In our October, 2015 Soundbytes (https://soundbytes2.com/2015/10/) I predicted that Omnichannel selling would become prevalent over the ensuing years with brick and mortar retailers being forced to offer an online solution, ecommerce companies needing to access buyers at physical locations and online brands (referred to as DTC or direct to consumer) being carried by 3rd party physical stores. Since that post, these trends have accelerated (including Amazon’s announcement last week that it is opening another “4-star store” in the bay area). Having had more time to observe this progression, I have developed several theories regarding this evolving new world that I would like to share in this post.

Issues for Brick and Mortar Stores when they Create an Online Presence

Physical retailers are not set up to handle volumes of online sales. Their distribution centers are geared towards sending larger volumes of products to their stores rather than having the technology and know-how to deal directly with consumers (a situation which motivated Walmart to buy Jet for $3.3 billion). In general, a retailer starting to sell online will need to create one or more new distribution centers that are geared towards satisfying direct to consumer online demand.

Another rude awakening for brick and mortar retailers when they go online is a dramatic increase in returns. On average, returns are about 9% of purchases from a retail store and 30% when purchased online. The discrepancy is even greater for clothing (especially shoes) as fit becomes a major issue. Given that consumers expect free shipping, and most want free return shipping, this becomes a cost that can eviscerate margins. The volume of returns also creates the problem of handling reverse logistics, that is tracking the return, crediting the customer, putting it back into the inventory system as available and restocking it into the appropriate bin location. Then there is the question as to whether the item can still be resold. For clothing this may require adding the cost of cleaning and pressing operations to keep the item fresh and having the systems to track movement of the inventory through this process.

Lastly, the question becomes whether a brick and mortar retailers’ online sales will (at least partly) cannibalize their in-store sales. If so, this, coupled with the growth of online buying, can make existing store footprints too large, reducing store profits.

If Brick and Mortar Retailers Struggle with an Omnichannel Approach, why do DTC Brands Want to Create an Offline Presence?

