Mike Kwatinetz is a Founding General Partner at Azure Capital Partners and a Venture Capitalist investing in application software (SaaS), ecommerce, consumer web and infrastructure technology companies. Successful exits include: Bill Me Later, VMware, TripIt and Top Tier.

Our predictions for 2023 were all fulfilled with the stock portion providing extremely strong performance. This was on the heels of poor performance in 2022 as it was one of the worst years in the past 50 for the stock market in general, and for my stocks in particular. In delineating the stock recommendations in our Top Ten predictions for 2023 we pointed out that the 6 stocks, on average had fallen nearly 49% in 2022 despite average revenue growth of about 38%. Since we expected all 6 to continue to grow in 2023 (and both Amazon and Shopify to increase their growth rates), we felt they were all poised for a recovery. This clearly proved accurate.

What went right for my stock picks in 2023 was great company results coupled with the benefit of an apparent end to the rate hike cycle. I have always pointed out that I am not amongst the best at forecasting the market as a whole but have been very strong at selecting great companies which over the long term (5 years or more) typically have solid stock appreciation if their operating performance is consistently good. But even great company’s stock performance can be heavily impacted in any given year by market conditions. Two key drivers of negative market conditions in 2022 were the huge spike in inflation coupled by the Fed raising rates to battle it.

At the beginning of 2023 we felt that inflation would be on the decline from its peak of 9.1% in June 2022 (see prediction 9). Given the expected decline in inflation we believed the Fed would slow and then stop increasing interest rates. Since the rise in interest rates was a major reason for the decline in our long-duration stocks, we believed that slowing and then stopping this rise would be a factor in driving elevated stock performance.

So, the big question for the market at the beginning of 2023 was whether the expected additional rate increases projected at just under 1% for the year (which theoretically was built into share prices at the end of 2022) would be enough for The Fed. It pretty much was as the Fed raised rates 1.0% during the year but stopped making increases after July and subsequently indicated that rates could start declining in 2024.

Stocks reacted well to what appears to be end of the upward climb in rates and tech stocks reacted particularly well as long duration investments tend to be influenced greatly by rate changes. Coupling this with what appears to be a soft landing created a positive environment for our recommended stocks.

Our six recommended stocks were up an average of 96% with 3 of the 6 appreciating over 100%. While we will have a longer discussion of the reasoning behind it in our next post, we wanted to disclose that all 6 will be recommendations in our 2024 Top Ten.

2023 Stock Recommendations

Tesla will outperform the market (it closed 2022 at $123.18/share)

As usual, Tesla was a wild ride in 2023. Partly, this was based on continued controversy surrounding Elon especially his actions post his October 2022 purchase of Twitter (now called X). But in addition, concerns over price drops, potential slowing momentum of Battery Electric Vehicles, challenges to Tesla market share and more weighed on the stock at times. These concerns buried the stock in 2022. In 2023 they continued to be sighted by shorts but proved overblown as the company reached its unit sales target of 1.8 million vehicles (up 40%), launched the CyberTruck in Q4 and substantially increased its market share of overall vehicles sold. As a result, Tesla stock was very strong in 2023 and closed the year at $248.48/share, a rise of 102%.

2. CrowdStrike (Crwd) will outperform the market (it closed 2022 at $105.29/share)

The most recently reported quarter for CrowdStrike, Q3 FY24 was another strong one as the pandemic had little impact on its results. Revenue was up over 35% and earnings 105%. Existing customers continued to expand use of the company’s products driving Net Revenue Retention to exceed 120% for the 20th consecutive quarter. The company’s stock, which had declined nearly 50% in 2022 (despite a revenue increase of 54%), had a dramatic recovery. It closed 2023 at $255.17/share, up 142%.

3. Amazon will outperform the market (it closed 2022 at $84.00/share)

As we expected, Amazon improved revenue growth in each quarter of 2023 from its low point of 8.6% in Q4 2022. In Q3 2023 growth was back to 12.6%. Additionally, the company increased its focus on profitability with Q3 profits up well over 200% versus the prior year’s weak numbers. This coupled with the improved environment for tech stocks helped drive Amazon’s share price to $151.75 at year end, up 81% from the close on December 31, 2022.

4. The Trade Desk (TTD) will outperform the market (it closed 2022 at $44.83/share)

Fears of a potential recession caused great concern for advertising revenue. After dropping sequentially in Q4 2022 (to 24.1%) and again in Q1 2023 (to 21.5%) TTD’s revenue growth began recovering in Q2 (to 23.1%) and again in Q3 (to 27.7%). The stock reacted well to the improvement and closed 2023 at $71.80 up 60% from year end 2022.

5. Datadog will outperform the market (it closed 2022 at $73.50/share)

Like many other high growth subscription-based software companies, Datadog experienced another solid year in 2023 with Q3 revenue growth at 26.7%. Also, like CrowdStrike, Datadog has a very high gross margin (GM) and is now at the point where it has started to leverage its GM driving up earnings (+96%) at a much faster rate than revenue. This level of success helped Datadog stock close the year at $121.65/share, up 66%.

6. Shopify (Shop) will outperform the market (it closed at $34.71/share)

In our post of Top Ten predictions, we pointed out that the pandemic had created a major warping of Shop revenue growth. Instead of the normal decline for high growth companies from its 47% level in 2019 it jumped to 86% growth in 2020 and still was above “normal” at 57% in 2021. Once physical retail normalized in 2022, Shopify growth plunged against the elevated comps declining to a nadir of 16% in Q2, 2022. When we included Shop in our Top Ten for 2023, we pointed out that we expected its revenue growth to return to 20% or more throughout 2023. This indeed did occur and the stock reacted well, closing the year at $77.88 up 124% year/year.

Non-Stock Specific Predictions

While I usually have a wide spectrum of other predictions, last year I wanted to focus on some pressing issues for my 3 predictions that are in addition to the fun one. These issues are Covid, inflation and California’s ongoing drought. They have been dominating many people’s thoughts for the past 3 years or more.

7. The Warriors will improve in the second half of the current season and make the Playoffs

This forecast proved correct as I expected the Warriors to make the playoffs but be unsuccessful at winning a title. They did rally in the latter part of the season to finish 6th (avoiding the play-in) and won the series against the Kings but failed to progress to the Western Finals.

8. Desalination, the key to ending long term drought, will make progress in California

Some of the pressure to create desalination plants throughout California was reduced by substantial rainfall last year that ended the drought and filled reservoirs. Despite this there was progress as the California Coastal Commission approved a $140 million desalination plant in Orange County (at Dana point) in late 2022. Resistance to its construction has been mounted by environmental groups but in 2023 the planning continued to move forward.

In April 2023, the Department of Water Resources (DWR) announced 3 more projects that will receive support from DWR and an additional 6 projects that will receive funds through a partnership with the National Alliance for Water Innovation. While the total water generated through all projects currently approved is still far short of fulfilling California needs, the tide seems to have begun to turn (no pun meant) towards favoring use of desalination.

9. Inflation will continue to moderate in 2023

This forecast proved pretty accurate as inflation moderated to just over 3% in 2023 (very slightly higher than my projected range). It was at 6.3% when I made the forecast.

10. Covid’s Impact on society in the US will be close to zero by the end of 2023

I consider this prediction mostly right. On the positive side I believe Covid no longer has much influence on people venturing out to shop, dine, go to the theater, travel, etc. Even cruise lines are experiencing a substantial return towards normal. The number of new Covid cases has waned significantly and deaths from it are close to zero. However, I would not say we’re quite at zero impact as there are still some spikes (of modest magnitude versus before) that cause concern to a portion of the population.

The past year has been extremely busy for me and the decline in blogs produced has been one of the consequences. On the one hand, I’m mortified that my annual Top Ten list has been delayed by 2 months. On the other hand, it turns out that the steep decline in tech valuations affords an opportunity for acquiring recommended stocks at much lower cost than they were on January 2. Because I don’t want to delay recommendations further, I am going to publish the recap of 2021 picks after the new Top Ten blog is out. Suffice it to say the recap will be of a down year after posting my best year ever in 2020, but that means (at least to me) that there is now an opportunity to build a portfolio around great companies at opportune pricing.

Starting in November of 2021 the Tech sector has taken a beating as inflation, potential interest rate spikes, the Russian threat to the Ukraine (followed by an invasion), a Covid jump due to Omicron and supply chain issues all have contributed to fear, especially regarding high multiple stocks. What is interesting is that the company performance of those I like continues to be stellar, but their stocks are not reflecting that. For 2022, the 6 stocks I’m recommending are Tesla, DocuSign, Amazon, Zoom, CrowdStrike and Shopify (the only new one on my list).

