Mike Kwatinetz is a Founding General Partner at Azure Capital Partners and a Venture Capitalist investing in application software (SaaS), ecommerce, consumer web and infrastructure technology companies. Successful exits include: Bill Me Later, VMware, TripIt and Top Tier.

I promised a new post within 3 weeks of the last one. It’s here…but is different than originally planned! Several recent M&A events have motivated me to try to explain some basics on what happens to associated stocks in such a situation, the most recent being the Zoom acquisition of Five9. If the acquisition is a stock for stock transaction (as the Zoom one is), the acquirors stock will usually decline in price right after the announcement of the deal. The reason for the inevitable next day decline of the acquirer’s stock can be misunderstood. In this post I will explain why the decline has little to do with investors reaction to the quality of the acquisition.

What happens when a stock for stock acquisition of a public company is announced?

When a public company offers to acquire another, it is quite usual for the offer to be at a premium to the current stock price of the target company. Without a premium there is little motivation for the target company to accept the offer, and it can create a legal issue – as class action attorneys are vigilant to find opportunities to sue and can claim that the target sold out too “cheaply”.

Assuming the number of shares involved is a material amount, then once the deal is made public, the stock of the acquirer will almost always decline the next day while the target’s price rises. The press often interprets this as “The Street” being negative on the acquisition, when in fact it has little to do with a critique of the deal. Instead, it stems from “Risk Arbitrage” where arbitragers will short the acquirer’s stock and buy the target’s stock to create a certain profit if the acquisition is consummated. To illustrate this, I will use an easy-to-understand example:

Suppose Company A is trading at $100/share and then offers to acquire Company B (trading at $60/share). Suppose the offer is one share of Company A stock for each share of Company B stock. At these prices an arbitrager can:

Buy Company B stock at $60/share – this equates to buying Company A stock at a discount if and when the deal closes since each share of B will then convert to one share of A

Short Company A stock and receive $100/share

The net result is a gain of $40/share assuming the deal consummates. This occurs because when the share of B is converted to a share of A it can be used to cover the short position without the arbitrager spending any money. The Arbitrager will continue to do this as long as there is a gap between the prices of the shares. Given the number of shares being sold, A’s stock price will usually fall (the next day) and B’s will rise until it is virtually equal to A’s price on an as converted basis. The difference once this reaches equilibrium is the “risk premium”.

The reason it’s called “Risk Arbitrage” is that if the deal falls apart money could be lost. Therefore, a smart arbitrager will assign a risk premium based on his or her assessment of the probability that the deal will break. Once the 2 stocks are in sync, they will continue to trade in sync with the difference in prices being the risk premium. This will probably mean that the acquirer’s stock will return to around its prior price a few days later plus or minus its normal fluctuation, and the premium or discount assigned by investors to the deal.

Using Zoom Acquisition of Five9 as a Real Example

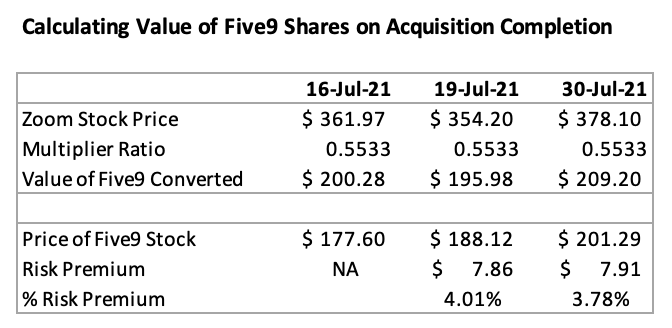

For an actual example, lets review the Zoom acquisition of Five9 announced on Sunday July 18, 2021. The agreement was to exchange each share of Five9 for 0.5533 shares of Zoom. At the close of the market on Friday, July 16 (just before the announcement):

Zoom shares were at $361.97 and Five9 shares were at $177.60

The theoretic value of a Five9 share based on 0.5533 of a Zoom share was $200.28 a 13% premium to the July 16 Five9 share price.

By the close on Monday July 19, Zoom shares had declined to $354.20 and Five9 shares had increased in price to $188.12. I saw many articles interpreting the Zoom drop in price as investors being negative on the deal. However, I believe it was the result of the volume of Zoom stock shorted by arbitragers.

Since 0.5533 times the Zoom price of $354.20 is $195.98 there was still a discrepancy in the ratio between the two stocks versus the ultimate conversion multiple of 0.5533 since Five9 was trading at 4.01% lower than the exchange ratio implied it was worth. This meant that Arbitragers were initially assigning a 4.01% risk factor based on the odds the deal would close. Once the two stocks settled into the appropriate ratio they have traded in sync since (less the Risk Premium). The risk premium has declined slightly in the two weeks since the deal was announced as arbitragers began to assess a lower risk factor to the odds the deal would break.

