covid-19 but its disruption has helped to highlight the importance of building a profitable business.

Question 2: What should Companies do in the current environment?

What Azure has been suggesting for its portfolio companies is the following series of steps:

If you are eligible, apply for government assistance through the PPP, SBA emergency loan or other programs.

Create multiple models for your business under different scenarios (different dates that people will be back to normal, whether consumer spending will be reduced even after being back, whether customers will delay payments, etc.)

If one or more of credible scenarios indicate that you will run out of cash, then cut costs as quickly as possible. For employees making over $100,000 per year (including founders) cutting them back to some amount that is still at $100,000 or more will have no impact on the forgiveness offered on the PPP loan.

Make every attempt to extend any bank lines coming due as banks have been asked to cooperate with their customers.

If you can afford it, be as kind as possible to your customers by extending terms, etc. Not all, but many, will remember your help and repay you with increased loyalty.

While advertising seems an easy area to cut costs, make sure you evaluate the payback period for customer acquisition marketing as costs may be lower and online conversion may be higher (we have seen that with a number of our companies). In fact, if the payback is reasonably quick it may pay to play offense by being aggressive!

If you have a strong cash position it may be a time to consider acquisitions as many companies will be struggling.

If you have a product that customers are opting to purchase in this environment, think about trying to convert as many as possible to a subscription so that you can extend the relationship beyond the current situation. This can be done by offering attractive discounts for signing up for one or more years rather than month to month. For example, Zoom offers 2 months free if you opt for an annual plan versus a monthly plan. My wife and I decided the cost savings made it worth signing up for a full year.

Question 3: Who are the current and longer-term winners and losers as a result of Covid-19?

Winners

The biggest winners appear to be those that can leverage working at home, educating at home, buying at home, supplying infrastructure for increased online usage, and supplying products for increased cleanliness of surfaces and one’s self. In the public markets, I fortunately have 3 of my annual Blog recommendations included in these categories:

Zoom is the most obvious example of a beneficiary of people working and educating at home. It has reported that daily usage is up an astounding 30X between December and April. Its stock performance is just as astounding, up well over 100% year to date from the time of my pick in early January. The question for the company is whether they can harness this to make us permanently change how we communicate. For my wife and I, the number of Zoom calls we are on is now running between 5 and 10 per week. When I add my business calls the number is quite a bit higher. As they say: “How ya gonna keep ’em down on the farm after they’ve seen Paree?” That is, we are permanent customers as are many of our friends and colleagues.

DocuSign is another of my blog picks that should benefit in both the near term and longer term from the impact of the virus and sheltering at home. Its stock reflects higher expectation as it has increased in value by 41% year-to-date. If more meetings are going to be virtual then more documents will require esignatures and DocuSign is the runaway leader in the category

There are many other pure play beneficiaries of a future where more people entertain themselves, work and educate at home. This includes Netflix (stock up over 25%) who has seen a large spike in usage, Slack (stock up 30% since January 27), and online educational plays (our former company Education.com has seen a large spike in traffic and revenue as has our existing portfolio company Showbie)

Amazon is the poster child for purchasing online. It has announced hiring of 175,000 employees for increased warehouse and logistics operations which Wall Street interpreted as a massive increase in demand driving the stock to new highs (its currently up over 25% YTD). It should also benefit from increased purchases of eBooks and increased online usage of its Web Services (I haven’t seen much chatter about AWS benefit but it should be very large and is highly profitable). Azure portfolio company, Open Road is seeing a significant increase in its sales of eBooks since sheltering-at-home began.

Infrastructure Companies whose revenue varies with web usage should also benefit as volumes are increasing massively: Zoom announced that daily usage is up 3,000%; many others I’ve heard have ranged from 50% to 700% or more. Schools are converting to online classes with student usage increasing to 4-7 hours per day. Gaming companies are also beneficiaries and users. I believe that total web traffic is up at least 50% and perhaps a lot more versus where it would have been.