In the introduction to my picks last year, I pointed out that over time share appreciation tends to correlate to revenue growth. This clearly did not occur over the last 14 months as illustrated in Table 1.

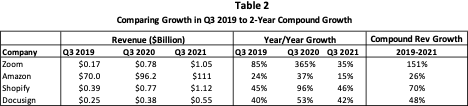

The average revenue gain in the last quarter reported by these companies was 43%, while the average stock in the group was down 17%. It should also be noted that Amazon reported that its major profit driver, AWS, had grown 40% while eCommerce had been relatively flat year over year and the stock reacted positively due to the AWS increase. Over time I expect share performance to be highly correlated to revenue growth, but clearly that has not been the case for the past 14 months. Shopify, Zoom, DocuSign and Amazon had revenue growth largely distorted by Covid, with 2020 growth being well above their norm and 2021 growth coming down dramatically. This caused their stocks to plummet as the interpretation of 2021 results was that long term growth had slowed. Yet in all cases the 2-year compound growth rate was well above the previous norm.

Table 2 highlights this abnormality.

In Q3 2019, Zoom’s revenue growth was 85%. Such a high rate of growth usually declines each year barring some abnormal situation. Instead, the growth rate soared in 2020 and the jump was followed by additional growth in 2021. The 2-year CAGR was 151% and Zoom had over 6 times the revenue in Q3 2021 than it did 2 years earlier. Yet, its share price is now roughly only 10% above where it was 2 years ago and down 63% from January 1, 2021. While Zoom is the most extreme situation of the four companies in Table 2, each of the other three have had a similar whipsaw of its revenue growth rate and in each case its stock soared in 2020 only to heavily trail revenue growth in 2021 despite its 2-year CAGR being above pre-pandemic levels in every case. While revenue growth at Tesla and CrowdStrike were not impacted in a similar way by the pandemic as both had more normal revenue growth patterns in 2020 and 2021, they still saw share performance significantly trail revenue growth for the past year.

Given the compression in revenue multiples across the board in tech stocks, the opportunity for investing appears timely to me. Of course, I cannot predict that the roughly 59% average decline in revenue multiple among these stocks represents the bottom…as I never know where the bottom is.

2022 Stock Recommendations (Note: base prices are as of February 25, 2022)

Tesla will continue to outperform the market (it closed at $810/share)

a. Tesla demand has far outstripped supply, as backlog increased steadily during 2021. And this is before the Cyber Truck with it’s over a million pre-orders, has come to market. This has been partly based on a substantial surge in demand and partly due to a shortage of some parts. While Tesla has made and will continue to drive up capacity by launching multiple new factories, supply of parts has prevented the factories from operating at capacity. Rather than overspending to secure more supply (a major error by Peloton), Tesla has chosen to raise prices and to prioritize production of more expensive (and more profitable) versions of its products. As of December 31, wait times for the standard Model 3, Model Y and Model S were approximately 10-11 months while the more expensive high-performance version of each had delivery times of 2-3 months. For the Model X, delivery dates were even longer. As we forecast in prior letters, Tesla gross margins have been rising and in its most recently announced fourth quarter were the highest in the industry. Yet, we believe they will still go up from here as:

Tesla, like Apple did for phones, is increasing the high margin software and subscription components of sales;

the full impact of recent price increases is not yet in the numbers;

its factories are not yet operating at full efficiency; and

Tesla will have lower shipping cost to European buyers once the Berlin factory begins to ramp.

b. Cyber Truck preorders are now estimated at over 1.25 million units (approximately $79 billion in sales value) according to a fan tracker site, or 50% more potential revenue than 2021 total revenue. Obviously, some of the orders will be cancelled given the long wait times before delivery, but still, this virtually assures large revenue increases for 2022 and 2023, only gated by obtaining enough supply of parts. The Cyber Truck is not expected to ship until mid-2022 and is not material to meeting revenue forecasts for this year. The Tesla Semi appears close to being ready to go into production, but battery constraints will probably mean any deliveries will be truly minimal for Q1 (Pepsi expects to take delivery of at least 15 in the near term). The Berlin factory, a key to increasing its share in Europe, will likely begin manufacturing in the first half of 2022. What this all points to is high revenue growth continuing, stronger GMs in 2022, and earnings escalation likely faster than revenue growth. While revenue growth is gated by supply constraints it should still be quite strong. And the high backlog not only assures that 2023 will be another high growth year but also means there is little pressure on Tesla pricing.

Shopify will outperform the market (it closed at $677 per share)

Shopify, like Amazon, Zoom and DocuSign experienced elevated growth in 2020. This was due to Covid keeping people out of stores (many of which weren’t even open). If we look at pre-Covid growth the company’s revenue increased by 45% year/year in Q3 2019. A year later revenue growth had escalated to 96% due to Covid. In Q3 2021 growth was 46%, returning to pre-Covid levels. The compound 2-year rate of growth was 70%. If Shopify can continue at a 35-40% revenue growth rate it will mean it has absorbed its higher level of revenue and is growing quite nicely from there.

Shopify has established a clear leadership position as the enabler of eCommerce sites. Its U.S. eCommerce market share, at 10.3% in 2021, is second to Amazon and well ahead of its closest competitors Walmart, eBay, and Apple. Net revenue retention for the company continues to be well over 100% as Shopify has successfully expanded services it provides to its eCommerce business customers. Additionally, because successful eCommerce companies are growing, Shopify also grows its portion of the customer revenue it shares. I expect continued growth to be well over 30% for several more years given three things:

a. Ecommerce should continue to take share from offline.

b. We expect Shopify to continue to gain share of Ecommerce.

c. Shopify will leverage expanded services leading to higher revenue per client.

In 2022 revenue growth is expected to be lower in the first half of the year than the second due to the benefit Covid had on the first half of 2021 and some changes Shopify made in its method of charging customers that took effect in the second half of 2021.

CrowdStrike will outperform the market (it closed at $182 per share)

CrowdStrike continues to gain substantial share of the data security market. Given its leadership position in the newest technology coupled with what is still a modest share of its TAM, the company remains poised for continued high growth. This coupled with over 120% net revenue retention for 12 straight quarters (primarily driven by expanded module purchases) makes CrowdStrike a likely long-term grower at over 50% per year.

The recent threats by Russia to create a Cyber attack on the U.S. could be an additional boost to the entire security industry. CrowdStrike stands to be a disproportionate beneficiary as it has the most advanced technology for defending companies against such attacks.

Amazon will outperform the market (it closed at $3076 per share)

Amazon, like Shopify, benefitted from the substantial number of people who shopped from home in 2020. This caused an expansion of its growth rate from 24% in Q3 2019 to 37% in in Q3 2020. In Q3 2021 growth was down to 15% against the tough compare. Looking at the 2-year compound rate the company appears to have had a modest benefit to growth. We expect the company to return to a 15-20% growth rate in the second half of 2022. This would mean that it has absorbed extra revenue and returned to the normal curve of growth declining. One thing that helped the stock was that higher margin Amazon Web Services (AWS) grew at 40%, much higher than modestly profitable commerce. AWS continues to be quite attractive relative to its peers and its quality and sophistication continues to improve.

A second potential driver for the stock is that new CEO Jassy may decide to increase the focus on earnings growth which is available to Amazon if it chooses to do so. If he does that could be a catalyst to share appreciation. To that end, on the Q4 earnings call the company announced that it would be increasing the cost of Prime by about 17%. This increase will go into effect in Mid-February for new members and in Mid-March for existing members. The impact will roll out over 12 months as existing members renew their annual membership. Despite this increase, Prime remains a distinct bargain as it not only includes free shipping but also a number of other benefits such as video streaming of movies and TV shows, some free eBooks, discounts at Whole Foods and more. Given that Prime has over 200 million members, the increase adds over $4 billion to revenue once it fully rolls out or about 1% of revenue. While this may not appear to be that much, it is worth about $8 per share in pre-tax earnings.

DocuSign will outperform the market (it closed at $115 per share)

DocuSign experienced some of the up and down in growth that Zoom did but to a more moderate extent. Its “normal” pre-Covid growth rate of 40% in Q3 of fiscal 2020 escalated to 53% a year later and then fell back down to 42% in its last reported quarter. As with other high growth stocks DocuSign’s rate would normally have fallen, so the 2-year compound rate of 48% was quite strong. Yet, as I write this letter, the stock is down by over 50% in the past year despite revenue increasing by 42%. This means the multiple of revenue has fallen by about 64% in a year.