This same pattern usually occurs each time a stock for stock transaction is announced. There is too much money to be made from the arbitrage if the two stocks don’t adjust based on the conversion ratio. Any time they get out of sync arbitragers will step in again. When they initiate a pair of transactions the combination of buying stock in the target and shorting stock in the acquirer generates an immediate profit in cash. In our example of Zoom if the stocks were still at the July 16 price a transaction could be:

Buy 10,000 shares of Five9 at $177.60 at a cost of $1,776,000

These shares would convert to 5,533 shares of Zoom when the acquisition closes

Sell short 5,533 shares of Zoom at $361.97/share to receive $2,002,780

Immediate cash to arbitrager = $2,002,780 – $1,776,000 = $226,780

If and when the acquisition closes the arbitrager would net a profit of $226,780

If the deal breaks there could be a loss as the Zoom share short would need to be covered and the Five9 shares sold. This is why there is a risk premium involved.

Of course, the July 16 prices disappeared quickly when the stocks opened on July 19 as the arbitragers begin to execute their transactions. But as long as the difference exceeded the risk premium, they continued to transact to realize an immediate cash return. Once equilibrium was reached arbitragers ceased transacting (unless the stocks were to get out of sync again).

Conclusion

If you own a stock making a major acquisition and its stock price drops the day after the transaction is announced, the drop is likely to be temporary. Of course, there are situations where investors actually are so negative towards the transaction that the acquirer stock does not recover, but the first day drop usually has little to do with that.

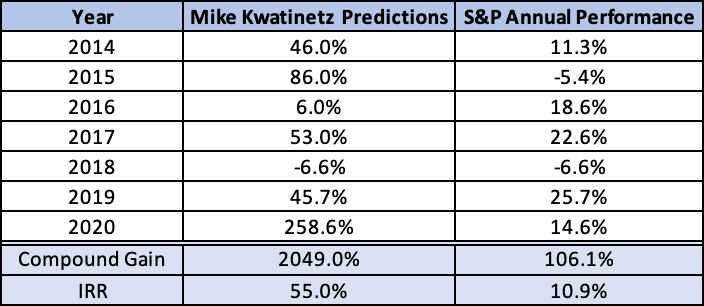

This may seem like a repeat of what you have heard from me in the past, but I enter each year with some trepidation as my favored stocks are high beta and usually had increased in value the prior year (in 2019 they were up about 46% or nearly double the S&P which also had a strong year). The fact is: I’m typically nervous that somehow my “luck” will run out. But, in 2020 I was actually pretty confident that my stock picks would perform well and would beat the market. I felt this confidence because the companies I liked were poised for another very strong growth year, had appreciated well under their growth over the prior 2-year period and were dominant players in each of their sub-sectors. Of course, no one could foresee the crazy year we would all face in 2020 as the worldwide pandemic radically changed society’s activities, purchasing behavior, and means of communication. As it turns out, of the 6 stocks I included in my top ten list 3 were beneficiaries of the pandemic, 2 were hurt by it and one was close to neutral. The pandemic beneficiaries experienced above normal revenue growth and each of the others faired reasonably well despite Covid’s impact. The market, after a major decline in March closed the year with double digit gains. Having said all that, I may never replicate my outperformance in 2020 as the 6 stocks had an average gain of an astounding 259% and every one of them outperformed the S&P gain of 14.6% quite handily.

Before reviewing each of my top ten from last year, I would like to once again reveal long term performance of the stock pick portion of the top ten list. I assume equal weighting for each stock in each year to come up with performance and then compound the yearly gains (or losses) to provide the 7-year performance. I’m comparing the S&P index at December 31 of each year to determine annual performance. Soundbyte’s compound gain for the 7-year period is 2049% which equates to an IRR of 55.0%. The S&P was up 106.1% during the same 7-year period, an IRR of 10.9%.

2020 Non-Stock Top Ten Predictions also Impacted by Covid

The pandemic not only affected stock performance, it had serious impact on my non-stock predictions. In the extreme, my prediction regarding the Warriors 2020-2021 season essentially became moot as the season was postponed to start in late December…so had barely over a week of games in the current year! My other 3 predictions were all affected as well. I’ll discuss each after reviewing the stock picks.

The 2020 Stocks Picked to Outperform the Market (S&P 500)

Tesla Stock which closed 2019 at $418/share and split 5 for 1 subsequently

Facebook which closed 2019 at $205/share

DocuSign which closed 2019 at $74/share

Stitch Fix which closed 2019 at $25.66/share

Amazon which closed 2019 at $1848/share

Zoom Video Communications which closed 2019 at $72.20/share

In last year’s recap I noted 3 of my picks had “amazing performance” as they were up between 51% and 72%. That is indeed amazing in any year. However, 2020 was not “any year”. The 6 picks made 2019 gains look like chopped liver as 4 of my 6 picks were up well over 100%, a 5th was up over 70% and the last had gains of double the S&P. In the discussion below, I’ve listed in bold each of my ten predictions and give an evaluation of how I fared on each.

