Mike Kwatinetz is a Founding General Partner at Azure Capital Partners and a Venture Capitalist investing in application software (SaaS), ecommerce, consumer web and infrastructure technology companies. Successful exits include: Bill Me Later, VMware, TripIt and Top Tier.

Our predictions for 2023 were all fulfilled with the stock portion providing extremely strong performance. This was on the heels of poor performance in 2022 as it was one of the worst years in the past 50 for the stock market in general, and for my stocks in particular. In delineating the stock recommendations in our Top Ten predictions for 2023 we pointed out that the 6 stocks, on average had fallen nearly 49% in 2022 despite average revenue growth of about 38%. Since we expected all 6 to continue to grow in 2023 (and both Amazon and Shopify to increase their growth rates), we felt they were all poised for a recovery. This clearly proved accurate.

What went right for my stock picks in 2023 was great company results coupled with the benefit of an apparent end to the rate hike cycle. I have always pointed out that I am not amongst the best at forecasting the market as a whole but have been very strong at selecting great companies which over the long term (5 years or more) typically have solid stock appreciation if their operating performance is consistently good. But even great company’s stock performance can be heavily impacted in any given year by market conditions. Two key drivers of negative market conditions in 2022 were the huge spike in inflation coupled by the Fed raising rates to battle it.

At the beginning of 2023 we felt that inflation would be on the decline from its peak of 9.1% in June 2022 (see prediction 9). Given the expected decline in inflation we believed the Fed would slow and then stop increasing interest rates. Since the rise in interest rates was a major reason for the decline in our long-duration stocks, we believed that slowing and then stopping this rise would be a factor in driving elevated stock performance.

So, the big question for the market at the beginning of 2023 was whether the expected additional rate increases projected at just under 1% for the year (which theoretically was built into share prices at the end of 2022) would be enough for The Fed. It pretty much was as the Fed raised rates 1.0% during the year but stopped making increases after July and subsequently indicated that rates could start declining in 2024.

Stocks reacted well to what appears to be end of the upward climb in rates and tech stocks reacted particularly well as long duration investments tend to be influenced greatly by rate changes. Coupling this with what appears to be a soft landing created a positive environment for our recommended stocks.

Our six recommended stocks were up an average of 96% with 3 of the 6 appreciating over 100%. While we will have a longer discussion of the reasoning behind it in our next post, we wanted to disclose that all 6 will be recommendations in our 2024 Top Ten.

2023 Stock Recommendations

Tesla will outperform the market (it closed 2022 at $123.18/share)

As usual, Tesla was a wild ride in 2023. Partly, this was based on continued controversy surrounding Elon especially his actions post his October 2022 purchase of Twitter (now called X). But in addition, concerns over price drops, potential slowing momentum of Battery Electric Vehicles, challenges to Tesla market share and more weighed on the stock at times. These concerns buried the stock in 2022. In 2023 they continued to be sighted by shorts but proved overblown as the company reached its unit sales target of 1.8 million vehicles (up 40%), launched the CyberTruck in Q4 and substantially increased its market share of overall vehicles sold. As a result, Tesla stock was very strong in 2023 and closed the year at $248.48/share, a rise of 102%.

2. CrowdStrike (Crwd) will outperform the market (it closed 2022 at $105.29/share)

The most recently reported quarter for CrowdStrike, Q3 FY24 was another strong one as the pandemic had little impact on its results. Revenue was up over 35% and earnings 105%. Existing customers continued to expand use of the company’s products driving Net Revenue Retention to exceed 120% for the 20th consecutive quarter. The company’s stock, which had declined nearly 50% in 2022 (despite a revenue increase of 54%), had a dramatic recovery. It closed 2023 at $255.17/share, up 142%.

3. Amazon will outperform the market (it closed 2022 at $84.00/share)

As we expected, Amazon improved revenue growth in each quarter of 2023 from its low point of 8.6% in Q4 2022. In Q3 2023 growth was back to 12.6%. Additionally, the company increased its focus on profitability with Q3 profits up well over 200% versus the prior year’s weak numbers. This coupled with the improved environment for tech stocks helped drive Amazon’s share price to $151.75 at year end, up 81% from the close on December 31, 2022.

4. The Trade Desk (TTD) will outperform the market (it closed 2022 at $44.83/share)

Fears of a potential recession caused great concern for advertising revenue. After dropping sequentially in Q4 2022 (to 24.1%) and again in Q1 2023 (to 21.5%) TTD’s revenue growth began recovering in Q2 (to 23.1%) and again in Q3 (to 27.7%). The stock reacted well to the improvement and closed 2023 at $71.80 up 60% from year end 2022.

5. Datadog will outperform the market (it closed 2022 at $73.50/share)

Like many other high growth subscription-based software companies, Datadog experienced another solid year in 2023 with Q3 revenue growth at 26.7%. Also, like CrowdStrike, Datadog has a very high gross margin (GM) and is now at the point where it has started to leverage its GM driving up earnings (+96%) at a much faster rate than revenue. This level of success helped Datadog stock close the year at $121.65/share, up 66%.

6. Shopify (Shop) will outperform the market (it closed at $34.71/share)

In our post of Top Ten predictions, we pointed out that the pandemic had created a major warping of Shop revenue growth. Instead of the normal decline for high growth companies from its 47% level in 2019 it jumped to 86% growth in 2020 and still was above “normal” at 57% in 2021. Once physical retail normalized in 2022, Shopify growth plunged against the elevated comps declining to a nadir of 16% in Q2, 2022. When we included Shop in our Top Ten for 2023, we pointed out that we expected its revenue growth to return to 20% or more throughout 2023. This indeed did occur and the stock reacted well, closing the year at $77.88 up 124% year/year.

Non-Stock Specific Predictions

While I usually have a wide spectrum of other predictions, last year I wanted to focus on some pressing issues for my 3 predictions that are in addition to the fun one. These issues are Covid, inflation and California’s ongoing drought. They have been dominating many people’s thoughts for the past 3 years or more.

7. The Warriors will improve in the second half of the current season and make the Playoffs

This forecast proved correct as I expected the Warriors to make the playoffs but be unsuccessful at winning a title. They did rally in the latter part of the season to finish 6th (avoiding the play-in) and won the series against the Kings but failed to progress to the Western Finals.

8. Desalination, the key to ending long term drought, will make progress in California

Some of the pressure to create desalination plants throughout California was reduced by substantial rainfall last year that ended the drought and filled reservoirs. Despite this there was progress as the California Coastal Commission approved a $140 million desalination plant in Orange County (at Dana point) in late 2022. Resistance to its construction has been mounted by environmental groups but in 2023 the planning continued to move forward.

In April 2023, the Department of Water Resources (DWR) announced 3 more projects that will receive support from DWR and an additional 6 projects that will receive funds through a partnership with the National Alliance for Water Innovation. While the total water generated through all projects currently approved is still far short of fulfilling California needs, the tide seems to have begun to turn (no pun meant) towards favoring use of desalination.

9. Inflation will continue to moderate in 2023

This forecast proved pretty accurate as inflation moderated to just over 3% in 2023 (very slightly higher than my projected range). It was at 6.3% when I made the forecast.

10. Covid’s Impact on society in the US will be close to zero by the end of 2023

I consider this prediction mostly right. On the positive side I believe Covid no longer has much influence on people venturing out to shop, dine, go to the theater, travel, etc. Even cruise lines are experiencing a substantial return towards normal. The number of new Covid cases has waned significantly and deaths from it are close to zero. However, I would not say we’re quite at zero impact as there are still some spikes (of modest magnitude versus before) that cause concern to a portion of the population.

2022 was one of the worst years in the past 50 for the stock market in general, and for my stocks in particular. There are multiple ways to look at it. On the one hand I’m mortified that stocks that I selected have declined precipitously not only impacting my personal investment portfolio but also those of you who have acted on my recommendations. On the other hand, I believe this creates a unique opportunity to invest in some great companies at prices I believe are extremely compelling.