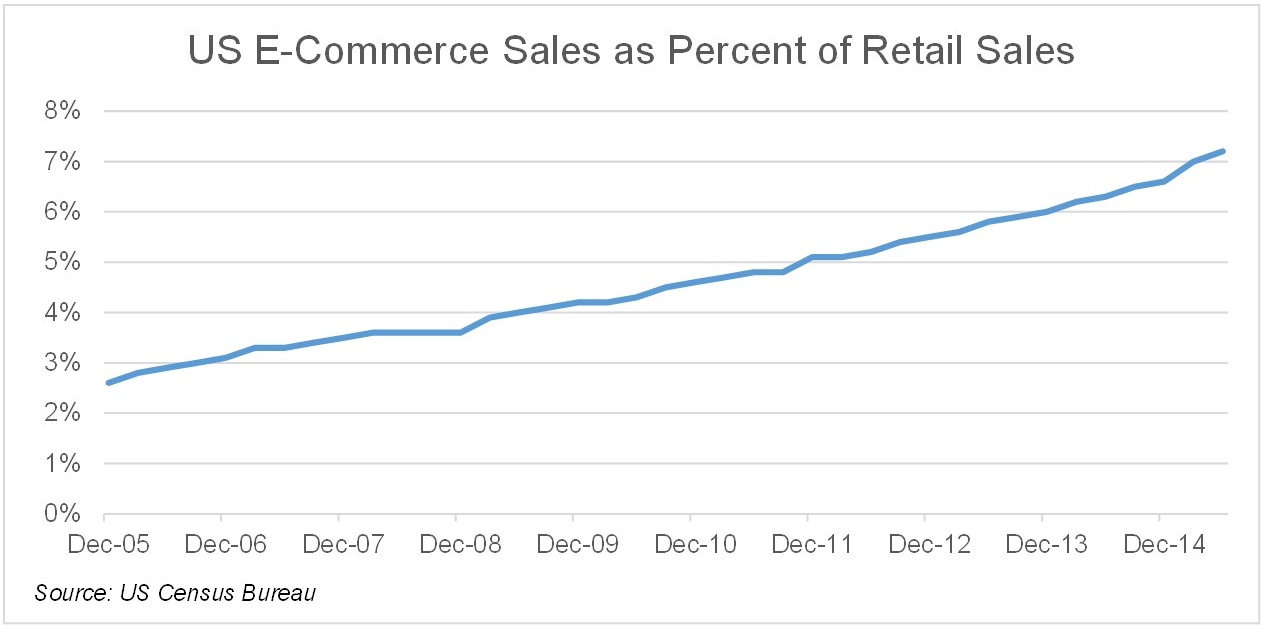

The answer is a pretty simple one: market access and customer acquisition. Despite a steady gain of share for online sales, brick and mortar still accounts for over 70% of consumer purchases. Not too long ago, Facebook was a pretty efficient channel to acquire customers. For the past 5 years, Azure portfolio companies have experienced a steep rise in CAC (customer acquisition cost) when using Facebook as the acquisition vehicle. There are many theories as to why, but it seems obvious to me that it is simply the law of supply versus demand. Facebook usage growth has slowed but the demand for ad inventory has increased dramatically, driving up prices. For large brands that use advertising for brand building rather than customer acquisition this does not appear to be a problem, especially when comparing its value to ads on television. For brands that use it for customer acquisition, doubling CAC changes the ratio of LTV (lifetime value or lifetime profits on a customer) to CAC making this method of customer acquisition far less effective.

The combination of these factors has led larger (and smaller) online brands to open brick and mortar outlets. Players like Warby Parker, Casper, Bonobos and even Tesla have done it by creating stores that are a different experience than traditional retail. Warby Parker, Bonobos and Tesla do not stock inventory but rather use the presence to attract customers and enable them to try on/test drive their products. I have bought products, essentially online, while at Warby Parker and Tesla physical locations.

I then had to wait between 2 to 6 weeks for the product to be manufactured and delivered (see the soundbite on Tesla below). What this means in each of their cases is that they kept their business models as ones of “manufacture to demand” rather than build to inventory. It seems clear that for all four of the companies cited above there is a belief that these physical outlets are a cost effective way of attracting customers with a CAC that is competitive to online ads. They also effectively use online follow-up once you have visited their brick and mortar outlet, thus creating a blend of the two methods. Once the customer is acquired, repeat purchases may occur directly online or in a combination of online and offline.

The Future Blend of Online/Offline

While we have seen a steady progression of companies experimenting with Omnichannel whether they started as offline or online players, we have yet to see an optimal solution. Rather, various players have demonstrated parts of that optimization. So, I’d like to outline a few thoughts regarding what steps might lead to more optimization:

- To the degree possible, online purchases by consumers should have an in-store pickup and review option at some savings versus shipping to the home. For clothing, there should also be an opportunity to try the online purchased items on before leaving the store. In that way consumers have the ability to buy online, coupled with the convenience of trying products on in a store. This would expose the customer to a broader set of inventory (online) than even a large footprint store might be able to carry. It would improve fit, lower cost to the brand (by lowering returns and reducing shipping cost) while allowing the brand to begin acquiring better information on fit – insuring an improvement for the next online purchase. A secondary benefit would be the increase in store traffic that was created.

- Many retailers will add Rental to the mix of options offered to customers to improve profits. Azure portfolio company, Le Tote, is a subscription rental company for everyday women’s clothes. As women give feedback on a large variety of aspects of fit and preferences it can improve the fit dramatically with each successive box. Retailers need to have systems that replicates this knowledge of their customers. The problem for pure brick and mortar retailers is that they have not had a relationship that enables them to get the feedback…and they don’t have software systems to build this knowledge even if they were to get it. Le Tote has also built up strong knowledge of women’s preferences as to style and has created successful house brands that leverage that knowledge based on massive feedback from subscribers. You may have seen the announcement that Le Tote has just acquired Lord & Taylor, the oldest department store in the country. It plans to use the millions of existing Lord & Taylor customers as a source of potential subscribers to its service. It also has a rental vehicle that can be used to improve monetization of items that don’t sell through at the stores.

- Successful online brands will be carried by offline retailers. This has already started to occur but will accelerate over time as DTC brands like Le Tote (and perhaps Stitchfix) use their tens of millions of specific customer feedback data points to produce products that meet the needs expressed in the feedback. If they have correctly mined the data, these brands should be quite successful in offline stores, whether it be their own or a third party retailers’ outlet. The benefit to the retailor in carrying online brands is two-fold: first the online brands that have effectively analyzed their data create products they know can sell in each geography; and second carrying online brands will improve the image of the retailor in the eyes of shoppers who view DTC companies as more forward thinking.