1. Tesla stock appreciation will continue to outperform the market (it closed last year at $418/share). Note that after the 5 for 1 split this adjusts to $84.50/share.

In 2020, Tesla provided one of the wildest rides I’ve ever seen. By all appearances, it was negatively impacted by the pandemic for three reasons: people reduced the amount they drove thereby lessening demand for buying a new vehicle, supply chains were disrupted, and Tesla’s Fremont plant was forced to be closed for seven weeks thereby limiting supply. Yet the company continued to establish itself as the dominant player in electronic, self-driving vehicles. It may have increased its lead in user software in its cars and it continued to maintain substantial advantages in battery technology. The environment was also quite favorable for a market share increase of eco-friendly vehicles.

Additionally, several other factors helped create demand for the stock. The 5 for 1 stock split, announced in August was clearly a factor in a 75% gain over a 3-week period. Inclusion in the S&P 500 helped cause an additional spike in the latter part of the year. Tesla expanded its product line into 2 new categories by launching the Model Y, a compact SUV, to rave reviews and demonstrating its planned pickup truck (due in late 2021) as well. While the truck demo had some snags, orders for it (with a small deposit) are currently over 650,000 units.

All in all, these factors led to Tesla closing the year at $706/share, post-split, an astounding gain of 744% making this the largest one year gain I’ve had in the 7 years of Soundbytes.

2. Facebook Stock will outpace the market (it closed 2019 at $205 per share)

Facebook was one of the companies that was hurt by the pandemic as major categories of advertising essentially disappeared for months. Among these were live events of any kind and associated ticketing company advertising, airlines and cruise lines, off-line retail, hotels, and much more. Combine this with the company’s continued issues with regulatory bodies, its stock faced an uphill battle in 2020. What enabled it to close the year at $273 per share, up 33% (over 2x the S&P), is that its valuation remains low by straight financial metrics.

3. DocuSign stock appreciation will continue to outperform the market (it closed 2019 at $74/share)

DocuSign was another beneficiary of the pandemic as it helped speed the use of eSignature technology. The acceleration boosted revenue growth to 53% YoY in Q3, 2021 (the quarter ended on October 31, 2020) from 39% in Fiscal 2020. Since growth typically declines for high-growth companies this was significant. Investors also seemed to agree with me that the company would not lose the gains when the pandemic ends. Further, DocuSign expanded its product range into contract life-cycle management and several other categories thereby growing its TAM (total available market). Despite increased usage, DocuSign COGs did not rise (Gross Margin was 79% in Q3). Finally, competition appeared to weaken as its biggest competitor, Adobe, lost considerable ground. This all led to a sizable stock gain of 200% to $222/share at year end.

4. Stitch Fix stock appreciation will continue to outperform the market (it closed 2019 at $25.66/share)

Stitch Fix had a roller coaster year mostly due to the pandemic driving people to work from home, which led to a decline in purchasing of clothes. I’m guessing many of you, like me, wear jeans and a fleece or sweatshirt most days so our need for new clothes is reduced. This caused Stitch Fix to have negative growth earlier in the year and for its stock to drop in price over 50% by early April. But, the other side of the equation is that brick and mortar stores lost meaningful share to eMerchants like Stitch Fix. So, in the October quarter, Stitch Fix returned to growth after 2 weak quarters caused by the pandemic. The growth of revenue at 10% YoY was below their pre-pandemic level but represented a dramatic turn in its fortunes. Additionally, the CEO guided to 20-25% growth going forward. The stock reacted very positively and closed the year at $58.72/share up 129% for the year.

5. Amazon stock strategy will outpace the market (it closed last year at $1848/share)

Amazon had a banner year in 2020 with a jump in growth driven by the pandemic. Net sales grew 37% YoY in Q3 as compared to an approximate 20% level, pre-pandemic. Their gains were in every category and every geography but certainly eCommerce led the way as consumers shifted more of their buying to the web. Of course, such a shift also meant increased growth for AWS as well. Net Income in Q3 was up 197% YoY to over $6.3 billion. Given the increase in its growth rate and strong earnings the stock performed quite well in 2020 and was up 76% to $3257/share.

In our post we also recommended selling puts with a strike price of $1750 as an augmented strategy to boost returns. Had someone done that the return would have increased to 89%. For the purposes of blog performance, I will continue to use the stock price increase for performance. Regardless, this pick was another winner.