Clorox is one of the major beneficiaries of our new emphasis on cleanliness through disinfecting our environment and washing our hands many times a day, as recommended by the new folk hero Dr. Fauci. While its stock is up 20% year-to-date, the question is whether the increased demand for disinfectants is a permanent change. I’m guessing that increased usage is permanent… but not to the extent we are seeing today.

Long-Term Losers

Losers span several industries and the question for many of the companies in these industries is how permanent the loss of demand will be. Let’s look at them sector by sector.

Department Stores are currently shut down in most of the United States. Companies already struggling are now experiencing substantial losses every week. Those that have a pharmacy or grocery area (like Walmart) can stay open, but the real key to reducing the losses is the effectiveness of their online offering. In most cases this is pretty weak, both in percentage of the retailer’s sales and the level of profitability given inefficient distribution and high levels of returns. I expect multiple brand name players to file for bankruptcy before the year is over.

The Travel Industry is being hit very hard by the shelter-in-place requirements. Airlines are flying planes that are nearly empty but trying to maintain their cash by not cancelling flights until close to the date of departure so that passengers cancelling will get credits rather than rebates. One hotel I spoke to when cancelling my reservation told me that occupancy was down 90%. Many have already closed their properties. While I expect business to improve greatly for both of these arenas when we are back to normal, they are both accumulating massive losses which might pressure viability. Further, when we are back to normal (whatever that becomes) I suspect that airline traffic will be down through at least mid-2021 as fears are elevated and will take some time to subside. Cruise lines may be in worse shape as the publicity around the various ships that had large portions of passengers and crew get Covid-19 has definitely caused many to reconsider vacationing this way. I expect this sector to be impacted at least through the end of 2021. Also, cruises have had to refund most fares as opposed to providing a credit for future travel.

Arena Entertainment providers and entertainers have been hurt badly by the closure of their venues during this time period. This includes movie theaters as well as complexes like the Chase Center and other arenas. The question becomes when will they be able to be open for full occupancy? And when they are will people stay away for some time. I expect many of them to be at full occupancy by early 2021 as younger people (who make up the majority who attend concerts) will drive renewal of demand for concerts.

Short-term Losers that can Return to Success

Advertising Platforms (TV, Web, etc) have seen demand drop as the travel industry, live events and brick and mortar retailers have little reason to maintain prior spending. Additionally, those companies looking to cut cost view advertising (especially brand building advertising) as a prime candidate for cuts. However, I believe that demand will return to normal as stores reopen and travel is permitted. As of now this appears to be sometime in Q3. While many companies in sectors that take longer to return to normal will still have reduced budgets, online players will likely increase spend, as will those seeing this as an opportunity to gain share.

The Sports Industry consists of teams, leagues, arenas, ticket sellers (like Stubhub), equipment providers and betting. All of these are experiencing close to zero revenue (with the exception of some equipment being sold for home use). Leagues (and teams) with large TV contracts are likely to reinitiate games without live audiences by July as participants can be restricted to those having tested for no virus immediately before a game. Even without an audience the TV money will make this profitable to do. Once these are back in play, betting will resume. Equipment providers can still sell T-shirts and other paraphernalia online, but once games resume their sales will increase. By as early as the fall, but no later than early 2021, I expect that many states will allow live audiences for games and that arenas will be back to normal capacity for them. This would allow ticket sellers and sports betting to be at normal capacity. Equipment suppliers also depend on school purchases as well as little league, etc. So, while revenue will begin growing in the fall it may not be back to normal before early 2021. A noted exception will be providers of at home equipment, like Peloton, which will lose business from gyms in the short run but should see a large increase in at-home purchases.

Non-Internet Service Providers (other than delivery services) have a particularly hard time as physical services cannot be provided online. Things like the Geek Squad, physician checkups and procedures, elective surgeries, automotive services, personal care like haircuts and manicures, massages, and more have been suspended. But as long as the entities survive this period, I believe there will be no permanent impairment of their businesses.