What went wrong for my stock picks in 2022? I have always pointed out that I am not amongst the best at forecasting the market as a whole but have been very strong at selecting great companies which over the long term (5 years or more) typically have solid stock appreciation if their operating performance is consistently good. But even great company’s stock performance can be heavily impacted in any given year by market conditions. Two key drivers of negative market conditions in 2022 were the huge spike in inflation coupled by the Fed raising rates to battle it. Inflation peaked at 9.1% in 2022. To put this in perspective, in the 9 years from 2012 to 2020, inflation was between 0.12% and 2.44% with 6 of the years below 2.0%. It began to increase in 2021 (up to 4.7%) but many thought this was temporary due to easing of the pandemic. When the rate kept increasing in the first half of 2022 the Feds began to act aggressively. A primary weapon is increasing the Fed Rate which they did 7 times in 2022 with the total increase of 4.25% being the largest amount in 27 years.

When rates increase the market tends to decline and high growth stocks decline even faster. So, the big question in 2023 is whether the expected additional rate increases projected at just under 1% for the year (which theoretically is built into current share prices) is enough for The Fed. In November, inflation was down to 7.11% and decreased further in December to 6.45%. If inflation continues to ease, The Fed can keep rate hikes in line with or below their stated target and market conditions should improve.

Of course, there is another issue for bears to jump on – the potential for a recession. That is why the December labor report was comforting. Jobs growth remained solid but not overly strong growing at 247,000 for the prior three months. This was substantially lower then where it had been at the end of 2021 (637,000 in Q4). While jobs growth of this amount might lead to wage growth of substance, the growth in December was a fairly normal 0.3%. If this persists, the theory is that inflation will moderate further. Additionally, more and more companies are announcing layoffs, particularly in the Tech sector.

I pointed out above that I am not a great forecaster of economics or of the market as a whole so the above discussion may not mean inflation moderates further, or that Fed Rate hikes stay below a one percent total in 2023, or that we avoid a deep recession – all of which could be further negatives for the market. But given where stocks now sit, I expect strong upside performance from those I recommend below.

I also want to mention that given the deep decline in the market, 2022 was extremely busy for me and the decline in blogs produced has been one of the consequences. I’ll try to be better in 2023! I am going to publish the recap of 2022 picks after the new Top Ten blog is out. Suffice it to say the recap will be of a significant miss for the stocks portion of the forecast, but that means (at least to me) that there is now an opportunity to build a portfolio around great companies at opportune pricing (of course I also thought that a year ago).

Starting in mid-2021 the Tech sector has taken a beating as inflation, potential interest rate spikes, the Russian threat to the Ukraine (followed by an invasion), a Covid jump due to Omicron and supply chain issues all have contributed to fear, especially regarding high multiple stocks. What is interesting is that the company performance of those I like continues to be stellar, but their stocks are not reflecting that.

For 2023, the 6 stocks I’m recommending are Tesla(TSLA), Amazon (AMZN), CrowdStrike (CRWD), Shopify (SHOP), Data Dog (DDOG) and The Trade Desk (TTD). The latter two replace Zoom and DocuSign. While I have removed Zoom and DocuSign from this year’s list, I still expect them to appreciate but their growth rates are substantially below their replacements.

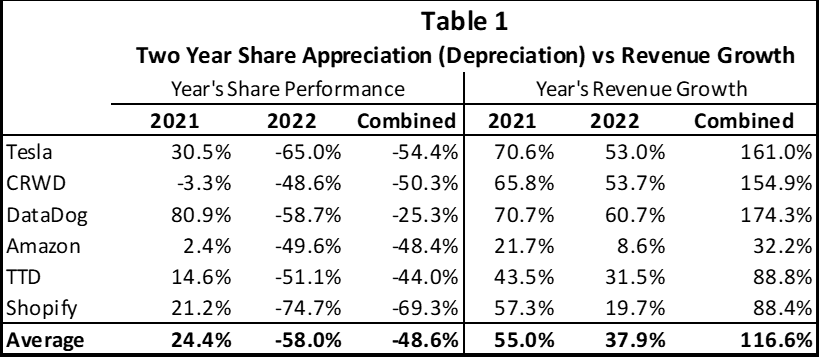

In the introduction to my picks last year, I pointed out that over time share appreciation tends to correlate to revenue growth. This clearly did not occur over in the last 12 months or the last 24 months as illustrated in Table 1.

Note: 2022 for CRWD is actually FY 23 estimated revenue as year end is Jan 31. 2022 revenue uses analyst consensus estimates for Q4 which has on average been lower than actual revenue. Averages are unweighted.

The average revenue gain in 2022 (FY 23 for CRWD) reported by these companies (using analyst estimates for Q4) was nearly 38% while the average stock in the group was down 58%. In 2021 all the stocks except CRWD were up but only Data Dog had higher appreciation than its revenue growth. But in 2022 Data Dog declined significantly despite over 60% revenue growth. If we look at the two-year combined record the average stock in this group had a revenue increase of over 116% with three of the six increasing revenues by over 150%! Yet, on average, share performance for the group was a decline of over 48%. It should also be noted that Amazon’s major profit driver, AWS grew much more quickly than the company as a whole. Another point to highlight is that the strength of the dollar meant that US dollar revenue growth was lower than actual growth on a neutral dollar basis.

While over time I would expect share performance to be highly correlated to revenue growth, clearly that has not been the case for the past 24 months. I look at the revenue multiple as a way of measuring the consistency of valuation. Of course, these multiples should be lower as a company’s growth rate declines but looking at these 6 companies the amount of the decline is well beyond anything usual. Certainly, the pandemic causing wild swings in growth rates is partly responsible in the case of Amazon and Shopify but the other 4 companies have continued to experience fairly usual growth declines for high growth companies and all remain at strong growth levels.

Table 2 shows the change in revenue multiples in 2021 and in 2022 and then shows the 2-year change as well. Over the 2-year period every one of these stocks experienced a multiple decline of at least 60% with three of them declining more than 80%. Even if one assumes that valuations were somewhat inflated at the beginning of 2021 it appears that they all have substantial upside from here especially given that they are all growth companies. Which means if the multiples stabilize at these levels the stocks would appreciate substantially in 2023. If the multiples returned to half of where they were on December 31, 2020, the appreciation would be pretty dramatic.

Notes: 1. CRWD numbers are for fiscal years 2022 and 2023 ending January 31. 2. For Q4 revenue for each company we used Analyst average estimates. 3. All averages are calculated on an unweighted basis.

Given the compression in revenue multiples across the board in tech stocks, the opportunity for investing appears timely to me. Of course, I cannot predict with certainty that the roughly 75% average decline in revenue multiple among these stocks represents the bottom but we never know where the bottom is.

2022 Stock Recommendations

(Note: as has been our method base prices are as of December 31, 2022)

1. Tesla will outperform the market (it closed 2022 at $123.18/share)

Despite revenue growth of over 50%, Tesla was one of the worst stocks in 2022. While Q4 financials have yet to be reported, the company car sales were announced as 405,278 in the quarter up over 31%. For the year, the company shipped over 1.3 million vehicles up 40% over 2021. These volumes are still without Tesla being in the biggest category of vehicles, pickup trucks. Revenue in Q4 is expected to be up more than units with an over 35% increase the analyst consensus (note: Tesla reported last night, and revenue was up 37%).

Earnings have been increasing faster than revenue and consensus earnings estimates for 2022 is over $4 (it came in at $4.07 up 80%), meaning the stock is now trading at about 30 X 2022 earnings. This is a very low level for a high growth company.

One concern for investors is the decrease in the Tesla backlog. At year end it was at about 44 days of production (or roughly ½ of units sold in Q4. While there are many elements to consider there is a concern that it will be difficult for Tesla to maintain an above 30% vehicle growth rate in 2023. But there are several factors that indicate that such a concern is potentially incorrect:

The US began again offering a $7500 tax credit for electric vehicles starting January 1, 2023. This clearly caused many to postpone their purchase to get the credit. Tesla attempted to offset this by offering a similar discount in the US late in 2022 but it is likely that demand was seriously impacted. In early 2023 Tesla lowered prices to insure more of its units qualified for the credit. While this price decrease lowers average AOV from Q4 it still left most of its units at or above prices one year ago as Tesla had raised prices multiple times in 2022.