As is normal for high growth companies, I expect DocuSign to continue to have a modest decline in revenue escalation from last quarter but believe growth will continue to be above 30% for several years as net retention among enterprise customers (which is 88% of revenue) is over 120% and the company continues to add new customers to this group at a solid pace. DocuSign is the dominant player in the use of eSignature and other management tools for documents. The use of these tools will be just as important in a post-Covid world.

DocuSign continues to add initiatives to keep Net Retention at or near the 120% level. These include growing its partnership with Salesforce, launching a new release of its software, Agreement Cloud which in addition to eSignature also includes the full cycle of contract creation and management. The company is also working on creating an eNotary product.

Zoom will outperform the market (it closed at $125 per share)

Zoom is a company that has had its revenue trajectory impacted the most by Covid. Before the pandemic, the company was growing revenue at 80%+ in 2019. Such a high growth rate would normally decline the following year but when Covid struck Corporate demand increased by a higher rate than normal and individuals flocked to Zoom in order to maintain some visual contact with friends and family. As a result, Zoom growth peaked at an unheard of 365% in Q2 of fiscal 2021 (reported in calendar Q3 of 2020). As people subsequently began leaving their homes Zoom’s growth was impacted. The corporate side of its business continued to have robust growth with Net Revenue Retention of over 130% as business customers from a year earlier increasing their spend by over 30% including churns. In addition, Zoom had a net add of new customers of 18% of the prior year’s total. Putting those together means that revenue from business customers grew about 45% and continued to grow about 10% sequentially while growth of the consumer side was flattish to slightly down sequentially. Combining the two trends meant that overall growth fell to 35% year over year in Q3 of fiscal 2022 and is expected to decline further in Q4. Looking at the 2-year compound growth rate for revenue in Table 2, one can see that Zoom experienced an elevation to over 150%, nearly double their pre-covid level. We believe that over the longer run Zoom can grow over 30% once the corporate side of its business becomes a bit more dominant and the consumer side begins to show moderate sequential growth. And we expect that sequential growth will begin to rise at some point during calendar 2022 (its fiscal 2023).

GMs were over 81% in FY 2020 (ending January 31, 2020), pre-Covid. The impact of free use to schools with students being on Zoom 8 hours a day, a major expansion of consumer free users, plus paying users expanding use without generating extra revenue (there is no charge for increasing usage) caused GMs to decline to under 70% in FY 2021. By Q3 FY 2022 GM had returned to 76%. We believe further improvement in GMs is inevitable as Covid declines and usage rates diminish without impacting revenue. This should mean that earnings increase at a faster rate than revenue assuming the company keeps G&A growth at or lower than revenue growth.

2022 Non-Stock Invitations

Republicans will recapture at least one of the Senate and House in the Interim elections

Since the Biden administration has taken power, inflation has surged to its highest rate since the Carter administration, the Ukraine crisis has emerged, Covid cases have jumped and Biden leadership and mental sharpness have come into question. While several of these issues may have come to the front no matter who was president, an ABC News/Washington Post poll shows the electorate clearly is dissatisfied. Biden’s approval rating has fallen to 37% and people believe by over a 2 to 1 margin that the Republicans would do a better job handling the economy. The poll results show that if the House elections were held today, 49% would vote Republican and 42% Democrat. Given how tenuous the Democrats majority is, this would likely lead to a change of control. It is only late February so there is still time for this to change, but many of these issues, especially the economy, may be hard to turn before the November election.

The travel industry will experience robust growth starting in the summer of 2022

The travel industry has had a pretty rocky 2020 and 2021 as Covid elicited substantial fear of boarding a plane, traveling out of the country and/or taking a cruise. In 2021, we did see a return to travel within the U.S. and it was accompanied by increasing prices of hotel rooms and restaurants. It seems clear (to me at least) that people are worn down by Covid and appear ready to resume some of their prior vacation habits. While new Covid cases are still at very high levels (but falling rapidly), the current version is much less deadly than prior ones. In my group of friends, several of us have planned a trip to France in May which will be the first time back in Europe for any of the 4 couples since 2019. While I’m less certain of when cruise lines will be back to normal, I expect them to see some renaissance this year. The only fly in the ointment is how serious the Russian crisis becomes. As of now I believe it will be restricted (from a military point of view) to the Ukraine.

PG&E and other utility companies will battle to dramatically increase what they charge those who convert to solar

There is a massive conflict between the drive to replace energy received from the grid with solar panels. On the one hand the U.S. government provides a 26% tax rebate for installing solar panels. And states like California are pushing to drive more solar through a net metering law (and in the past tax rebates). Also, California is now mandating roof solar panels for all new homes. On the other hand, utility companies like the three in California are battling to increase charges to those that install solar as an offset to the revenue they would lose. The Solar Rights Alliance estimates that “going big on Solar” could save American households over $473 billion over 30 years, whereas “doubling down” on new powerline installation would add $385 billion in cost to American households. When a household converts to solar, energy companies lose revenue and these companies are intent on increasing the cost to solar users to offset this.

Net Metering means a household can sell back excess energy produced to their utility company, which in turn offsets any cost they incur on days when their solar falls short of needs and they need to buy from the utility. The dollars they were entitled to by selling back is then deducted from the bill for energy used. Before 2016 the price the utility company paid for the excess they bought was equal to the price they sold energy back to the consumer. As more homes installed solar the energy companies pushed for a change and in 2016 NEM 2.0 was passed. This allowed the utilities to charge $ 0.03 per kWh for power they sold back to consumers. It also added an interconnect fee of $145 or more to PG&E and different amounts for the other California utility companies. Further, it established a policy of varying rates based on the time of day (which meant higher charges on energy purchased during the middle of very hot days).

Still, as more and more households install solar (including all new homes), the utility companies view it their right to be able to increase charges so they can grow revenue. There has been a push before the California Public Utilities Commission to pass NEM 3.0. It would allow the 3 major utility companies to charge between $56 and $91/month to any home with a new installation of solar. Additionally, it would slash the credit for selling back energy. If it had passed this would have added significant cost to homes with solar and likely reduced the number of existing homes that install it by 70% or more. For now, the public furor over NEM 3.0 caused the PUC to postpone action on this indefinitely. Instead, a large rate increase was granted to PG&E to help pay for remediating their negligence that contributed to California fires. But this battle is far from over! I’m expecting some sort of political compromise on new charges to solar homes to occur when the furor dies down. It likely will lower the added charges from the prior proposal but still increase the cost. While I am predicting this increase in 2022, it may not happen until 2023.

If Green comes back at full capacity the Warriors will win the NBA Championship

As usual I had to have my one fun pick. Clearly this is not a “gimme” and maybe shows my fan bias. In fact, the Warriors have serious issues even getting to the championship game as the Suns have been playing great and Memphis is on the rise and easily could beat out the Warriors for second in the West. This means the Warriors could need to overcome home court advantages for each of those teams assuming each of the three wins in earlier rounds. But, before Green was injured, the Warriors were the top defensive team in the league and also playing quite well on offense and Klay Thompson had yet to play. Since his injury Kuminga has emerged as another strong cog in the Warrior wheel and Klay appears to be working towards his former production by the playoffs.

In last year’s top ten I pointed out that Wiggins was likely to shine for the Warriors and he has certainly done that on offense and defense this year. Despite a so-called slump, Curry is still the best shooter on the planet and will likely return to full form when Green returns as its no coincidence that his tail-off started under the pressure of breaking the 3-point scoring record but has mostly been with Green out. Poole has developed into a strong 6th man who is capable of providing a scoring boost when needed. Looney could benefit from a little easing of his minutes coming into the playoffs as he was playing his best basketball ever for most of the season. Iguodala should be very additive in the playoffs, assuming he is healthy. Finally, Gary Payton is a game changer on defense and Kerr has been using him very effectively.

I wanted to start this post by repeating something I discussed in my top ten lists in 2017 and 2018 which I learned while at Sanford Bernstein in my Wall Street days: “Owning companies that have strong competitive advantages and a great business model in a potentially mega-sized market can create the largest performance gains over time (assuming one is correct).” It does make my stock predictions somewhat boring (as they were on Wall Street where my top picks, Dell and Microsoft each appreciated over 100X over the ten years I was recommending them).