Conclusion

Coming back to where this post began, I’m still wondering who the Warriors will draft! But more importantly, I hope all of you and your families are safe and healthy. We will get through this!

Each year, Azure hosts a marketing day for CMOs and CEOs of its consumer-facing portfolio companies. This year, on February 27th, we had sessions on the following topics:

Refreshing Your Brand as the Business Grows

Metrics for Evaluating Successful Marketing

Leveraging Comedy to Lower Customer Acquisition Cost

Know the Next Generation: An introduction to Gen Z

The Benefits and Drawbacks of a Multi-Channel Strategy

Influencer Strategies

Optimizing Pinterest

I presented the one on Metrics, but the other sessions are conducted by a combination of portfolio executives and outside speakers, each a leading thinker on the topic. Since I invariably learn quite a lot from other speakers, it seems only fair to borrow from their talks for a few blog posts so that I can share these benefits.

Much of this post will be based on concepts that I found especially enlightening from the session by Chris Bruzzo, the current CMO of Electronic Arts, on knowing Generation Z. I won’t cite each place I am using something from Chris versus my own thoughts; but you can assume much of the content emanates from Chris. Since Chris is one of the most creative thinkers in marketing, I’m hoping this will make me look good!

Marketers have Defined Generational Characteristics

Marketers often use personas to help understand what they need to do to address different types of customers. A persona may be:

A married woman 35 years old with a job and 2 children aged 6 and 9;

A 16-year-old male who is a sophomore in high school;

A non-working woman aged 50

A great deal of research has been done on the characteristics of particular “personas” to better enable a company to create and market products that meet their needs. One categorization of people is by age, with 5 different generations being profiled. The youngest group to emerge as important is Gen Z, roughly defined as those born between 1995 and 2012. Currently the U.S. population over 12 years old is distributed as follows:

What this means is that Gen Z has become a significant portion of the population to consider when creating and marketing products. With that in mind, let’s compare several characteristics of the youngest three of these groups.

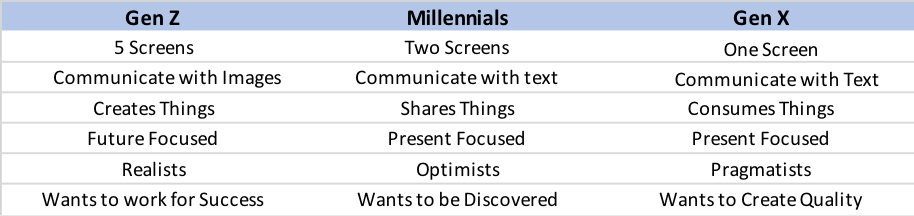

Source: EA Research

Gen Z is the first generation that are digital natives. They are profiled as having cautious optimism, wanting to be connected, seeking community and wanting to create and control things. Earlier generations, including Millennials, watched TV an increasing number of hours, often multi-tasking while they did. Gen Z has replaced much of TV watching with device “screen time”, including visiting YouTube (72% of Gen Z visit it daily). When asked “What device would you pick if you could have only one?”, GenZers chose the TV less than 5% of the time. Prior generations respond well to email marketing while Gen Z needs to be reached through social media. Gen Z has little tolerance for barriers of entry for reaching a site and will just move on (I feel the same way and think many members of other generations do as well). So, when targeting new customers (especially Gen Z) remove barriers to entry like requiring registration before a user becomes a customer. It is important to demonstrate value to them first.

Gen Z grew up in an era where the Internet was part of life and smart phones were viewed as essential… rather than a luxury. On average they spend 40% of their free time on screens. What is even more eye opening is that 91% go to bed with their devices. Advertisers have responded to these trends by gradually shifting more of their spend online. This has been difficult for newspapers and magazines for quite a while, but now it is also having a major impact on flattening out the use of TV as an advertising medium.