The Tesla CyberTruck has a wait list that exceeds 1.5 million vehicles, which if added to the backlog, would increase it to a full year of vehicles. But, of course, the company needs to get this into production to address these orders. Currently the company is expected to begin production around the middle of this year and get to high volume some time in Q4.

Tesla has an easy comp in Q2 since China shut down for much of Q2 2022.

The company now has the manufacturing capacity to increase volumes – the question will be parts supply and whether demand will be strong if the economy goes into a recession.

Since manufacturing capacity increased by the end of Q3, Q4 showed another strong sequential increase in units sold of nearly 18%. Once again demand was not an issue for the company as its order backlog, while lower than at its peak, remained at 6 weeks exiting the quarter. This does not include the estimated 1.5 million units in backlog for the Tesla CyberTruck which would put the total backlog at over one year of current production capacity. The current estimate for this vehicle going into production is roughly mid-year 2023.

Tesla has increased manufacturing capacity with Fremont and China at their highest levels ever exiting Q3, and Berlin and Texas in the early ramp up stage. Despite a reduction of its backlog, demand for its vehicles continues to increase. As you hear of new competition in the electric vehicle market keep in mind that Tesla share of the US market for all cars is still only about 3% and in China and Europe it remains under 2%. As the world transitions to electric vehicles, we expect Tesla’s share of all auto sales to rise substantially, even as it declines in total dominance of the electric vehicle market. It deserves re-emphasis: when the Cybertruck begins shipping, Tesla total backlog could exceed one year of units even assuming higher production. And the Cybertruck current backlog isn’t expected to be fulfilled until late 2027!

As we forecast in prior letters, Tesla gross margins have been rising and in Q3 remained the highest in the industry. While lower vehicle prices and increasing cost of parts will place some pressure on gross margins, we still believe they will continue to remain by far the highest of any auto manufacturer:

Tesla, like Apple did for phones, is increasing the high margin software and subscription components of sales;

The full impact of price increases was not yet in the numbers last year, so its price reductions have less impact than their percent of AOV and add-on sales are likely to offset a portion of the decreases;

As its new factories ramp, they will increase their efficiency; and

Tesla will have lower shipping cost to European buyers as the new Berlin factory reaches volume production.

In Q4, we believe the Tesla Semi was produced in very small volumes and limited production capacity will mean any deliveries will remain minimal during the next few quarters. However, given its superior cost per mile the Semi is likely to become a major factor in the industry. Despite its price starting at $150,000 its cost per mile should be lower than diesel semis. Given potential of up to $40,000 in US government incentives the competitive advantage over diesels will be even greater. The company is expecting to increase production to about 50,000 per year by some time in 2024 (which would represent potential incremental annual sales in the 8-10 billion range). While this is ambitious, the demand could well be there as it represents a single digit percent of the worldwide market for a product that should have the lowest cost/mile of any in the semi category.

The new version of the roadster is being developed but it’s unclear when it will be ready. Nevertheless, it will become another source of incremental demand at high margins. What this all points to is high revenue growth continuing, strong gross margins in 2023 and beyond, and earnings escalation likely faster than revenue growth. While revenue growth is gated by supply constraints it should still be quite strong. The high backlog helps assure that 2023, 2024 and 2025 will be high growth years. While the company has reduced pricing recently, the ability to sell greater dollars in software should help maintain strong AOV and gross margins

2. Crowdstrike (Crwd) will outperform the market (it closed 2022 at $105.29/share)

The most recently reported quarter for CrowdStrike, Q3 FY23 was another strong one as the pandemic had little impact on its results. Revenue was up 53% and earnings 135%. Existing customers continued to expand use of the company’s products driving Net Revenue Retention to exceed 120% for the 16th consecutive quarter. CrowdStrike now has over 59% of customers using 5 or more of its modules and 20% using at least 7 of its modules. Of course, the more modules’ customers use the bigger the moat that inhibits customer defection.

Older data security technology was focused primarily on protecting on-premises locations. CrowdStrike has replaced antivirus software that consumes significant computing power with a less resource-intensive and more effective “agent” technology. CrowdStrike’s innovation is combining on premise cybersecurity measures with protecting applications in the cloud. Since customers have a cloud presence, the company is able to leverage its network of customers to address new security issues in real time, days faster than was possible with older technology. While the company now has nearly 20 thousand subscription customers it is still relatively early in moving the market to its next gen technology. Given its leadership position in the newest technology coupled with what is still a modest share of its TAM the company remains poised for high growth.

High revenue growth coupled with 79% subscription gross margins, should mean earnings growth is likely to continue to exceed revenue growth for some time. In Q3 earnings grew 135%. While its stock is being penalized along with the rest of the tech market (its multiple of revenue declined by over 66% in 2022 and 80% in the past 2 years), its operational success seems likely to continue. Once pressures on the market ease, we believe CrowdStrike stock could be a substantial beneficiary.

3. Amazon will outperform the market (it closed 2022 at $84.00/share)

Amazon improved revenue growth in Q3 to 15% from 7% in Q2. In constant currency (taking out the impact of the increased strength of the dollar) its growth was 19% versus 10% in Q2. However, the company guidance for Q4 unnerved investors as it guided to Q4 revenue growth of 2-8% year/year and 4.6% higher in constant currency. Because AWS, which grew 27% y/y in Q3 is a smaller part of revenue in Q4 than other parts of the year, the weaker consumer growth can tend to mute overall growth in Q4. As the company heads into 2023 it should benefit from weaker comps and we expect revenue growth to improve from Q4. Of course, the Fed pushing up interest rates is likely to slow the economy and Analysts are currently predicting revenue growth of about 10% in 2023 (which would be higher in constant currency). But it’s important to understand that the profit driver for the company is AWS which generates nearly all the profits for the company. Even in a weaker economy we would expect AWS revenue to grow over 20%.

While Amazon is not the “rocket ship” that other recommendations offer, its revenue multiple has slipped by over 60% in the past 2 years. We believe improved growth coupled with smaller Fed increases should benefit the stock. One important side point is that the fluctuation in Rivian stock impacts Amazon earnings and Rivian was down quite a bit in Q4.

One wild card for the stock is whether its recent 20 for 1 stock split will lead to its being included in the Dow Jones Index. Because the index is weighted based on stock price Amazon could not be included prior to the split as its weight (based on stock price) would have been around 30% of the index. Given its share price post-split it is now a good fit. The Dow Index tries to represent the broad economy so having the most important company in commerce included would seem logical. Changes in the composition of the index are infrequent, occurring about once every 2 years, so even if it gets included it is not predictable when that will occur. However, should it occur, it would create substantial incremental demand for the stock and likely drive up the price of Amazon shares.

4. The Trade Desk (TTD) will outperform the market (it closed 2022 at $44.83/share)

TTD provides a global technology platform for buyers of advertising. In the earlier days of the web, advertisers placed their ads on sites that had a large pool of users that met their demographic requirements. These sites were able to charge premium rates. TTD and others changed this by enabling an advertiser to directly buy the demographic they desired across a number of sites. This led to lower rates for advertisers and better targeting. Now with the rise of Connected TV TTD applies the same method to video. By moving in this direction advertisers can value and price data accurately. Given its strength of relationships, TTD has become the leader in this arena. The company believes that we are early in this wave and that it can maintain high growth for many years as advertisers shift to CTV from other platforms that have been more challenged due to government regulations regarding privacy as well as Apple changes for the iPhone.

In Q3 The Trade Desk grew revenue 39% and earnings 44% as their share of the advertising market continued to increase. We believe TTD can continue to experience strong growth in Q4 and 2023. We also believe after having its revenue multiple contract 70% over the past 2 years the company can also gain back some of that multiple.

5. DataDog will outperform the market (it closed 2022 at $73.50/share)

Datadog is an observability service for cloud-scale applications, providing monitoring of servers, databases, tools, and services, through a SaaS-based data analytics platform. Despite growing revenue close to 60% and earnings about 100% its stock still declined about 59% in 2022 due to the rotation out of tech stocks driven by the large Fed Rate increases. The company remains in a strong position to continue to drive high revenue growth and even higher earnings growth going forward.