Let’s do a little simple math. Suppose one can generate an IRR of 26% per year (my target is to be over 25%) over a long period of time. The wonder of compounding is that at 26% per year your assets will double every 3 years. In 6 years, this would mean 4X your original investment dollars and in 12 years the result would be 16X. For comparison purposes, at 5% per year your assets would only be 1.8X in 12 years and at 10% IRR 3.1X. While 25%+ IRR represents very high performance, I have been fortunate enough to consistently exceed it (but always am worried that it can’t keep up)! For my recommendations of the past 6 years, the IRR is 34.8% and since this exceeds 26%, the 6-year performance is roughly 6X rather than 4X.

What is the trick to achieving 25% plus IRR? Here are a few of my basic rules:

Start with companies growing revenue 20% or more, where those closer to 20% also have opportunity to expand income faster than revenue

Make sure the market they are attacking is large enough to support continued high growth for at least 5 years forward

Stay away from companies that don’t have profitability in sight as companies eventually should trade at a multiple of earnings.

Only choose companies with competitive advantages in their space

Re-evaluate your choices periodically but don’t be consumed by short term movement

As I go through each of my 6 stock picks I have also considered where the stock currently trades relative to its growth and other performance metrics. With that in mind, as is my tendency (and was stated in my last post), I am continuing to recommend Tesla, Facebook, Amazon, Stitch Fix and DocuSign. I am adding Zoom Video Communications (ZM) to the list. For Zoom and Amazon I will recommend a more complex transaction to achieve my target return.

2020 Stock Recommendations:

1. Tesla stock appreciation will continue to outperform the market (it closed last year at $418/share)

Tesla is likely to continue to be a volatile stock, but it has so many positives in front of it that I believe it wise to continue to own it. The upward trend in units and revenue should be strong in 2020 because:

The model 3 continues to be one of the most attractive cars on the market. Electric Car Reviews has come out with a report stating that Model 3 cost of ownership not only blows away the Audi AS but is also lower than a Toyota Camry! The analysis is that the 5-year cost of ownership of the Tesla is $0.46 per mile while the Audi AS comes in 70% higher at $0.80 per mile. While Audi being more expensive is no surprise, what is shocking is how much more expensive it is. The report also determined that Toyota Camry has a higher cost as well ($0.49/mile)! Given the fact that the Tesla is a luxury vehicle and the Camry is far from that, why would anyone with this knowledge decide to buy a low-end car like a Camry over a Model 3 when the Camry costs more to own? What gets the Tesla to a lower cost than the Camry is much lower fuel cost, virtually no maintenance cost and high resale value. While the Camry purchase price is lower, these factors more than make up for the initial price difference

China, the largest market for electronic vehicles, is about to take off in sales. With the new production facility in China going live, Tesla will be able to significantly increase production in 2020 and will benefit from the car no longer being subject to import duties in China.

European demand for Teslas is increasing dramatically. With its Chinese plant going live, Tesla will be able to partly meet European demand which could be as high as the U.S. in the future. The company is building another factory in Europe in anticipation. The earliest indicator of just how much market share Tesla can reach has occurred in Norway where electric cars receive numerous incentives. Tesla is now the best selling car in that country and demand for electric cars there now exceeds gas driven vehicles.

While 2020 is shaping up as a stairstep uptick in sales for Tesla given increased capacity and demand, various factors augur continued growth well beyond 2020. For example, Tesla is only partway towards having a full lineup of vehicles. In the future it will add:

Pickup trucks – where pre-orders and recent surveys indicate it will acquire 10-20% of that market

A lower priced SUV – at Model 3 type pricing this will be attacking a much larger market than the Model X

A sports car – early specifications indicate that it could rival Ferrari in performance but at pricing more like a Porsche

A refreshed version of the Model S

A semi – where the lower cost of fuel and maintenance could mean strong market share.

2. Facebook stock appreciation will continue to outperform the market (it closed last year at $205/share)

Facebook, like Tesla, continues to have a great deal of controversy surrounding it and therefore may sometimes have price drops that its financial metrics do not warrant. This was the case in 2018 when the stock dropped 28% in value during that year. While 2019 partly recovered from what I believe was an excessive reaction, it’s important to note that the 2019 year-end price of $205/share was only 16% higher than at the end of 2017 while trailing revenue will have grown by about 75% in the 2-year period. The EPS run rate should be up in a similar way after a few quarters of lower earnings in early 2019. My point is that the stock remains at a low price given its metrics. I expect Q4 to be quite strong and believe 2020 will continue to show solid growth.

The Facebook platform is still increasing the number of active users, albeit by only about 5%-6%. Additionally, Facebook continues to increase inventory utilization and pricing. In fact, given what I anticipate will be added advertising spend due to the heated elections for president, senate seats, governorships etc., Facebook advertising inventory usage and rates could increase faster (see prediction 7 on election spending).

Facebook should also benefit by an acceleration of commerce and increased monetization of advertising on Instagram. Facebook started monetizing that platform in 2017 and Instagram revenue has been growing exponentially and is likely to close out 2019 at well over $10 billion. A wild card for growth is potential monetization of WhatsApp. That platform now has over 1.5 billion active users with over 300 million active every day. It appears close to beginning monetization.

The factors discussed could enable Facebook to continue to grow revenue at 20% – 30% annually for another 3-5 years making it a sound longer term investment.

3. DocuSign stock appreciation will continue to outperform the market (it closed last year at $74/share)

DocuSign is the runaway leader in e-signatures facilitating multiple parties signing documents in a secure, reliable way for board resolutions, mortgages, investment documents, etc. Being the early leader creates a network effect, as hundreds of millions of people are in the DocuSign e-signature database. The company has worked hard to expand its scope of usage for both enterprise and smaller companies by adding software for full life-cycle management of agreements. This includes the process of generating, redlining, and negotiating agreements in a multi-user environment, all under secure conditions. On the small business side, the DocuSign product is called DocuSign Negotiate and is integrated with Salesforce.

The company is a SaaS company with a stable revenue base of over 560,000 customers at the end of October, up well over 20% from a year earlier. Its strategy is one of land and expand with revenue from existing customers increasing each year leading to a roughly 40% year over year revenue increase in the most recent quarter (fiscal Q3). SaaS products account for over 95% of revenue with professional services providing the rest. As a SaaS company, gross margins are high at 79% (on a non-GAAP basis).

The company has now reached positive earnings on a non-GAAP basis of $0.11/share versus $0.00 a year ago. I use non-GAAP as GAAP financials distort actual results by creating extra cost on the P&L if the company’s stock appreciates. These costs are theoretic rather than real.

My only concern with this recommendation is that the stock has had a 72% runup in 2019 but given its growth, move to positive earnings and the fact that SaaS companies trade at higher multiples of revenue than others I still believe it can outperform this year.

4. Stitch Fix Stock appreciation will continue to outperform the market (it closed last year at $25.66/share)

Stitch Fix offers customers, who are primarily women, the ability to shop from home by sending them a box with several items selected based on sophisticated analysis of her profile and prior purchases. The customer pays a $20 “styling fee” for the box which can be applied towards purchasing anything in the box. The company is the strong leader in the space with revenue approaching a $2 billion run rate. Unlike many of the recent IPO companies, it has shown an ability to balance growth and earnings. The stock had a strong 2019 ending the year at $25.66 per share up 51% over the 2018 closing price. Despite this, our valuation methodology continues to show it to be substantially under valued and it remains one of my picks for 2020. The likely cause of what I believe is a low valuation is a fear of Amazon making it difficult for Stitch Fix to succeed. As the company gets larger this fear should recede helping the multiple to expand.

Stitch Fix continues to add higher-end brands and to increase its reach into men, plus sizes and kids. Its algorithms to personalize each box of clothes it ships keeps improving. Therefore, the company can spend less on acquiring new customers as it has increased its ability to get existing customers to spend more and come back more often. Stitch Fix can continue to grow its revenue from women in the U.S. with expansion opportunities in international markets over time. I believe the company can continue to grow by roughly 20% or more in 2020 and beyond.

Stitch Fix revenue growth (of over 21% in the latest reported quarter) comes from a combination of increasing the number of active clients by 17% to 3.4 million, coupled with driving higher revenue per active client. The company accomplished this while generating profits on a non-GAAP basis.