There are several implications from the numbers shown in the above chart. First, it is very clear to see that newspapers and magazines as we know them are not viable. This has led to iconic players like the New York Times and Fortune monetizing their brands through conferences, trips, wine clubs, and more. Lesser known brands have simply disappeared. In 2018, TV revenue continued to grow slightly despite losing share as the smaller share was of a larger pie. But in 2019, TV advertising dollars declined, and the decline is forecast to continue going forward. Several factors can be attributed to this but certainly one is that brands targeting Gen Z are aware that TV is not their medium of choice. One unintended consequence of major brands shifting spend to the Internet is that because they are less price sensitive to cost than eCommerce companies, this has led to higher pricing by Facebook and Google.

Personalization is Becoming “Table Stakes” and Offering Co-Creation is a Major Plus

Consumers, in general, and especially Gen Z, are demanding that brands do more to personalize products to their needs and interests. In fact, Gen Z even wants to participate in product creation. One example involves Azure portfolio company Le Tote. The company, much like Stitch Fix, uses algorithms to personalize the clothing it sends based on specifics about each customer. When the company added the ability for consumers to personalize their box (from the already personalized box suggested by the algorithm) there was a sizeable spike in satisfaction…despite the fact that the items the consumer substituted led to a decline in how well the clothes fit! This example shows that using customer data to select new items is only a first step in personalization. Letting the customer have more of a say (be a co-creator) is even more important.

Conclusions

Startups need to diversify their marketing spend away from Facebook and Google as the ROI on these channels has contracted. At the Azure marketing day, we highlighted testing whether Pinterest, influencers, brick and mortar distribution and/or comedy might be sources that drive a higher ROI.

If Gen Zers are being targeted, YouTube, Snap, Instagram, and Twitch are likely better places to market

When targeting new customers (especially Gen Z) remove barriers to entry like requiring registration before a user becomes a customer. It is important to demonstrate value to them first.

Build great apps for iPhones and Android phones but what is becoming most important is making sure that smart phones work well on your site without requiring an app, as most Gen Zers will use their phones for access. When they do, the mobile web version needs to be strong so that they don’t need to download your app before discovering the value you offer.

Involve customers as much as possible in the design/selection/creation of your products as this extends personalization to “co-creation” and will increase satisfaction.

Soundbytes

Readers are aware that I invest in growth stocks (some of which I suggest to you) to achieve superior performance. What you may not be aware of is that over the past 25 years my strategy for investing has been to put the majority of capital in A or better rated municipal bonds (Munis) to generate income in a relatively safe way (and I believe everyone should diversify how they apportion capital). I use a complex strategy to generate superior returns and in the past 25 years I have earned, on average, between 4% and 5% tax free annually. But in the current environment new investments in Munis will have much lower yields so I have started to look at “safe” alternatives to generate income. This type of investment is for income generation and involves a different category of stocks than the growth stocks I target for high returns through stock appreciation.

Given the recent downturn in the stock market I did my first “bond alternative” investment earlier this week. My goal is to generate income of over 5% on an after-tax basis in stocks that are “safe” investments from the point of view of continuing to deliver dividends at or above current levels.

My first set of transactions was in Bristol Myers Squibb:

I bought the stock at $56.48 where the dividend is 3.2% per year

I sold Jan 21 calls at a strike price of 60 and received $4.95

If the stock is not called my cash yield, including $1.80 in dividends, would be $6.75 over less than one year which would equal 12% before taxes

I also sold Jan 21 puts at a strike price of $55 and received $6.46. If the stock is not put to me and is not called that would increase my one-year yield to over 23% of the $56.48 stock price and I would repeat the sale of calls and puts next year. Since my net cost was $43.27 the percentage yield would be over 30% of my cash outlay.

If the stock was called my net gain would equal the profit on the stock, the dividends for one year plus the premiums on the options and would exceed 30%

If the stock went below $55 and was put to me at that price I would be ok with that as the new shares would have a net cost of just over $49 with a dividend yield of close to 4.0% (assuming the company follows past practice of raising dividends each year) and I could sell new puts at a lower strike price.