6. Shopify (Shop) will outperform the market (it closed at $34.71/share)

Shop, like Amazon, experienced elevated growth in 2020 and the first half of 2021. This was due to Covid keeping people out of stores (many of which weren’t even open) and resulted in revenue escalating 86% in 2020 from 47% in 2019. The rate tapered off to a still elevated 57% in 2021 with Q4 at 41%. The elevated comps resulted in a decline in growth to below normalized levels once consumers returned to Brick & Mortar stores. By Q2, 2022 year over year revenue growth had fallen to 16%. We expected growth to return to over 20% and potentially stabilize there. This occurred in Q3 as revenue growth improved to 22%. We believe Shopify can continue to achieve stable growth in the 20% range or higher in 2023 as long as the economy does not go into a deep recession. Shopify has established a clear leadership position as the enabler of eCommerce sites. Its market share is second to Amazon and well ahead of its closest competitors Walmart, eBay, and Apple. Net revenue retention for the company continues to be over 100% as Shopify has successfully expanded services it provides to its eCommerce business customers. Additionally, because successful eCommerce companies are growing, Shopify also grows its portion of the customer revenue it shares.

Because of the wild swing in growth due to Covid, Shop experienced the most extreme multiple compression of the 6 stocks we’re recommending, 79% last year and 84% over the past two years. This leaves room for the stock to appreciate far beyond its growth rate in 2023 if market conditions improve.

Non-Stock Specific Predictions

While I usually have a wide spectrum of other predictions, this time I wanted to focus on some pressing issues for my 3 predictions that are in addition to the fun one. These issues are Covid, inflation and California’s ongoing drought. They have been dominating many people’s thoughts for the past 3 years or more. The danger in this is that I am venturing out of my comfort zone with 2 of the 3. We’ll start with the fun prediction.

7. The Warriors will improve in the second half of the current season and make the Playoffs

I always like to include at least one fun pick. But unlike a year ago, when I correctly forecast that the Warriors would win the title, I find it hard to make the same pick this year. While I believe they can still win it, they are not as well positioned as they were a year ago. This is partly because a number of teams have gotten considerably better including Memphis, Denver, the Kings and New Orleans in the West (with the Thunder, an extremely young team appearing to be close) and the Celtics, Bucks, Nets and Cavaliers in the East. The Warriors, by giving up Otto Porter and Gary Payton II (GPII), and other experienced players, took a step backwards in the near term. I believe signing Divincenzo gives them a strong replacement for GPII. They will need Klay and Poole to play at their best and Kuminga to continue to progress if they are to have a stronger chance to repeat.

8. Desalination, the key to ending long term drought, will make progress in California

It’s hard to believe that California has not been a major builder of desalination plants given the past 7 years of inadequate rainfall. Despite the recent rainfall, which might bring reservoirs back to a normal state by summer, it appears to be a necessary part of any rational long-term plan. Instead, the state is spending the equivalent of over one desalination plant per mile to build a high-speed railway (HSR) ($200 million per mile and rising vs $80 million for a small and up to $250 million for a very large desalination plant). When voters originally agreed to help fund the HSR the cost was projected at $34 billion dollars. According to the Hoover Institute, the cost has grown to over triple that and is still rapidly rising. If I had my druthers, I would divert at least some of these funds to build multiple desalination plants so we can put the water crisis behind us. Not sure of how many are needed but it seems like 10 miles of track funding 10 larger plants would go a long way towards solving the problem. It is interesting that Israel has built plants and has an abundance of water despite being a desert.

9. Inflation will continue to moderate in 2023

The Fed began raising rates to combat inflation early in 2022, but it didn’t peak until June when it reached 9.1%. One trick in better understanding inflation is that the year over year number is actually the accumulation of sequential increases for the past 12 months. What this means is that it takes time for inflation to moderate even when prices have become relatively stable. Because the sequential inflation rates in the second half of the year have been much lower than in the first half, inflation should keep moderating. As can be seen from Table 3, the full year’s increase in 2022 was 6.26% (which is slightly off from the announced rate as I’ve used rounded sequential numbers). The magnitude of the increase was primarily due to the 5.31% increase from January 1 through June 30.

If the second half of the year had replicated this, we would be at over 11% for the year. However, the Fed actions have taken hold and in the second half of the year (July 1 – December 31) inflation was down to 0.90% or an annualized rate of under 2.0%. And between November 1 and December 31 we had complete flattening of sequential cost. What this indicates to me is that the likelihood of inflation moderating through June 30, 2023 is extremely high (no pun meant). If I were to guess where we would be in June, I’d speculate that the year/year increase will be between 1% and 3%.

10. Covid’s Impact on society in the US will be close to zero by the end of 2023

Covid has reached the point where most (roughly 70%) of Americans are vaccinated and we estimate that over 75% of those that aren’t have already been infected at some point and therefore have some natural immunity. This means about 92% of Americans now have some degree of protection against the virus. Of course, given the ongoing mutation to new forms of Covid (most recently to the Omicron version) these sources of immunity do not completely protect people and many who have been vaccinated eventually get infected and many who already had Covid got reinfected. However, if we study peak periods of infection there appears to be steady moderation of the number of infections.

Covid infections reached their highest peak in the US around January 2022 at a weekly rate of approximately 5 million new cases. It subsequently dropped steadily through May before rising to another peak, fueled by Omicron, in July 2022 at a weekly rate of about 1 million (an 80% peak to peak decrease). Again, it subsequently dropped until rising more recently to a post-holiday/winter peak in early January 2023 to a weekly count of under 500,000 (a peak-to-peak drop of over 50% from July).

While the progress of the disease is hard to forecast the combination of a more highly vaccinated population coupled with a high proportion of unvaccinated people now having some immunity from having contracted the disease seems to be leading to steady lowering of infection rates.

More importantly, death rates have declined even faster as lower infection rates have been coupled with milder cases and better treatments (due to vaccinations and natural immunity increases for the 50% of the population that have contracted the disease over the past 3 years). Despite the recent post-holiday spike, deaths from Covid were under 4,000 across the country (or about 0.001% of the population) in the most recent week reported. If the seasonal pattern follows last year, this will be a peak period. So, using this as being very close to the likely maximum rate per week, we can forecast that the annual death rate from Covid in 2023 will be between 100,000 and 200,000 Americans. This would put it between the 4th and 6th leading causes of death for the year with heart disease and Cancer the leading causes at over 600,000 each.

Given that most people have already significantly reduced use of masks and are visiting restaurants, department stores, theaters, sporting events, concerts and numerous other venues where people are quite close to each other, we believe the impact of Covid on the economy has faded and that 2023 will be a relatively normal year for consumers. Of course, the one wild card, which I believe has a low probability of occurring, is that a new variant causes a surprising massive spike in deaths.

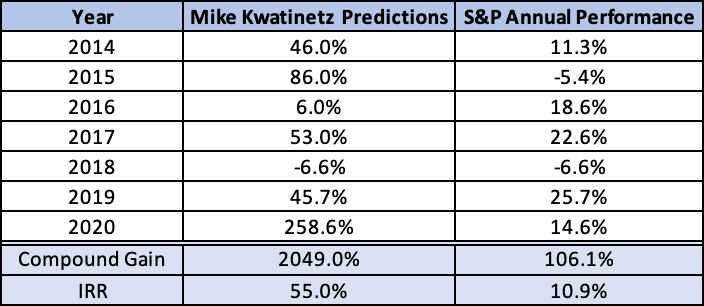

I wanted to start this post by repeating something I discussed in my top ten lists in 2017, 2018 and 2020 which I learned while at Sanford Bernstein in my Wall Street days: “Owning companies that have strong competitive advantages and a great business model in a potentially mega-sized market can create the largest performance gains over time (assuming one is correct).” It does make my stock predictions somewhat boring (as they were on Wall Street where my top picks, Dell and Microsoft each appreciated over 100X over the ten years I was recommending them).