5. Amazon stock strategy will outpace the market (it closed last year at $1848/share).

Amazon shares increased by 23% last year while revenue in Q3 was up 24% year over year. This meant the stock performance mirrored revenue growth. Growth in the core commerce business has slowed but Amazon’s cloud and echo/Alexa businesses are strong enough to help the company maintain roughly 20% growth in 2020. The company continues to invest heavily in R&D with a push to create automated retail stores one of its latest initiatives. If that proves successful, Amazon can greatly expand its physical presence and potentially increase growth through the rollout of numerous brick and mortar locations. But at its current size, it will be difficult for the company to maintain over 20% revenue growth for many years (excluding acquisitions) so I am suggesting a more complex investment in this stock:

Buy X shares of the stock (or keep the ones you have)

Sell Amazon puts for the same number of shares with the puts expiring on January 15, 2021 and having a strike price of $1750. The most recent sale of these puts was for over $126

So, net out of pocket cost would be reduced to $1722

A 20% increase in the stock price (roughly Amazon’s growth rate) would mean 29% growth in value since the puts would expire worthless

If the stock declined 226 points the option sale would be a break-even. Any decline beyond that and you would lose additional dollars.

If the options still have a premium on December 31, I will measure their value on January 15, 2021 for the purposes of performance.

6. I’m adding Zoom Video Communications to the list but with an even more complex investment strategy (the stock is currently at $72.20)

I discussed Zoom Video Communications (ZM) in my post on June 24, 2019. In that post I described the reasons I liked Zoom for the long term:

Revenue retention of a cohort was about 140%

It acquires customers very efficiently with a payback period of 7 months as the host of a Zoom call invites various people to participate in the call and those who are not already Zoom users can be readily targeted by the company at little cost

Gross Margins are over 80% and could increase

The product has been rated best in class numerous times

Its compression technology (the key ingredient in making video high quality) appears to have a multi-year lead over the competition

Adding to those reasons it’s important to note that ZM is improving earnings and was slightly profitable in its most recent reported quarter

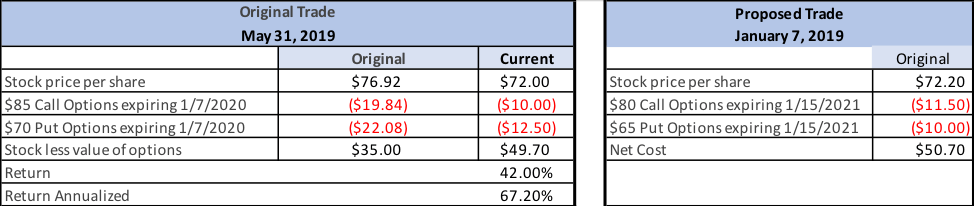

The fly in the ointment was that my valuation technology showed that it was overvalued. However, I came up with a way of “future pricing” the stock. Since I expected revenue to grow by about 150% over the next 7 quarters (at the time it was growing over 100% year over year) “future pricing” would make it an attractive stock. This was possible due to the extremely high premiums for options in the stock. So far that call is working out. Despite the company growing revenue in the 3 quarters subsequent to my post by over 57%, my concern about valuation has proven correct and the stock has declined from $76.92 to $72.20. If I closed out the position today by selling the stock and buying back the options (see Table 1) my return for less than 7.5 months would be a 42% profit. This has occurred despite the stock declining slightly due to shrinkage in the premiums.

Table 1: Previous Zoom trade and proposed trade

I typically prefer using longer term options for doing this type of trade as revenue growth of this magnitude should eventually cause the stock to rise, plus the premiums on options that are further out are much higher, reducing the risk profile, but I will construct this trade so that the options expire on January 15, 2021 to be able to evaluate it in one year. In measuring my performance we’ll use the closing stock price on the option expiration date, January 15, 2021 since premiums in options persist until their expiration date so the extra 2 weeks leads to better optimization of the trade.

So, here is the proposed trade (see table 1):

Buy X shares of the stock at $72.20 (today’s price)

Sell Calls for X shares expiring January 15, 2021 at a strike of $80/share for $11.50 (same as last price it traded)

Sell puts for X shares expiring January 15, 2021 with strike of $65/share for $10.00 (same as last price it traded)

I expect revenue growth of 60% or more 4 quarters out. I also expect the stock to rise some portion of that, as it is now closer to its value than when I did the earlier transaction on May 31, 2019. Check my prior post for further analysis on Zoom, but here are 3 cases that matter at December 31, 2020:

Stock closes over $80/share (up 11% or more) at end of the year: the profit would be 58% of the net cost of the transaction

This would happen because the stock would be called, and you would get $80/share

The put would expire worthless

Since you paid a net cost of $50.70, net profit would be $29.30

Stock closes flat at $72.20: your profit would be $21.50 (42%)

The put and the call would each expire worthless, so you would earn the original premiums you received when you sold them

The stock would be worth the same as what you paid

Stock closes at $57.85 on December 31: you would be at break even. If it closed lower, then losses would accumulate twice as quickly:

The put holder would require you to buy the stock at the put exercise price of $65, $7.15 more than it would be worth

The call would expire worthless

The original stock would have declined from $72.20 to $57.85, a loss of $14.35

The loss on the stock and put together would equal $21.50, the original premiums you received for those options

Outside of my stock picks, I always like to make a few non-stock predictions for the year ahead.

7. The major election year will cause a substantial increase in advertising dollars spent

According to Advertising Analytics political spending has grown an average of 27% per year since 2012. Both the rise of Super PACs and the launch of online donation tools such as ActBlue have substantially contributed to this growth. While much of the spend is targeted at TV, online platforms have seen an increasing share of the dollars, especially Facebook and Google. The spend is primarily in even years, as those are the ones with senate, house and gubernatorial races (except for minor exceptions). Of course, every 4th year this is boosted by the added spend from presidential candidates. The Wall Street Journal projects the 2020 amount will be about $9.9 billion…up nearly 60% from the 2016 election year. It should be noted that the forecast was prior to Bloomberg entering the race and if he remains a viable candidate an additional $2 billion or more could be added to this total.

The portion targeted at the digital world is projected to be about $2.8 billion or about 2.2% of total digital ad spending. Much of these dollars will likely go to Facebook and Google. This spend has a dual impact: first it adds to the revenue of each platform in a direct way, but secondly it can also cause the cost of advertising on those platforms to rise for others as well.

8.Automation of Retail will continue to gain momentum

This will happen in multiple ways, including:

More Brick & Mortar locations will offer some or all the SKUs in the store for online purchase through Kiosks (assisted by clerks/sales personnel). By doing this, merchants will be able to offer a larger variety of items, styles, sizes and colors than can be carried in any one outlet. In addition, the consolidation of inventory achieved in this manner will add efficiency to the business model. In the case of clothing, such stores will carry samples of items so the customer can try them on, partly to optimize fit but also to determine whether he or she likes the way it looks and feels on them. If one observes the massive use of Kiosks at airports it becomes obvious that they reduce the number of employees needed and can speed up checking in. One conclusion is this will be the wave of the future for multiple consumer-based industries.

Many more locations will begin incorporating technology to eliminate the number of employees needed in their stores. Amazon will likely be a leader in this, but others will also provide ways to reduce the cost of ordering, picking goods, checking out and receiving information while at the store.

9. The Warriors will come back strong in the 2020/21 season

Let me begin by saying that this prediction is not being made because I have been so humbled by my miss in the July post where I predicted that the Warriors could edge into the 2020 playoffs and then contend for a title if Klay returned in late February/early March. Rather, it is based on analysis of their opportunity for next season and also an attempt to add a little fun to my Top Ten List! The benefit of this season:

Klay and Curry are getting substantial time off after 5 seasons of heavy stress. They should be refreshed at the start of next season

Russell, assuming he doesn’t keep missing games with injuries, is learning the Warriors style of play

Because of the injuries to Klay, Curry, Looney, and to a lesser extent Green and Russell, several of the younger members of the team are getting experience at a much more rapid rate than would normally be possible and the Warriors are able to have more time to evaluate them as potential long-term assets

If the Warriors continue to lose at their current rate, they will be able to get a high draft choice for the first time since 2012 when they drafted Harrison Barnes with the 7th pick. Since then their highest pick has been between the 28th and 30th player chosen (30 is the lowest pick in the first round)

The Warriors will have more cap space available to sign a quality veteran

Andre Iguodala might re-sign with the team, and while this is not necessary for my prediction it would be great for him and for the team

The veterans should be hungry again after several years of almost being bored during the regular season

I am assuming the Warriors will be relatively healthy next season for this to occur.