The second stock I invested in for income is AT&T.

I bought the stock at $34.60 where the dividend is 6.0% per year

I sold Jan 21 calls at a strike price of $37 and received $2.05 per share

If the stock is not called my year 1 cash yield would be $4.13 per share over less than a year or about 12% before taxes

I also sold Jan 21 puts with a strike of $32 and received $3.30 per share. If the stock is not put to me and is not called, that would increase my one-year yield to over 20% of the stock price and over 25% of the net cash outlay

If the stock was called, I would only have 3 quarters of dividends, but the gain would be over 30% of my net original cash outlay

If the stock was put to me my cost of the new shares, after subtracting the put premium would be $28.70 and the dividend alone would provide a 7.2% pre-tax yield and I could sell new puts at a lower price.

We shall see how this works out but unless they cut the dividends, I won’t worry if the stock is lower a year from now as that would only increase my yield on new stock purchased due to the puts. The chance of either company cutting dividends seems quite low which is why I view this as a “safe” alternative to generate income as I won’t sell either stock unless they are called at the higher strike price.

I also began reserving capital starting about a month ago as I expected the virus to impact the market. These purchases used about 10% of what I had put aside. I put another 15% to work on Friday, March 13 as the market had fallen further and valuations have become quite attractive – remember the secret is to “buy low, sell high”. When the market is low its always scary or it wouldn’t be low! I do confess that I didn’t sell much when it was high as I tend to be a long-term holder of stocks I view as game changers…so I missed the opportunity to sell high and then repurchase low.

I wanted to start this post by repeating something I discussed in my top ten lists in 2017 and 2018 which I learned while at Sanford Bernstein in my Wall Street days: “Owning companies that have strong competitive advantages and a great business model in a potentially mega-sized market can create the largest performance gains over time (assuming one is correct).” It does make my stock predictions somewhat boring (as they were on Wall Street where my top picks, Dell and Microsoft each appreciated over 100X over the ten years I was recommending them).

Let’s do a little simple math. Suppose one can generate an IRR of 26% per year (my target is to be over 25%) over a long period of time. The wonder of compounding is that at 26% per year your assets will double every 3 years. In 6 years, this would mean 4X your original investment dollars and in 12 years the result would be 16X. For comparison purposes, at 5% per year your assets would only be 1.8X in 12 years and at 10% IRR 3.1X. While 25%+ IRR represents very high performance, I have been fortunate enough to consistently exceed it (but always am worried that it can’t keep up)! For my recommendations of the past 6 years, the IRR is 34.8% and since this exceeds 26%, the 6-year performance is roughly 6X rather than 4X.

What is the trick to achieving 25% plus IRR? Here are a few of my basic rules:

Start with companies growing revenue 20% or more, where those closer to 20% also have opportunity to expand income faster than revenue

Make sure the market they are attacking is large enough to support continued high growth for at least 5 years forward

Stay away from companies that don’t have profitability in sight as companies eventually should trade at a multiple of earnings.

Only choose companies with competitive advantages in their space

Re-evaluate your choices periodically but don’t be consumed by short term movement

As I go through each of my 6 stock picks I have also considered where the stock currently trades relative to its growth and other performance metrics. With that in mind, as is my tendency (and was stated in my last post), I am continuing to recommend Tesla, Facebook, Amazon, Stitch Fix and DocuSign. I am adding Zoom Video Communications (ZM) to the list. For Zoom and Amazon I will recommend a more complex transaction to achieve my target return.