In the seven years we have been offering stock picks on this blog this strategy has worked quite well as the cumulative gains for my picks now exceeds 21X and the 7-year IRR is 55%. The two stocks that have been on the list every year, Tesla and Facebook, were at the end of 2020 at 77X and 11X, respectively, of the price I bought them in mid-2013. They both have been on our recommended list every year since but this is about to change.

In last year’s Top 10 list I pointed out that my target is to produce long-term returns at or above 26%. At that rate one would double their money every 3 years. Since the S&P has had compound growth of 10.88%/year for the past 7 years, and Soundbytes has been at 55%, I thought you might find it interesting to see how long a double takes at various levels of IRR and what multiple you would have after 10 years for each one.

Table: Compound Returns at Various Rates

The wonder of compounding is quite apparent in the table, but it also shows that patience is a virtue as holding the stocks of great companies longer can multiply your money significantly over time, while too many investors become inpatient and sell prematurely. In our last post of 2020 we outlined the thinking process to select great companies, but even great companies can have some periods where their returns are below par. Given that our picks were up an average of 259% last year, I’m back to a fearful mode that 2021 might be that period. Of course, I’m always fearful but sticking with great companies has worked out so far and trying to time when to sell and buy back those companies often leads to sub-optimization.

To some extent, over a 5-year period or longer, stock appreciation is correlated with a company’s growth. So, as I go through each of my 6 stock picks, I will discuss what that might mean for each company. With that in mind, as is my tendency (and was stated in my last post), I am continuing to recommend 5 of the 6 stocks from last year: Tesla, Zoom, Amazon, Stitch Fix and DocuSign. I am removing Facebook from the list and adding CrowdStrike. To be clear, I still believe Facebook will outperform the S&P (see Pick 7 below) but I also believe that over the next few years CrowdStrike and the 5 continuing stocks will experience greater appreciation.

2021 Stock Recommendations:

1. Tesla stock appreciation will continue to outperform the market (it closed last year at $706/share)

Tesla is the one stock in the group that is not trading in synch with revenue growth for a variety of reasons. This means it is likely to continue to be an extremely volatile stock, but it has so many positives in front of it that I believe it wise to continue to own it. The upward trend in units and revenue should be strong in 2021 because, in addition to continued high demand for the model 3:

China Expansion: Tesla continues to ramp up production in China, the world’s largest market. In 2020 the company sold about 120,000 cars (which placed it a dominant number 1 in battery powered cars) there as its Giga Factory in Shanghai ramped up production. Trade Group China Passenger Car Association predicts that Tesla will sell as many as 280,000 vehicles there in 2021…an increase of about 133%. While that is significant growth it only would represent 20% of the number of battery powered vehicles forecast to be sold. The limitation appears to be production as the Shanghai factory is just nearing a volume of 5,000 vehicles per week. Tesla believes it can double that during this year. The Model Y has just been introduced in China and early press is calling it a major hit. Together with the Model 3, I believe this positions Tesla to be supply constrained. Should the company increase production earlier in the year, it has the opportunity to sell more than the forecast 280,000 vehicles. What is also important to note, is Tesla seems to be making greater profits on sales of its cars in China than in the U.S so as China becomes a larger portion of the mix Gross Margin could increase.

European Factory: Tesla has a cost disadvantage in Europe as its cars are not currently built there. So, while it established an early lead in market share, as others have launched battery powered vehicles at lower prices Tesla lost market share. That should all change when its Berlin Giga Factory begins production in July, 2021. This coupled with the Model Y introduction (it will be built in the Berlin factory) should mean a notable increase in sales as Europe returns to more normal times.

Model Y introduction: The Model Y, launched in early 2020 in the U.S., is already selling about 12,000 units a month here. This exceeds sales of crossover vehicles from every major brand (per GCBC which uses VIN reporting to calculate its numbers). It is expected to start being delivered in China in February.

Cybertruck: The Cybertruck (see our graphic here) was introduced to extremely mixed reactions. Traditionalists tended to hate it due to its radical departure from what they have come to expect for a pickup truck from companies like Ford, Toyota, etc. But it rang a cord with many and pre-orders are now up to 650,000 units according to Finbold. To give perspective on what this means, it is 30% higher than the total number of vehicles Tesla sold in 2020. While a portion of these orders could be cancelled as they only required a $100 deposit, the magnitude does imply significant incremental demand when Tesla launches in this category. The launch is expected late this year.

Roadster: Tesla has plans to re-introduce a Roadster in 2021. You may recall that the first Tesla’s were sports cars and are now collectors’ cars mostly valued between $50,000 and $70,000 but now the last one built, having about 200 miles on it is up for sale at $1.5 million. This time around it will make it an ultra-premium vehicle in specifications and in price. The base price Tesla has indicated starts at $200,000. A “Founders Series” will be $50,000 higher (with only 1,000 of those available). At those prices, gross margins should be quite high. The range Tesla initially indicated for this car was 620 miles and the speed from 0 to 60 of 1.9 seconds which would be much quicker than the McLaren 570S gas powered auto.

Tesla Semi: of all the vehicle categories that would benefit from being battery powered I believe the Semi is on top. That is because cost of ownership is one of the highest priorities for vehicles used in commerce. And Tesla claims that their semi will offer the lowest cost of ownership due to economic cost of fuel, less maintenance required as it has fewer parts, and easier repairs. According to Green Car Reports Musk has said it will begin being produced in 2021. Even assuming that Elon’s optimism is off, it appears that it could hit the market in early 2022. Once a definite date and specs are public, sales forecasts for Tesla could rise in 2022.

I’ve taken more time than usual to review my thoughts on Tesla as its astounding stock appreciation in 2020 make it vulnerable to stock pullbacks of some magnitude from time to time. But, its potential to achieve meaningful share of overall auto sales as various geographies shift to battery powered vehicles gives it the potential to achieve high growth in revenue for many years to come.

2. DocuSign stock appreciation will continue to outperform the market (it closed last year at $222/share)

DocuSign is the runaway leader in e-signatures facilitating multiple parties signing documents in a secure, reliable way for board resolutions, mortgages, investment documents, etc. Being the early leader creates a network effect, as hundreds of millions of people are in the DocuSign e-signature database. The company has worked hard to expand its scope of usage for both enterprise and smaller companies by adding software for full life-cycle management of agreements. This includes the process of generating, redlining, and negotiating agreements in a multi-user environment, all under secure conditions. On the small business side, the DocuSign product is called DocuSign Negotiate and is integrated with Salesforce.

DocuSign was another beneficiary of the pandemic as it helped speed the use of eSignature technology. The acceleration boosted revenue growth to 53% YoY in Q3, 2021 (the quarter ended on October 31, 2020) from 39% in Fiscal 2020. Total customers expanded by 46% to 822,000. At the same time Net Retention (dollars spent by year-ago customers in Q3 FY21 vs dollars spent by the same customers a year earlier) was 122% in the quarter. Non-GAAP gross margin remained at 79% as increased usage per customer (due to the pandemic) had minimal impact on cost. Given DocuSign’s strong Contribution Margin, operating profits increase faster than revenue and were up to $49 million from $17 million in the year ago quarter. What has happened represents an acceleration of the migration to eSignature technology which will be the base for DocuSign going forward. Once a company becomes a customer, they are likely to increase their spend, as evidenced by 122% Net Revenue growth. Finally, competition appeared to weaken as its biggest competitor, Adobe, lost considerable ground. This all led to a sizable stock gain of 200% to $222/share at year end. In my view, the primary risk is around valuation but at 50% growth this gets mitigated as earnings should grow much faster than revenue. I continue to believe the stock will appreciate faster than the S&P.

3. Stitch Fix Stock appreciation will continue to outperform the market (it closed last year at $58.72/share)

Stitch Fix offers customers, who are primarily women (although its sales in Men’s clothing is rising), the ability to shop from home by sending them a box with several items selected based on sophisticated analysis of their profile and prior purchases. The customer pays a $20 “styling fee” for the box which can be applied towards purchasing anything in the box. The company is the strong leader in the space with revenue at nearly a $2 billion run rate. The stock had a strong finish to 2020 after declining substantially earlier in the year due to Covid negatively impacting performance. This occurred despite gaining market share as people simply weren’t buying a normal amount of clothes at the onset of the pandemic. When revenue growth rebounded in the October quarter to 10% YoY and 7% sequentially the stock gained significant ground and closed the year up 129%.