10. At least one of the major Unicorns will be acquired by a larger player

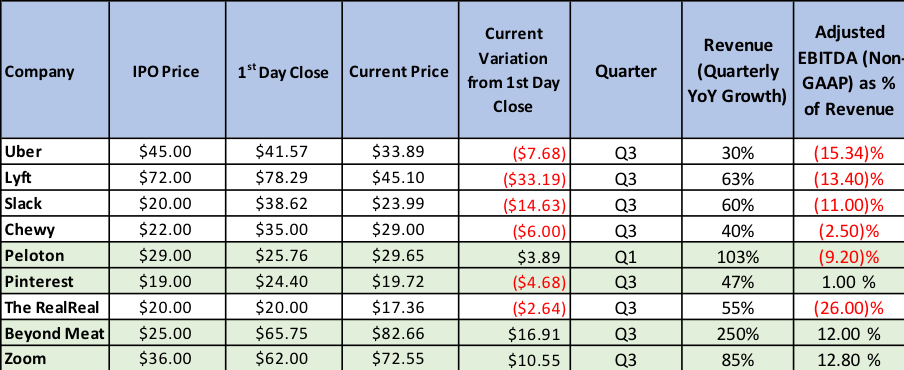

In 2019, there was a change to the investing environment where most companies that did not show a hint of potential profitability had difficulty maintaining their market price. This was particularly true of highly touted Unicorns, which mostly struggled to increase their share price dramatically from the price each closed on the day of their IPO. Table 2 shows the 9 Unicorns whose IPOs we highlighted in our last post. Other than Beyond Meat, Zoom and Pinterest, they all appear some distance from turning a proforma profit. Five of the other six are below their price on the first day’s close. A 6th, Peloton, is slightly above the IPO price (and further above the first days close). Beyond Meat grew revenue 250% in its latest quarter and moved to profitability as well. Its stock jumped on the first day and is even higher today. While Pinterest is showing an ability to be profitable it is still between the price of the IPO and its close on the first day of trading. Zoom, which is one of our recommended buys, was profitable (on a Non-GAAP basis) and grew revenue 85% in its most recent quarter. A 10th player, WeWork, had such substantial losses that it was unable to have a successful IPO.

Something that each of these companies have in common is that they are all growing revenue at 30% or more, are attacking large markets, and are either in the leadership position in that market or are one of two in such a position. Because of this I believe one or more of these (and comparable Unicorns) could be an interesting acquisition for a much larger company who is willing to help make them profitable. For such an acquirer their growth and leadership position could be quite attractive.

My long term readers know that every so

often the blog wanders into the sports arena. In doing so, I apply the same

type of analysis that I do for public stocks and for VC investments to sports,

and usually, basketball. Given all the turmoil that has occurred in the NBA

this off-season, including the Warriors losing Durant, Iguodala, Livingston,

Cousins and several other players, I thought it would be interesting to

evaluate the newly changed team. Both ESPN and CBS power rankings have them 7th

in the West and 11th in the NBA. I find that an overreaction as the

Warriors may have beaten the Raptors if Klay Thompson not been injured, they

swept Portland, and won the last 2 Rockets games without Durant. At the time

this drove a lot of chatter that the team might be better off without Durant (I

disagree).

But rather then compare the revised roster to

last year’s, it seems more closely matched with the 2014-15 team, as that was a

championship team that did not include Kevin Durant. I will make 2 key

assumptions:

Klay Thompson will return by

the end of February and be as effective as he was before his injury

The Warriors will make the

playoffs despite missing Thompson for the majority of the season

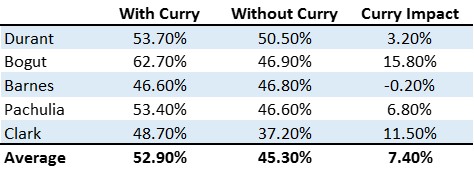

It all starts with Curry

A third key assumption that has been proven over and over again is that players that come to the Warriors usually perform better as they benefit from the “Curry Effect”, namely, getting more shots without having someone closely guarding them, (The Curry Effect), resulting in an average improved shooting percentage of over 5%. In all fairness, it really is the “Curry plus Thompson Effect” as the extreme focus on preventing the two of them from taking 3 point shots is what frees up others. It helps that Curry is unselfish and readily passes the ball when he is double or triple teamed. Thompson’s passing has improved substantially but since he gets his shot off so quickly, he has less need to pass it. Last year both shot over 40% from 3 despite defensive efforts focused on preventing each of them from taking those shots.

Starting Teams: 2019-20 vs 2014-15

Table 1

Curry, Thompson and Green, the heart and soul of the Warriors, all remain from the 2014-15 roster, and now are at their peaks. In the 2014-15 season when Green first became a starter, Curry was one year away from reaching his peak and Thompson was just coming into his own especially on defense. I believe each of them is better today then they were at that time. At his best, Bogut may have been better than Cauley-Stein, but by 2014 Bogut had been through a number of injuries. Last year Cauley-Stein averaged nearly double the points of 2014 Bogut (11.9 vs 6.3), took slightly more rebounds per game and was a better free throw shooter. Stein, much like Bogut, is also considered a solid pick setter and defender. Russell is someone who should benefit greatly from playing with Curry. Even without that, last season he averaged over twice as many points per game as 2014 Barnes (21.1 vs 10.1) which should take considerable pressure off Curry (and Klay when he returns). However, Barnes was a better defender in 2014 than Russell is today. I give the edge to all 5 starters on the 2019 starting team compared to the 5 that started in 2014-15.

Thompson may be the most underrated player in the league!

It’s unfortunate that Thompson was injured in game 6 of the 2019 finals as he was once again proving just how good he can be. Not only was he playing lockdown defense, but he also drove the offense in what has been referred to as a typical Klay game 6. In just 32 minutes, before getting injured, he scored 30 points on 83% effective shooting percentage (67% on 3s), went 10 for 10 on free throws, and had 5 rebounds and 2 steals. I believe Golden State, even without Durant, would have forced a game 7 if Thompson did not get injured.

It boggles my mind that one of the websites

could refer to Thompson as “an average player” who did not merit a max contract.

This is bordering on the ridiculous and has a lot to do with the fact that the

most important measure of shooting, effective shooting percentage (where each 3

made counts as 1½ 2 point shots made) does not normally get reported (or even

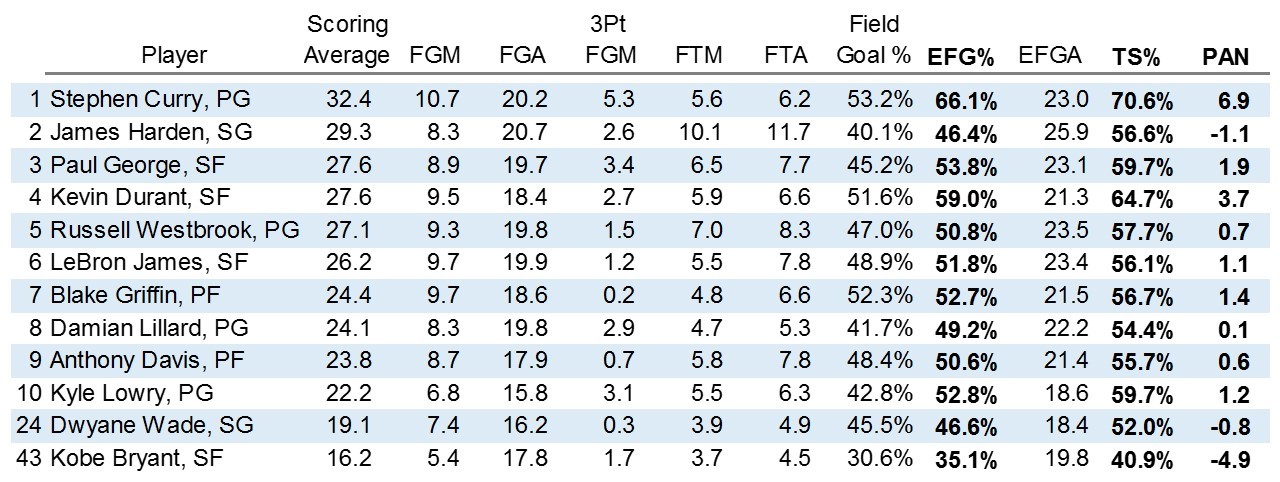

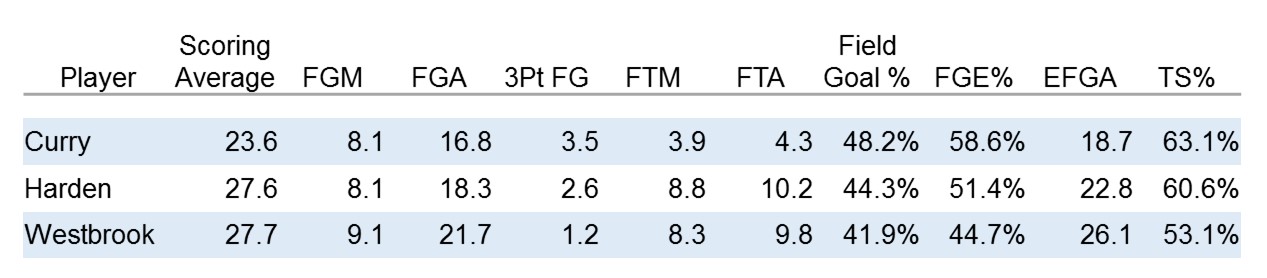

noticed). In Table 2, I list the top 31 scorers from last season (everyone who

averaged at least 20 points per game) and rank them by effective shooting.