2020 Stock Recommendations:

1. Tesla stock appreciation will continue to outperform the market (it closed last year at $418/share)

Tesla is likely to continue to be a volatile stock, but it has so many positives in front of it that I believe it wise to continue to own it. The upward trend in units and revenue should be strong in 2020 because:

The model 3 continues to be one of the most attractive cars on the market. Electric Car Reviews has come out with a report stating that Model 3 cost of ownership not only blows away the Audi AS but is also lower than a Toyota Camry! The analysis is that the 5-year cost of ownership of the Tesla is $0.46 per mile while the Audi AS comes in 70% higher at $0.80 per mile. While Audi being more expensive is no surprise, what is shocking is how much more expensive it is. The report also determined that Toyota Camry has a higher cost as well ($0.49/mile)! Given the fact that the Tesla is a luxury vehicle and the Camry is far from that, why would anyone with this knowledge decide to buy a low-end car like a Camry over a Model 3 when the Camry costs more to own? What gets the Tesla to a lower cost than the Camry is much lower fuel cost, virtually no maintenance cost and high resale value. While the Camry purchase price is lower, these factors more than make up for the initial price difference

China, the largest market for electronic vehicles, is about to take off in sales. With the new production facility in China going live, Tesla will be able to significantly increase production in 2020 and will benefit from the car no longer being subject to import duties in China.

European demand for Teslas is increasing dramatically. With its Chinese plant going live, Tesla will be able to partly meet European demand which could be as high as the U.S. in the future. The company is building another factory in Europe in anticipation. The earliest indicator of just how much market share Tesla can reach has occurred in Norway where electric cars receive numerous incentives. Tesla is now the best selling car in that country and demand for electric cars there now exceeds gas driven vehicles.

While 2020 is shaping up as a stairstep uptick in sales for Tesla given increased capacity and demand, various factors augur continued growth well beyond 2020. For example, Tesla is only partway towards having a full lineup of vehicles. In the future it will add:

Pickup trucks – where pre-orders and recent surveys indicate it will acquire 10-20% of that market

A lower priced SUV – at Model 3 type pricing this will be attacking a much larger market than the Model X

A sports car – early specifications indicate that it could rival Ferrari in performance but at pricing more like a Porsche

A refreshed version of the Model S

A semi – where the lower cost of fuel and maintenance could mean strong market share.

2. Facebook stock appreciation will continue to outperform the market (it closed last year at $205/share)

Facebook, like Tesla, continues to have a great deal of controversy surrounding it and therefore may sometimes have price drops that its financial metrics do not warrant. This was the case in 2018 when the stock dropped 28% in value during that year. While 2019 partly recovered from what I believe was an excessive reaction, it’s important to note that the 2019 year-end price of $205/share was only 16% higher than at the end of 2017 while trailing revenue will have grown by about 75% in the 2-year period. The EPS run rate should be up in a similar way after a few quarters of lower earnings in early 2019. My point is that the stock remains at a low price given its metrics. I expect Q4 to be quite strong and believe 2020 will continue to show solid growth.

The Facebook platform is still increasing the number of active users, albeit by only about 5%-6%. Additionally, Facebook continues to increase inventory utilization and pricing. In fact, given what I anticipate will be added advertising spend due to the heated elections for president, senate seats, governorships etc., Facebook advertising inventory usage and rates could increase faster (see prediction 7 on election spending).

Facebook should also benefit by an acceleration of commerce and increased monetization of advertising on Instagram. Facebook started monetizing that platform in 2017 and Instagram revenue has been growing exponentially and is likely to close out 2019 at well over $10 billion. A wild card for growth is potential monetization of WhatsApp. That platform now has over 1.5 billion active users with over 300 million active every day. It appears close to beginning monetization.

The factors discussed could enable Facebook to continue to grow revenue at 20% – 30% annually for another 3-5 years making it a sound longer term investment.

3. DocuSign stock appreciation will continue to outperform the market (it closed last year at $74/share)

DocuSign is the runaway leader in e-signatures facilitating multiple parties signing documents in a secure, reliable way for board resolutions, mortgages, investment documents, etc. Being the early leader creates a network effect, as hundreds of millions of people are in the DocuSign e-signature database. The company has worked hard to expand its scope of usage for both enterprise and smaller companies by adding software for full life-cycle management of agreements. This includes the process of generating, redlining, and negotiating agreements in a multi-user environment, all under secure conditions. On the small business side, the DocuSign product is called DocuSign Negotiate and is integrated with Salesforce.