- Department store footprints will need to shrink or be shared with online players. The issue discussed earlier of overall ecommerce coupled with brick and mortar stores cannibalizing store demand when they start selling online can be dramatically mitigated by having smaller stores. In that way retailers can maintain their brand presence, continue to get foot traffic, and improve store efficiency. Any larger footprint store may need to take part of its space and either sublet it (as Macys is doing in some locations) or attract online brands that are willing to pay for a presence in those stores in the form of a percentage of revenue generated or rent. The offer to DTC brands may be to have a pop-up for a set period, or to agree to a longer-term relationship. By working with DTC brands in this way retailers can improve gross margin per square foot (a critical KPI for brick and mortar players) for poorly utilized portions of their store footprints. The secondary benefit to the retailer would be that the online brands will generate additional traffic to the stores. There are already a few startups that are creating a store within a store concept that carries DTC brands. They hope to be the middleman between DTC brands and large retailers/shopping malls making it easier for the DTC brands to penetrate more locations, and easier for the retailer to deal with one new player that will install multiple DTC brands in their locations.

- There will be more combinations of online and offline companies merging. By doing that the expertise needed for each area of the business can be optimized. The online companies presumably have better software, logistics and more efficient methods of acquiring online customers. The brick and mortar retailers have greater knowledge of running a physical store, an existing footprint to carry the online brands, locations that allow for delivery to their stores, and a customer base to market to online (reducing the CAC and increasing LTV).

- For Omnichannel companies, revenue attribution is complex but becomes essential to managing where dollars are spent. Revenue attribution is the tracking, connecting, and crediting marketing efforts to their downstream revenue creation. For example, if a potential customer responds to a Facebook ad by going online to look at items, then visits a store to check them out live, but eventually buys one or more of the items in response to a google ad, the question becomes: which channel should get credit for acquiring the customer? This is important as the answer may impact company strategy and help determine where marketing dollars get spent. Several Azure portfolio companies are now using 3rd party software from companies like Hive to appropriately give attribution to each channel that helped contribute to the eventual sale. This process is important as it helps determine future spending. We expect better run Omnichannel companies to evolve their analysis of marketing to include attribution models.

Conclusion: The future winners in retail will be those that successfully migrate to the most optimal omnichannel models

What I have described in this post is inevitable. Some large proportion of customers will always want to do some or all of their shopping at a brick & mortar store. By blending the positive attributes of physical retail with the accessibility to the larger number of options that can exist online, companies can move to more optimal models that address all potential customers. But unless this is done in an intelligent way booby traps like inefficient floor space, excessive returns, high shipping costs and more will rear their ugly heads. This post describes steps for retailers/brands to take that are a starting point for optimizing an omnichannel approach.

Soundbytes

- When I had just left Wall Street, I received calls from the press and a very large investor in Hewlett Packard regarding my opinion of the proposed acquisition of Compaq Computer. I said: “HP is in 6 business areas with Imaging being their best and PCs their worst. Doubling up on the worst of the 6 does not make sense to me.” When asked what they should do instead, I replied: “Double up on the best business: acquire Xerox.” My how the tide has turned as Xerox was in trouble then and could have been bought at a very low price. Now it appears Xerox may acquire HP. To be clear, Xerox is still a much smaller market cap company…but I’m enjoying seeing how this process will work out.

- In the last Soundbytes, I mentioned that I had purchased a Tesla Model 3. What is interesting is that 6 weeks later I am being told that it may take as long as 3-4 more weeks before I receive the car. This means delivery times have extended to at least 9 weeks. I can’t say how reliable this is but the salesperson I am dealing with told me that Tesla has prioritized production of Model S, Model X and shipments to Europe and Asia over even the more expensive versions of Model 3’s (mine cost almost $59,000 before sales tax). One can easily conclude that production must be at full capacity and that the mix this quarter will contain more higher priced cars. So, demand in the quarter appears to be in excess of 100,000 units and price per car appears strong. Assuming the combination of maximum production in the U.S. and some production out of the Chinese factory, supply might also exceed 100,000 units. If the supply is available, then Tesla should have a strong Q4. However, there is the risk that Tesla doesn’t have the parts to supply both factories or that they have somehow become less efficient. The latest thing to drive down the Tesla stock price is the missteps in showcasing the new truck. I’m not sure why a company should be castigated for an esoteric feature not working in a prototype of a product that won’t be in production until sometime in 2021. Remember, Tesla at its core is a technology company producing next gen autos. I’ve seen other technology companies like Microsoft and Oracle have glitches in demos of future products without such a reaction. As for the design of the truck, I believe Tesla is targeting a 10% to 20% share of the truck market with a differentiated product rather than attempting to attract all potential buyers. 10% of the U.S. pickup market would result in 250,000 units per year. The company has announced pre-orders for the vehicle have already reached 200,000. If these orders are real, they have a home run on their hands but since the deposit is only $100 there is no guarantee that all deposits will convert to actual purchases when the truck goes into production.