Thompson is number 8 in effective shooting and number 3 in 3-point percentage

among this group. So, if effective shooting percentage was regularly published,

Thompson would show up consistently helping the perception of his value. When

this is coupled with his being a third team all-defensive player (i.e., one of

the top 15 defenders in the league) it appears clear that he should be

considered one of the top 15 players in the league.

Table

2: Top Scorers 2018-2019 Season

6th Man 2019-20 vs 2014-15

Kevon Looney has emerged as a potential

star in the works. While he may not yet be the defensive presence of Iguodala,

he is getting close. His scoring per minute played was higher than Andre’s

2014-15 numbers and his rebounds per minute were more than twice as much. While

Iguodala had greater presence and could run the team as well as assist others

in scoring, Looney at least partly makes up for this in his ability to set

screens. Looney also has a much higher effective shooting percentage (62.7% vs

54.0%) than Andre had in 2014-15. While Kevon doesn’t shoot 3s he gets many

points by putting back offensive rebounds and dunking lob passes. Overall, I

give the edge to Iguodala based on the Looney of last season but given Looney’s

potential to improve this might be dead even in the coming one.

Rest of the Bench for the 2 teams

It is the bench that is hardest to

evaluate. Unlike last year’s bench, the 2014-15 bench was quite strong which

spawned the Warrior logo “Strength in Numbers”. It included quality veteran

players like Leandro Barbosa, David Lee, Mareese Sprouts and Shaun Livingston, who

was playing at a much higher level than last season. The four of these together

averaged over 26 points per game. This

coming year’s bench is much younger and more athletic. It includes Alec Burks,

Glenn Robinson, Alfonzo McKinnie and Omari Spellman, plus several rookies and

Jacob Evans III. The first four are all capable of scoring and are solid 3-point

shooters (they could increase to well above average once with the Warriors). I

expect that group, coupled with one or two of the others, to exceed the 2014-15

bench in defense…but may not have as much scoring fire power. The team is

likely to give one or two of the rookies as well as Evans opportunities to earn

minutes as well. The bench is an improvement over last year but may not be as

strong as the 2014-15 squads.

Overall Assessment

I believe the 2019-2020 squad is better

than the championship team of 2015. The starting lineup features the core 3

players who have improved since then, D’Angelo Russell who was an all-star last

year, and a solid center in Willie Cauley-Stein making the edge substantial.

Looney as 6th man is already giving evidence of future stardom.

While he was not quite the Andre Iguodala of 2014-15, the difference is modest,

and Looney continues to improve. The 2014-15 bench appears superior to that of

next season, but the edge is not great as the newer group should be stronger

defensively and is not far off the older group as scorers – the question will

be how well they gel and how much the Curry/Klay factor improves their scoring.

Finally, I think Kerr is a better coach today than he was given the last 5

years of experience.

They May Have Improved vs 2014-15, but so has the Competition

ESPN and CBS power rankings reflect the

fact that multiple teams have created new “super star” two-somes:

Lakers: Lebron and Anthony

Davis

Clippers: Kawhi Leonard and

Paul George

Houston: Harden and Westbrook

(in place of Chris Paul)

Nets: Kyrie Irving and Durant

Contenders also include improving young teams

like Boston, Philadelphia, Denver, and Utah plus an improved Portland squad. This

makes the landscape much tougher than when the Warriors won their 2015

championship. Yet, none of these teams seem better than the Cleveland team (led

by a younger LeBron, Kyrie Irving and Kevin Love) the Warriors beat in 2015.

So, assuming Klay returns by late February and is back to par, I believe the

Warriors will remain strong contenders given the starting team with four all-stars

augmented by Willie Cauley-Stein and an improving Kevon Looney as 6th

man. However, it will be much tougher going in the early rounds in the playoffs,

making getting to the finals longer odds than in each of the past 5 years.

SoundBytes

An examination of Table 2

reveals several interesting facts:

Curry, once again is the leader

among top scorers in effective shooting and the only one over 60%

Antetokounmpo is only slightly

behind despite being a very poor 3-point shooter. If he can improve his

distance shooting, he may become unstoppable

Russell Westbrook, once again,

had the worst effective shooting percent of anyone who averaged 20 points or

more. In fact, he was significantly below the league average. Part of the

reason is despite being a very poor 3-point shooter he continues to take too

many distance shots. Whereas most players find that taking 3s increases their

effective shooting percent, for Westbrook it lowers it. I haven’t been able to

check this, but one broadcaster stated that he has the lowest 3-point

percentage of any player in history that has taken over 2500 3-point shots!

I believe that Westbrook has a

diminished chance to accumulate as many triple doubles next season as he has in

the past. There is only one ball and both he and Harden tend to hold it most of

the time. When Chris Paul came to the Rockets his assists per game decreased by

about 15% compared to his prior 3 season average.

This post is the third in my series on Key Performance Indicators (KPIs), with a heavy emphasis on contribution margin (CM). Previously, I analyzed why CM is such a strong predictor of success. Given that, companies should consistently look at ways of improving it while still maintaining sufficient growth in their business.

In Azure’s recent full day marketing seminar for our consumer (B2C) focused companies, my session highlighted 6 methods of improving CM:

Increase follow-on sales from existing customers

Raise the average invoice value of the initial and subsequent sales to a customer

Increase GM (Gross Margin) through price increases

Increase GM by reducing cost of goods sold (COGs)

Reduce Blended CAC (cost of customer acquisition) by increasing free or very low cost traffic

Decrease marketing spend as a % of revenue

Before drilling down on each of these I want to define several key terms that will be used throughout the discussion:

Contribution Margin = GM – Marketing/Sales Costs – other cost that vary with sales

Paid CAC = Market Spend/New Customers acquired through this spend

Blended CAC = Market Spend/All new customers

CAC Recovery Time (CAC RT) = the number of months until variable profit on a customer equals CAC

LTV/CAC = Life Time Value (LTV) of a customer/CAC

I will now review each of these strategies and provide some thoughts on how to activate these in consumer-facing businesses:

1. Increase Follow-On sales from existing customers

Since existing customers have little or no cost associated with getting them to buy, this will decrease blended CAC, increasing CM.

Increasing customer retention through improvements in customer care, more interesting and more targeted emails to a customer, or launching a subscription of one kind or another can all help.

On the first point here is an email I received shortly after subscribing to Harry’s, that I thought did an excellent job at engaging me with their customer support, increasing my likelihood to keep my subscription active:

Hi there,

My name is Katie, and I’m a member of the Harry’s team. I wanted to reach out and say thanks for supporting Harry’s.

You are important to us, and I am here to personally help you however I can to make your Harry’s experience as smooth as possible – both literally and figuratively. Please don’t hesitate to reach out with any thoughts or questions about your Harry’s products or Shave Plan, or just life in general. (And just a reminder that your next box is scheduled to ship on October 27th.) Thanks again for your support, and I hope to speak soon!

All the best, Katie

On the subscription concept, think about Amazon Prime. How many of you buy more frequently from Amazon because of being a prime member?

Add to product portfolio. By giving your customers more options of what to buy (all within the concept of your brand) customers are given the opportunity to spend more often.

Make sure your emails are interesting. This will increase the open rate and drive more follow on sales. If all your emails are about discounting your product, then customers will have less interest in opening them and your brand will be devalued. I’ve received emails from numerous sites that say an X% discount is available until a certain date, and then when that date passes, I receive a new offer that is the same or sometimes better. The most frequently opened emails have headers and content that creates interest beyond whatever products you sell. A/B test different headers and different content. It doesn’t matter how small or large you are or how many emails you send, it always pays to try different variations to increase open rates and conversion. Experiment with different messaging to different customer segments like those who purchased recently, those who “liked” an item, those that have never purchased, etc.