The company is a SaaS company with a stable revenue base of over 560,000 customers at the end of October, up well over 20% from a year earlier. Its strategy is one of land and expand with revenue from existing customers increasing each year leading to a roughly 40% year over year revenue increase in the most recent quarter (fiscal Q3). SaaS products account for over 95% of revenue with professional services providing the rest. As a SaaS company, gross margins are high at 79% (on a non-GAAP basis).

The company has now reached positive earnings on a non-GAAP basis of $0.11/share versus $0.00 a year ago. I use non-GAAP as GAAP financials distort actual results by creating extra cost on the P&L if the company’s stock appreciates. These costs are theoretic rather than real.

My only concern with this recommendation is that the stock has had a 72% runup in 2019 but given its growth, move to positive earnings and the fact that SaaS companies trade at higher multiples of revenue than others I still believe it can outperform this year.

4. Stitch Fix Stock appreciation will continue to outperform the market (it closed last year at $25.66/share)

Stitch Fix offers customers, who are primarily women, the ability to shop from home by sending them a box with several items selected based on sophisticated analysis of her profile and prior purchases. The customer pays a $20 “styling fee” for the box which can be applied towards purchasing anything in the box. The company is the strong leader in the space with revenue approaching a $2 billion run rate. Unlike many of the recent IPO companies, it has shown an ability to balance growth and earnings. The stock had a strong 2019 ending the year at $25.66 per share up 51% over the 2018 closing price. Despite this, our valuation methodology continues to show it to be substantially under valued and it remains one of my picks for 2020. The likely cause of what I believe is a low valuation is a fear of Amazon making it difficult for Stitch Fix to succeed. As the company gets larger this fear should recede helping the multiple to expand.

Stitch Fix continues to add higher-end brands and to increase its reach into men, plus sizes and kids. Its algorithms to personalize each box of clothes it ships keeps improving. Therefore, the company can spend less on acquiring new customers as it has increased its ability to get existing customers to spend more and come back more often. Stitch Fix can continue to grow its revenue from women in the U.S. with expansion opportunities in international markets over time. I believe the company can continue to grow by roughly 20% or more in 2020 and beyond.

Stitch Fix revenue growth (of over 21% in the latest reported quarter) comes from a combination of increasing the number of active clients by 17% to 3.4 million, coupled with driving higher revenue per active client. The company accomplished this while generating profits on a non-GAAP basis.

5. Amazon stock strategy will outpace the market (it closed last year at $1848/share).

Amazon shares increased by 23% last year while revenue in Q3 was up 24% year over year. This meant the stock performance mirrored revenue growth. Growth in the core commerce business has slowed but Amazon’s cloud and echo/Alexa businesses are strong enough to help the company maintain roughly 20% growth in 2020. The company continues to invest heavily in R&D with a push to create automated retail stores one of its latest initiatives. If that proves successful, Amazon can greatly expand its physical presence and potentially increase growth through the rollout of numerous brick and mortar locations. But at its current size, it will be difficult for the company to maintain over 20% revenue growth for many years (excluding acquisitions) so I am suggesting a more complex investment in this stock:

Buy X shares of the stock (or keep the ones you have)

Sell Amazon puts for the same number of shares with the puts expiring on January 15, 2021 and having a strike price of $1750. The most recent sale of these puts was for over $126

So, net out of pocket cost would be reduced to $1722

A 20% increase in the stock price (roughly Amazon’s growth rate) would mean 29% growth in value since the puts would expire worthless

If the stock declined 226 points the option sale would be a break-even. Any decline beyond that and you would lose additional dollars.

If the options still have a premium on December 31, I will measure their value on January 15, 2021 for the purposes of performance.