Stitch Fix continues to add higher-end brands and to increase its reach into men, plus sizes and kids. Its algorithms to personalize each box of clothes it ships keeps improving. It appears to be beyond the worst days of the pandemic and expects revenue growth to return to a more normal 20-25% for fiscal 2021 (ending in July). This is partially due to easy comps in Q3 and Q4 and partly due to clothing purchase behavior improving. The company will also be a beneficiary of a number of closures of retail stores.

Assuming it is a 20-25% growth company that is slightly profitable, it still appears under-valued at roughly 3X expected Q2 annualized revenue. As a result, I continue to recommend it.

4. Amazon stock will outpace the market (it closed last year at $3257/share).

Amazon shares increased by 76% last year while revenue in Q3 was up 37% year over year (versus 21% in 2019). This meant the stock performance exceeded revenue growth as its multiple of revenue expanded in concert with the increased revenue growth rate. Net Income grew 197% YoY in the quarter as the leverage in Amazon’s model became apparent despite the company continuing to have “above normal” expenditures related to Covid. We expect the company to continue at elevated revenue and earnings growth rates in Q4 and Q1 before reaching comps with last year’s Covid quarters. Once that happens growth will begin to decline towards the 20-25% level in the latter half of 2021.

What will remain in place post-Covid is Amazon’s dominance in retail, leading share in Web Services and control of the book industry. Additionally, Amazon now has a much larger number of customers for its Food Services than prior to the pandemic. All in all, it will likely mean that the company will have another strong year in 2021 with overall growth in the 25-30% range for the year and earnings growing much faster. But remember, the degree earnings grow is completely under Amazon’s control as they often increase spend at faster rates than expected, especially in R&D.

5. Zoom Video Communications will continue to outperform the market (it closed last year at $337/share)

When I began highlighting Zoom in my post on June 24, 2019, it was a relatively unknown company. Now, it is a household name. I’d like to be able to say I predicted that, but it came as a surprise. It was the pandemic that accelerated the move to video conferencing as people wanted more “personal contact” than a normal phone call and businesses found it enhanced communications in a “work at home world”. Let me remind you what I saw in Zoom when I added it to the list last year, while adding some updated comments in bold:

At the time, Revenue retention of business customers with at least 10 employees was about 140%. In Q3, FY 2021 revenue retention of business customers was still 130% despite pandemic caused layoffs.

It acquires customers very efficiently with a payback period of 7 months as the host of a Zoom call invites various people to participate in the call and those who are not already Zoom users can be readily targeted by the company at little cost. Now that Zoom is a household name, acquiring customers should be even less costly.

At the time, Gross Margins were over 80% and I believed they could increase. In Q3, GM had declined to 68% as usage increased dramatically and Zoom made its products available to K-12 schools for free. Given that students were all mostly attending school virtually, this is a major increase in COGs without associated revenue. When the pandemic ends gross margins should return close to historic levels – adding to Zoom profits.

The product has been rated best in class numerous times

Its compression technology (the key ingredient in making video high quality) appears to have a multi-year lead over the competition

Adding to those reasons I noted at the time that ZM was improving earnings and was slightly profitable in its then most recent reported quarter. With the enormous growth Zoom experienced it has moved to significant profitability and multiplied its positive cash flow.

While ZM stock appreciated 369% in 2020, it actually was about equal to its revenue growth rate in Q3 2020, meaning that the price to revenue was the same as a year earlier before despite:

Moving to significant profitability

Becoming a Household name

Having a huge built-in multiplier of earnings as schools re-open

6. CrowdStrike will outperform the market (it closed 2020 at $211/share and is now at 217.93)

When I evaluate companies, one of the first criteria is whether their sector has the wind behind its back. I expect the online security industry to not only grow at an accelerated pace but also face an upheaval as more modern technology will be used to detect increased attacks from those deploying viruses, spam, intrusions and identity theft. I suspect all of you have become increasingly aware of this as virus after virus makes the news and company after company reports “breaches” into their data on customers/users.

The U.S. cyber security market was about $67 billion in 2019 and is forecast to grow to about $111 billion by 2025 (per the Business Research Company’s report). Yet Cloud Security spend remains at only about 1.1% of total Cloud IT spend (per IDC who expects that percent to more than double). CrowdStrike is the player poised to take the most advantage of the shift to the cloud and the accompanying need for best-in-class cloud security. It is the first Cloud-Native Endpoint Security platform. As such it is able to monitor over 4 trillion signals across its base of over 8500 subscription customers. The companies leading technology for modern corporate systems has led to substantial growth (86% YoY in its October quarter). It now counts among its customers 49 of the Fortune 100 and 40 of the top global 100 companies.

Tactically, the company continues to add modules to its suite of products and 61% of its customers pay for 4 or more, driving solid revenue retention. The company targets exceeding 120% of the prior year’s revenue from last year’s cohort of customers. They have succeeded in this for 8 quarters in a row through upselling customers combined with retaining 97% – 98% of them. Because of its cloud approach, growing also has helped gross margins grow from 55% in FY 18 to 66% in FY 19 to 72% in FY 20 and further up to 76% in its most recent quarter. This, combined with substantial improvement in the cost of sales and marketing (as a % of revenue) has in turn led to the company going from a -100% operating margin in Fiscal 2018 to +8% in Q3, FY21. It seems clear to me that the profit percentage will increase dramatically in FY22 given the leverage in its model.

Non-Stock Picks for 2021

7. Online Advertising Companies will Experience a Spike in Growth in the Second Half of 2021

The pandemic hit was devastating for the travel industry, in-person events and associated ticket sellers, brick and mortar retailers and clothing brands. Rational behavior necessitated a dramatic reduction of advertising spend for all those impacted. U.S. advertising revenue declined by 4.3% to $213 billion, or around 17% according to MagnaGlobal, if one excludes the jump in political advertising (discussed in our last post), with Global spend down 7.2%. That firm believes digital formats grew revenue about 1% in 2020 (with TV, radio and print declining more than average). Digital formats would normally be up substantially as they continue to gain share, so the way to think about this is that they experienced 10-20% less revenue than would have occurred without Covid.

Assuming things return to normal in H2 2021, digital advertising will continue to gain share, total industry revenue will be higher than it would have been without Covid (even without the increased political spending in 2020) and comps will be easy ones in H2 of 2021. While there will not be major political spending there could be Olympic games which typically boost ad spend. So, while we removed Facebook from our 6 stock picks, it and other online players should be beneficiaries.

8. Real Estate will Show Surprising Resiliency in 2021

The story lines for Real Estate during the pandemic have been:

The flight to larger outside space has caved urban pricing while driving up suburban values

Commercial real estate pricing (and profits) is collapsing, creating permanent impairment in their value for property owners with post-pandemic demand expected to continue to fall

My son Matthew is a real estate guru who has consulted to cities like New York and Austin, to entities like Burning Man and is also a Professor of Real Estate Economics at NYU. I asked him to share his thoughts on the real estate market.

Both Matthew (quoted below) and I disagree with the story lines. I believe a portion of the thinking regarding commercial real estate pricing relates to the collapse of WeWork. That company, once the darling of the temporary rental space, had a broken IPO followed by a decline in value of nearly 95%. But the truth is that WeWork had a model of committing to long term leases (or purchasing property without regard to obtaining lowest cost possible) and renting monthly. Such a company has extreme risk as it is exposed to downturns in the business cycle where much of their business can disappear. Traditional commercial property owners lease for terms of 5 to 25 years, with 10-15 years being most common, thus reducing or even eliminating that risk as leases tend to be across business cycles. The one area where both Matthew and I do believe real estate could be impacted, at least temporarily, is in Suburban Malls and retail outlets where Covid has already led to acceleration of bankruptcies of retailers a trend I expect to continue (see prediction 10).