Build a Community of your customers. The more you can get customers engaged with you and with each other, the more committed to you they become and the longer they are retained. Think through how you can build an active community among your users through shared photos, videos, chatting, podcasts or events. Most of this should not involve trying to push new purchases but engaging your community to interact with you and each other.

2. Raise the average invoice value of the initial and subsequent sales to a customer

Since shipping costs will not increase proportionately, this will raise GM dollars and therefore CM.

Increase pricing. Most startups underprice their product thinking that will increase market adoption. Even some of the largest companies in the world have found there was ample room to increase prices. Thinking differently, Apple upped prices to over $1,000 for an iPhone. And then increased it again to $1,349 for the top of the line product. Five years ago, how many of you thought people would pay over $1,000 for a cell phone? This shows that unless you A/B test different price points you have no idea whether a price increase is the right strategy.

Upsell logical add-on products. While trying to get a customer to add to their shopping cart may seem obvious, many companies do not do this on a consistent basis. Some examples of ones that have: a flower company added vases to the offer, a mattress company added pillows and sheets; a subscription razor company added shaving gel; a cell phone company added a case. All of these led to reasonable attach rates of the add-on product and higher average invoice value. Testing what you could add to generate upsell should be a constant process.

“Selling” value added services is another form of upsell. This could include things like concierge customer service, service contacts, premier membership with benefits like: invites to special events, early access to new products, reduced shipping cost, preferred discounts on products, etc. If you get your customers to engage in one or more services, you will significantly increase their connection to your product and likely increase retention.

3. Increase Gross Margin through price Increases

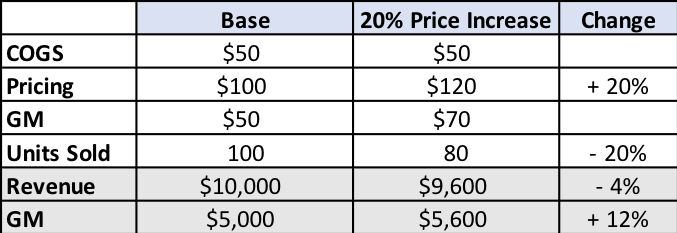

Surprisingly, sometimes higher prices position a product as premium (having more value) and generate increased unit sales. Often higher prices generate more revenue even when fewer unit sales result. What may be counter intuitive is that GM$ can increase even if revenue declines. For example, suppose a company has COGs of $50 for a product and is currently pricing it at $100. If a price increase of 20% causes 20% lower unit sales, revenue would decline by 4% while GM$ would increase 12%. Higher gross margin dollars provide more ability to spend on marketing.

4. Improving GM by reducing COGs

Better Pricing: When your volume increases, ask for better pricing from suppliers. Just as its important to price test regularly, its also important to talk to multiple potential suppliers of your parts/product. An existing supplier may not be eager to voluntarily offer a price discount that goes with increased volume but is more likely to do so if it knows you are checking with others.

Changing Packaging: Packaging should be re-examined regularly as improvements may help customer retention. But it also may be possible to lower the cost of the packaging or to change it in a way that lowers shipping costs since that may be based on the size of the box rather than weight.

Shipping Costs: Lower shipping cost per $ of revenue (increasing GM and CM) by generating larger orders. In addition to upsell, this can be done by offering better discounts if the order size is larger. One site I have purchased from offers 10% discount if your net spend (after discount) is over $100, 15% if over $150 and 20% if over $200. Getting to the highest discount lowers the price of the product by enough to motivate buyers (including me) to try to buy over $200 in merchandise. The extra revenue creates incremental product margin dollars and decreases shipping cost as a percentage of revenue. This in turn increases GM$.

For a subscription company this can be done by scheduling less frequent (larger) deliveries. The shipping cost of the larger order will be a much smaller percent of revenue, raising GM.

Opening a Second distribution center to reduce shipping cost. Orders shipped from a west coast distribution center to an east coast customer will have 5 zone pricing. By having a second distribution center in a place like Columbus, Ohio (a frequently used location) those same orders will usually be 1 zone, sometimes 2 zone pricing, resulting in substantial savings per order. The caveat here is that a company needs enough volume for the total savings on orders to exceed the fixed cost of a second distribution center.

5. Improving CM by driving “free” or “nearly free” traffic

The higher the proportion of free or inexpensive traffic to total traffic, the lower the blended CAC.

Improving SEO (search engine optimization). I’ve learned from SEO experts that optimizing SEO is not free, but rather very low cost compared to paid traffic. Our previous post walks through some of the science involved in making improvements. I would suggest using an SEO consultant as it is likely to lead to far better results.

Convert a visitor not ready to buy to an email recipient. If you do that than you will have subsequent opportunities to market to her or him. A slightly costlier version of this is to use remarketing to woo visitors who came to your site but didn’t buy. While using remarketing (advertising) has a cost, it is usually much lower CAC than other methods.

Produce emails that get forwarded and go viral. Such emails need to motivate recipients to forward them due to being very funny, of human interest, etc. While there is typically a product offering embedded in them, the header emphasizes the reason to read it. One Azure portfolio company, Shinesty, recently had an email that was opened by about 7X the number of people it was initially sent to. That generated a lot of potential customers without spending extra marketing dollars. Engaging emails has enabled Shinesty to maintain high CM and high growth.

Use social networking to generate incremental customers. Having the right posts on a social network like Instagram can lead to new potential customers finding out about you and lead to additional sales.

Optimize Customer Retention. Or as my good friend Chris Bruzzo (CMO of EA) spoke about at the Azure Marketing conference: “Love the ones you’re with.” Existing customers are usually the largest source of “free” buyers in a period. The longer you retain a customer, the more repeat buyers you have, increasing contribution margin. So, it’s imperative to take great care of your existing customers.

Drive PR. Like SEO, there is some cost involved in this but if you are judicious in any agency spend and thoughtful in creating news worthy press releases this can be a great source of traffic at a modest cost. However, I recommend you try to understand what you are getting from PR because I have seen situations where the spend did not produce meaningful results.

6. Decrease Marketing Spend as a % of Revenue.

The CAC Recovery Time plays a major role in how to manage your market spend to balance growth and burn. For example, if CAC Recovery Time is one month, spending more will not drive up burn appreciably. If it takes more than a year to recover your CAC, moderating market spend is critical to achieving a reasonable CM. If you recoup CAC faster, you can invest more quickly in the next round of customers. In the consumer space, I won’t invest in a company that has a long (a year or more) CAC Recovery Time as customers are likely to churn in an average of 2-3 years, making it difficult to achieve a reasonable business model. For B2B company’s customer longevity tends to be much longer, and the LTV/CAC can be 5X or more even if CAC Recovery Time is a year.

When a company decreases its market spend as a % of revenue it may experience lower growth but better CM. However, many companies have waste in their marketing spend so it’s important to measure the efficacy of each area of spend separately and to eliminate programs with a low return. This will allow you to reduce the spend with minimal impact on growth rates. There is a balance needed to try to optimize the relationship between CM and revenue growth as higher burn requires raising money more frequently and can put your company at risk. On the other hand, a company generating $1M in revenue needs to be growing at 100% or more to warrant most VCs to consider investing. Since CM should improve with scale, spending more on marketing may be a viable strategy for early stage companies. Once a company reaches $10M in revenue, annual growth of 50% will get it to $76M in revenue in 5 years so such a company should consider better CM rather than driving much higher growth rates and continuing to burn excessive cash.

In summary, Contribution Margin is the lifeblood of a company. If it is weak, the company is likely to fail over time. If it is strong and revenue growth is high, success seems likely. Improving CM is an ongoing process. I realize many of you probably feel much of what I’ve said is obvious, but my question is:“How many of these suggestions are you already doing on a regular basis?”

While you may be using several of the suggestions in this post, I encourage you to try more and to also double down where you can on the ones you already are trying. The results will make your company more valuable!

SoundBytes

I just want to remind readers that my collaborator on my blog posts, Andrea Drager, doesn’t typically take a bow for her significant contributions. Also, in this post, Chris Bruzzo added several improvements that have been incorporated. So many thanks to Andrea and Chris.

Can’t help but comment on the start to the NBA season. Not surprisingly, the Warriors are off to a great start with Curry and Durant leading the way. Greene and Thompson now have moved close to their usual contribution so I’m hopeful that the team can keep up its current pace.

What surprised me early on was the lack of recognition that both Toronto and San Antonio would be greatly improved. Remember, while San Antonio lost Kawhi, he only played a few games last year so with the addition of DeRozan should improve and once again reach the playoffs. For Toronto the change to Kawhi is a marked improvement placing them very competitive with the Celtics for eastern leadership.