6. I’m adding Zoom Video Communications to the list but with an even more complex investment strategy (the stock is currently at $72.20)

I discussed Zoom Video Communications (ZM) in my post on June 24, 2019. In that post I described the reasons I liked Zoom for the long term:

Revenue retention of a cohort was about 140%

It acquires customers very efficiently with a payback period of 7 months as the host of a Zoom call invites various people to participate in the call and those who are not already Zoom users can be readily targeted by the company at little cost

Gross Margins are over 80% and could increase

The product has been rated best in class numerous times

Its compression technology (the key ingredient in making video high quality) appears to have a multi-year lead over the competition

Adding to those reasons it’s important to note that ZM is improving earnings and was slightly profitable in its most recent reported quarter

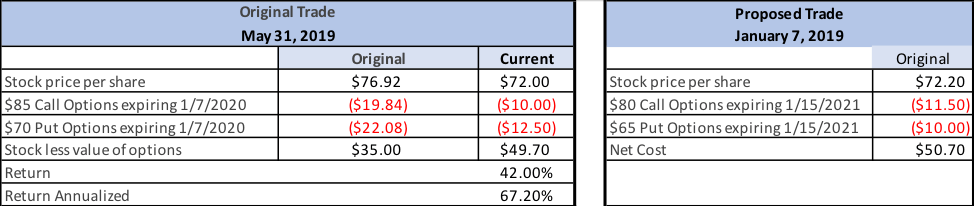

The fly in the ointment was that my valuation technology showed that it was overvalued. However, I came up with a way of “future pricing” the stock. Since I expected revenue to grow by about 150% over the next 7 quarters (at the time it was growing over 100% year over year) “future pricing” would make it an attractive stock. This was possible due to the extremely high premiums for options in the stock. So far that call is working out. Despite the company growing revenue in the 3 quarters subsequent to my post by over 57%, my concern about valuation has proven correct and the stock has declined from $76.92 to $72.20. If I closed out the position today by selling the stock and buying back the options (see Table 1) my return for less than 7.5 months would be a 42% profit. This has occurred despite the stock declining slightly due to shrinkage in the premiums.

Table 1: Previous Zoom trade and proposed trade

I typically prefer using longer term options for doing this type of trade as revenue growth of this magnitude should eventually cause the stock to rise, plus the premiums on options that are further out are much higher, reducing the risk profile, but I will construct this trade so that the options expire on January 15, 2021 to be able to evaluate it in one year. In measuring my performance we’ll use the closing stock price on the option expiration date, January 15, 2021 since premiums in options persist until their expiration date so the extra 2 weeks leads to better optimization of the trade.

So, here is the proposed trade (see table 1):

Buy X shares of the stock at $72.20 (today’s price)

Sell Calls for X shares expiring January 15, 2021 at a strike of $80/share for $11.50 (same as last price it traded)

Sell puts for X shares expiring January 15, 2021 with strike of $65/share for $10.00 (same as last price it traded)

I expect revenue growth of 60% or more 4 quarters out. I also expect the stock to rise some portion of that, as it is now closer to its value than when I did the earlier transaction on May 31, 2019. Check my prior post for further analysis on Zoom, but here are 3 cases that matter at December 31, 2020:

Stock closes over $80/share (up 11% or more) at end of the year: the profit would be 58% of the net cost of the transaction

This would happen because the stock would be called, and you would get $80/share

The put would expire worthless

Since you paid a net cost of $50.70, net profit would be $29.30

Stock closes flat at $72.20: your profit would be $21.50 (42%)

The put and the call would each expire worthless, so you would earn the original premiums you received when you sold them

The stock would be worth the same as what you paid

Stock closes at $57.85 on December 31: you would be at break even. If it closed lower, then losses would accumulate twice as quickly:

The put holder would require you to buy the stock at the put exercise price of $65, $7.15 more than it would be worth

The call would expire worthless