The rest of this prediction is a direct quote from Matthew (which I agree with).

“Real estate in 2021 will go down as the year that those who do not study history will be doomed to repeat it. The vastly overblown sentiments of the “death of the city” and the flight to the suburbs of households and firms will be overshadowed by the facts.

In the residential world, while the market for rentals may have somewhat softened, no urban owners have been quick to give up their places, in fact, they turned to rent them even as they buy or rent roomier locations within the city or additional places outside the cities, driving up suburban prices more quickly. In fact, even in markets such as NYC, per square foot housing sale prices are stable or rising. US homebuilding sentiment is the highest in 35 years, with several Y/Y growth statistics breaking decades long records leading up to a recent temporary fizzle due to political turmoil.

The commercial office world, which many decry as imminently bust due to the work at home boom, has seen a slowdown of new leases signed in some areas. But because most commercial office leases are of a 10–15-year term, a single bad year has little effect. While some landlords will give concessions today for an extended term tomorrow, their overall NPV may remain stable or even rise. In the meantime, tech giants like Amazon are gobbling up available space in the Seattle and Bellevue markets, and Facebook announced a 730,000 square foot lease in midtown Manhattan late in the year. In the end, the persistence of cities as clusters of activity that provide productivity advantages to firms and exceptional quality of life, entertainment options, restaurants and mating markets to individuals will not diminish. The story of cities is the story of pandemic after pandemic, each predicting the death of the city and each resulting in a larger, denser, more successful one.

The big story of real estate in 2021 will be the meteoric rise of industrial, which began pre-COVID and was super charged as former in-person sales moved to online and an entire holiday season was run from “dark stores” and warehouses. The continual build out of the last mile supply chain will continue to lower the cost of entry for retailers to accelerate cheaper delivery options. This rising demand for industrial will continue the trend of the creation of “dark stores” which exist solely as shopping locations for couriers, Instacart, Whole Foods and Amazon. Industrial is on the rise and the vaccine distribution problems will only accelerate that in 2021.”

9. Large Brick and Mortar Retailers will continue their downward trend with numerous bankruptcies and acquisitions by PE Firms as consumer behavior has permanently shifted

While bankruptcies are commonplace in the retail world, 2020 saw an acceleration and there was a notable demise of several iconic B&M (Brick & Mortar) brands, including:

It is important to understand that a bankruptcy does not necessarily mean the elimination of the entity, but instead often is a reorganization that allows it to try to survive. Remember many airlines and auto manufacturers went through a bankruptcy process and then returned stronger than before. Often, as part of the process, a PE firm will buy the company out of bankruptcy or buy the brand during the bankruptcy process. For example, JC Penny filed for bankruptcy protection in May, 2020 and was later acquired by the Simon Property Group and Brookfield Property Partners in September, 2020. Nieman Marcus was able to emerge from bankruptcy protection without being acquired. However, in both cases, reorganizing meant closing numerous stores.

There are many who believe things will: “go back to normal” once the pandemic ends. I believe this could not be further from the truth as consumer behavior has been permanently impacted. During the pandemic, 150 million consumers shopped online for the first time and learned that it should now be part of how they buy. But, even more importantly, those who had shopped online previously became much more frequent purchasers as they came to rely on its advantages:

Immediate accessibility to what you want (unlike out of stock issues in Brick and Mortar retail)

Fast and Free shipping in most cases

A more personalized experience than in store purchasing

As older Brick & Mortar brands add online shopping to their distribution strategy, most are unable to offer the same experience as online brands. For example, when you receive a package from Peloton the unboxing experience is an absolute delight, when you receive one from Amazon it is perfectly wrapped. On the other hand, I have bought products online from Nieman Marcus, an extremely high-end retailer, and the clothes seemed to be tossed into the box, were creased and somewhat unappealing when I opened the box. Additionally, a company like Amazon completely understands the importance of customer retention and its support is extraordinary, while those like Best Buy that offer online purchasing fall far of the bar set by Amazon.

What that all means is that many Brick and Mortar retailers will not solve their issues:

Adding more of an online push will not be enough

Customers that have experienced the benefits of online purchasing will continue to use it in much greater amounts than before the pandemic

Ecommerce will continue to take share from Brick and Mortar stores

As a result, we believe that in 2021 the strain on physical retail will continue, resulting in many more well-known (and lesser known) store chains and manufacturing brands filing for bankruptcy as the dual issues of eCommerce and of the pandemic keeping stores closed and/or operating at greatly diminished customer traction throughout most of the year. Coming on the heels of a disastrous 2020 it will be harder for many of them to even emerge from bankruptcy after reorganizing (including closing many stores).

10. The Warriors will make the playoffs this Year

I couldn’t resist including one fun pick. We did speak about this in our last post but wanted to include it as an actual 2021 pick. Many pundits had the Warriors as dead before this season began once Klay Thompson was injured. And, of course, more piled on when the team lost its first 2 games by large margins. But they were mis-analyzing several significant factors:

Steph Curry is still Steph Curry at his peak no matter who the supporting cast

Andrew Wiggins is a superior talent who has the ability to shine on both offense and defense now that he is no longer in a sub-optimal Minnesota environment

Kelly Oubre Jr is also talented enough to be a great defender. His offense, while poor so far, is well above average and over the course of the season that should show well

Draymond Green is in his prime and remains one of the top defenders in the league. He is also a great facilitator on the offensive end of the floor.

James Wiseman is a phenomenon with the talent to be a star. As the season progresses, I expect him to continue to get better and become a major factor in Warrior success

Eric Pascal was on the all-rookie team last year and has gotten better

It is clear that the team needs more games to get Curry and Green back into peak playing condition, Wiseman to gain experience and the Warriors to become acclimated to playing together. They have started to show improved defense but still need time to develop offensive rhythm. I expect them to be a major surprise this year and make the playoffs.

SoundBytes

Please Wear A Mask: I recently read a terrific book describing the 1918 flu pandemic called The Great Influenzaby John Barry. That pandemic was much deadlier than the current one, with estimates of the number of people it killed ranging from 35 million to 100 million when the world population was less than 25% of what it is today. What is so interesting is how much the current situation has replicated the progress of that one. One of the most important conclusions Barry draws from his extensive study of the past is that wearing a mask is a key weapon for reducing the spread.

This may seem like a repeat of what you have heard from me in the past, but I enter each year with some trepidation as my favored stocks are high beta and usually had increased in value the prior year (in 2019 they were up about 46% or nearly double the S&P which also had a strong year). The fact is: I’m typically nervous that somehow my “luck” will run out. But, in 2020 I was actually pretty confident that my stock picks would perform well and would beat the market. I felt this confidence because the companies I liked were poised for another very strong growth year, had appreciated well under their growth over the prior 2-year period and were dominant players in each of their sub-sectors. Of course, no one could foresee the crazy year we would all face in 2020 as the worldwide pandemic radically changed society’s activities, purchasing behavior, and means of communication. As it turns out, of the 6 stocks I included in my top ten list 3 were beneficiaries of the pandemic, 2 were hurt by it and one was close to neutral. The pandemic beneficiaries experienced above normal revenue growth and each of the others faired reasonably well despite Covid’s impact. The market, after a major decline in March closed the year with double digit gains. Having said all that, I may never replicate my outperformance in 2020 as the 6 stocks had an average gain of an astounding 259% and every one of them outperformed the S&P gain of 14.6% quite handily.

Before reviewing each of my top ten from last year, I would like to once again reveal long term performance of the stock pick portion of the top ten list. I assume equal weighting for each stock in each year to come up with performance and then compound the yearly gains (or losses) to provide the 7-year performance. I’m comparing the S&P index at December 31 of each year to determine annual performance. Soundbyte’s compound gain for the 7-year period is 2049% which equates to an IRR of 55.0%. The S&P was up 106.1% during the same 7-year period, an IRR of 10.9%.

2020 Non-Stock Top Ten Predictions also Impacted by Covid

The pandemic not only affected stock performance, it had serious impact on my non-stock predictions. In the extreme, my prediction regarding the Warriors 2020-2021 season essentially became moot as the season was postponed to start in late December…so had barely over a week of games in the current year! My other 3 predictions were all affected as well. I’ll discuss each after reviewing the stock picks.

The 2020 Stocks Picked to Outperform the Market (S&P 500)

Tesla Stock which closed 2019 at $418/share and split 5 for 1 subsequently

Facebook which closed 2019 at $205/share

DocuSign which closed 2019 at $74/share

Stitch Fix which closed 2019 at $25.66/share

Amazon which closed 2019 at $1848/share

Zoom Video Communications which closed 2019 at $72.20/share

In last year’s recap I noted 3 of my picks had “amazing performance” as they were up between 51% and 72%. That is indeed amazing in any year. However, 2020 was not “any year”. The 6 picks made 2019 gains look like chopped liver as 4 of my 6 picks were up well over 100%, a 5th was up over 70% and the last had gains of double the S&P. In the discussion below, I’ve listed in bold each of my ten predictions and give an evaluation of how I fared on each.

1. Tesla stock appreciation will continue to outperform the market (it closed last year at $418/share). Note that after the 5 for 1 split this adjusts to $84.50/share.

In 2020, Tesla provided one of the wildest rides I’ve ever seen. By all appearances, it was negatively impacted by the pandemic for three reasons: people reduced the amount they drove thereby lessening demand for buying a new vehicle, supply chains were disrupted, and Tesla’s Fremont plant was forced to be closed for seven weeks thereby limiting supply. Yet the company continued to establish itself as the dominant player in electronic, self-driving vehicles. It may have increased its lead in user software in its cars and it continued to maintain substantial advantages in battery technology. The environment was also quite favorable for a market share increase of eco-friendly vehicles.

Additionally, several other factors helped create demand for the stock. The 5 for 1 stock split, announced in August was clearly a factor in a 75% gain over a 3-week period. Inclusion in the S&P 500 helped cause an additional spike in the latter part of the year. Tesla expanded its product line into 2 new categories by launching the Model Y, a compact SUV, to rave reviews and demonstrating its planned pickup truck (due in late 2021) as well. While the truck demo had some snags, orders for it (with a small deposit) are currently over 650,000 units.

All in all, these factors led to Tesla closing the year at $706/share, post-split, an astounding gain of 744% making this the largest one year gain I’ve had in the 7 years of Soundbytes.

2. Facebook Stock will outpace the market (it closed 2019 at $205 per share)

Facebook was one of the companies that was hurt by the pandemic as major categories of advertising essentially disappeared for months. Among these were live events of any kind and associated ticketing company advertising, airlines and cruise lines, off-line retail, hotels, and much more. Combine this with the company’s continued issues with regulatory bodies, its stock faced an uphill battle in 2020. What enabled it to close the year at $273 per share, up 33% (over 2x the S&P), is that its valuation remains low by straight financial metrics.

3. DocuSign stock appreciation will continue to outperform the market (it closed 2019 at $74/share)

DocuSign was another beneficiary of the pandemic as it helped speed the use of eSignature technology. The acceleration boosted revenue growth to 53% YoY in Q3, 2021 (the quarter ended on October 31, 2020) from 39% in Fiscal 2020. Since growth typically declines for high-growth companies this was significant. Investors also seemed to agree with me that the company would not lose the gains when the pandemic ends. Further, DocuSign expanded its product range into contract life-cycle management and several other categories thereby growing its TAM (total available market). Despite increased usage, DocuSign COGs did not rise (Gross Margin was 79% in Q3). Finally, competition appeared to weaken as its biggest competitor, Adobe, lost considerable ground. This all led to a sizable stock gain of 200% to $222/share at year end.

4. Stitch Fix stock appreciation will continue to outperform the market (it closed 2019 at $25.66/share)

Stitch Fix had a roller coaster year mostly due to the pandemic driving people to work from home, which led to a decline in purchasing of clothes. I’m guessing many of you, like me, wear jeans and a fleece or sweatshirt most days so our need for new clothes is reduced. This caused Stitch Fix to have negative growth earlier in the year and for its stock to drop in price over 50% by early April. But, the other side of the equation is that brick and mortar stores lost meaningful share to eMerchants like Stitch Fix. So, in the October quarter, Stitch Fix returned to growth after 2 weak quarters caused by the pandemic. The growth of revenue at 10% YoY was below their pre-pandemic level but represented a dramatic turn in its fortunes. Additionally, the CEO guided to 20-25% growth going forward. The stock reacted very positively and closed the year at $58.72/share up 129% for the year.

5. Amazon stock strategy will outpace the market (it closed last year at $1848/share)

Amazon had a banner year in 2020 with a jump in growth driven by the pandemic. Net sales grew 37% YoY in Q3 as compared to an approximate 20% level, pre-pandemic. Their gains were in every category and every geography but certainly eCommerce led the way as consumers shifted more of their buying to the web. Of course, such a shift also meant increased growth for AWS as well. Net Income in Q3 was up 197% YoY to over $6.3 billion. Given the increase in its growth rate and strong earnings the stock performed quite well in 2020 and was up 76% to $3257/share.

In our post we also recommended selling puts with a strike price of $1750 as an augmented strategy to boost returns. Had someone done that the return would have increased to 89%. For the purposes of blog performance, I will continue to use the stock price increase for performance. Regardless, this pick was another winner.

6. I added Zoom Media to the list of recommended stocks. It closed 2019 at $72.20

When I put Zoom on my list of recommended stocks, I had no idea we’d be going through a pandemic that would turn it into a household name. Instead, I was confident that the migration from audio calls to video conference calls would continue to accelerate and Zoom has the best product and pricing in the category. For its fiscal 2020-year (ending in January, 2020) Zoom grew revenue 78% with the final sequential quarter of the year growth at 13.0%. Once the pandemic hit, Zoom sales accelerated greatly with the April quarter up 74% sequentially and 169% YoY. The April quarter only had 5 weeks of pandemic benefit. The July quarter had a full 3 months of benefit and increased an astounding 102% sequentially and 355% YoY. Q3, the October quarter continued the upward trend but now had a full quarter of the pandemic as a sequential compare. So, while the YoY growth was 367%, the sequential quarterly growth began to normalize. At over 17% it still exceeded what it was averaging for the quarters preceding the pandemic but was a disappointment to investors and the stock has been trading off since reporting Q3 numbers. Regardless of the pullback, the stock is ahead 369% in 2020, closing the year at $337/share .

In the post we also outlined a strategy that combined selling both put and call options with purchasing the stock. Later in the year we pointed out that buying back the calls and selling the stock made sense mid-year if one wanted to maximize IRR. If one had followed the strategy (including the buyback we suggested) the return would still have been well over a 100% IRR but clearly lower than the return without the options. As with Amazon, for blog performance, we are only focused on the straight stock strategy. And this recommendation turned out to be stellar.

Unusual Year for the Non-Stock Predictions

7. The major election year will cause a substantial increase in advertising dollars spent

This forecast proved quite valid. Michael Bloomberg alone spent over $1 billion during his primary run. The Center for Responsive Politics reported that they projected just under $11 billion in spending would take place between candidates for president, the Senate and the House in the general election. This was about 50% higher than in 2016. Additionally, there will be incremental dollars devoted to the runoff Senate races in Georgia. This increase helped advertising companies offset some of the lost revenue discussed above.

8. Automation of Retail will continue to gain momentum

Given the pandemic, most projects were suspended so this did not take place. And it may be a while before we have enough normalization for this trend to resume, but I am confident it will. However, the pandemic also caused an acceleration in eCommerce for brick and mortar supermarkets and restaurants. I’m guessing almost everyone reading this post has increased their use of one or more of: Instacart, Amazon Fresh, Walmart delivery, Safeway delivery, Uber Eats, GrubHub, Doordash, etc. My wife and I even started ordering specialty foods (like lox) from New York through either Goldbelly or Zabars. Restaurants that would not have dreamed of focusing on takeout through eCommerce are now immersed in it. While this was not the automation that I had contemplated it still represents a radical change.

9. The Warriors will come back strong in the 2020/2021 season