6. I added Zoom Media to the list of recommended stocks. It closed 2019 at $72.20

When I put Zoom on my list of recommended stocks, I had no idea we’d be going through a pandemic that would turn it into a household name. Instead, I was confident that the migration from audio calls to video conference calls would continue to accelerate and Zoom has the best product and pricing in the category. For its fiscal 2020-year (ending in January, 2020) Zoom grew revenue 78% with the final sequential quarter of the year growth at 13.0%. Once the pandemic hit, Zoom sales accelerated greatly with the April quarter up 74% sequentially and 169% YoY. The April quarter only had 5 weeks of pandemic benefit. The July quarter had a full 3 months of benefit and increased an astounding 102% sequentially and 355% YoY. Q3, the October quarter continued the upward trend but now had a full quarter of the pandemic as a sequential compare. So, while the YoY growth was 367%, the sequential quarterly growth began to normalize. At over 17% it still exceeded what it was averaging for the quarters preceding the pandemic but was a disappointment to investors and the stock has been trading off since reporting Q3 numbers. Regardless of the pullback, the stock is ahead 369% in 2020, closing the year at $337/share .

In the post we also outlined a strategy that combined selling both put and call options with purchasing the stock. Later in the year we pointed out that buying back the calls and selling the stock made sense mid-year if one wanted to maximize IRR. If one had followed the strategy (including the buyback we suggested) the return would still have been well over a 100% IRR but clearly lower than the return without the options. As with Amazon, for blog performance, we are only focused on the straight stock strategy. And this recommendation turned out to be stellar.

Unusual Year for the Non-Stock Predictions

7. The major election year will cause a substantial increase in advertising dollars spent

This forecast proved quite valid. Michael Bloomberg alone spent over $1 billion during his primary run. The Center for Responsive Politics reported that they projected just under $11 billion in spending would take place between candidates for president, the Senate and the House in the general election. This was about 50% higher than in 2016. Additionally, there will be incremental dollars devoted to the runoff Senate races in Georgia. This increase helped advertising companies offset some of the lost revenue discussed above.

8. Automation of Retail will continue to gain momentum

Given the pandemic, most projects were suspended so this did not take place. And it may be a while before we have enough normalization for this trend to resume, but I am confident it will. However, the pandemic also caused an acceleration in eCommerce for brick and mortar supermarkets and restaurants. I’m guessing almost everyone reading this post has increased their use of one or more of: Instacart, Amazon Fresh, Walmart delivery, Safeway delivery, Uber Eats, GrubHub, Doordash, etc. My wife and I even started ordering specialty foods (like lox) from New York through either Goldbelly or Zabars. Restaurants that would not have dreamed of focusing on takeout through eCommerce are now immersed in it. While this was not the automation that I had contemplated it still represents a radical change.

9. The Warriors will come back strong in the 2020/2021 season

This was my fun prediction. Unfortunately, the combination of injuries and Covid eliminated fun for sports fans. I expected that there would be enough games in 2020 to evaluate whether my forecast was correct or not. Since the season started in late December its premature to evaluate it. Also, I pointed out that the team had to stay relatively healthy for the prediction to work. Guess what? The Warriors have already had 2 devastating injuries (Thompson the critical one, and Chriss, who I expected would help the second team as well).

Yet, several things I predicted in the post have occurred:

The younger players did develop last season, especially Pascal

The Warriors did get a very high draft choice and at first blush he seems like a winner

The Warriors did use the Iguodala cap space to sign a strong veteran, Oubre.

Given the absence of Thompson, the team will be successful if they make the playoffs. So, let’s suspend evaluating the forecast to see if that occurs in a packed Western Conference despite losing Thompson. Last year they started 4 and 16. For the 2020-2021 season (as of January 3) they are 3 and 3 and appear to be a much better team that needs time to jell. But the jury is out as to how good (or bad) they will be.

10. At least one of the major Unicorns will be acquired by a larger player

There were 9 Unicorns listed in the post. Eight are still going at it by themselves but the 9th, Slack, has recently been acquired by SalesForce making this an accurate prediction.

2021 Predictions coming soon

Stay tuned for my top ten predictions for 2021… but please note most of the 6 stocks from 2020 will continue on the list and as usual, for these stocks, we will use their 2020 closing prices as the start price for 2021. For any new stock we add, we will use the price of the stock as we are writing the post.

Soundbytes

I thought I would share something I saw elsewhere regarding New Year’s wishes. In the past most people wished for things like success for themselves and/or family members in one form or another. The pandemic has even transformed this. Today, I believe most people are more focused on wishing for health for them, their family, friends, and an end to this terrible pandemic. Please take care of yourselves, stay safe. We are getting closer to the end as vaccines are here and will get rolled out to all of us over the next 4-6 months.

This post will be more of a stream of consciousness rather than one of focus on a topic.

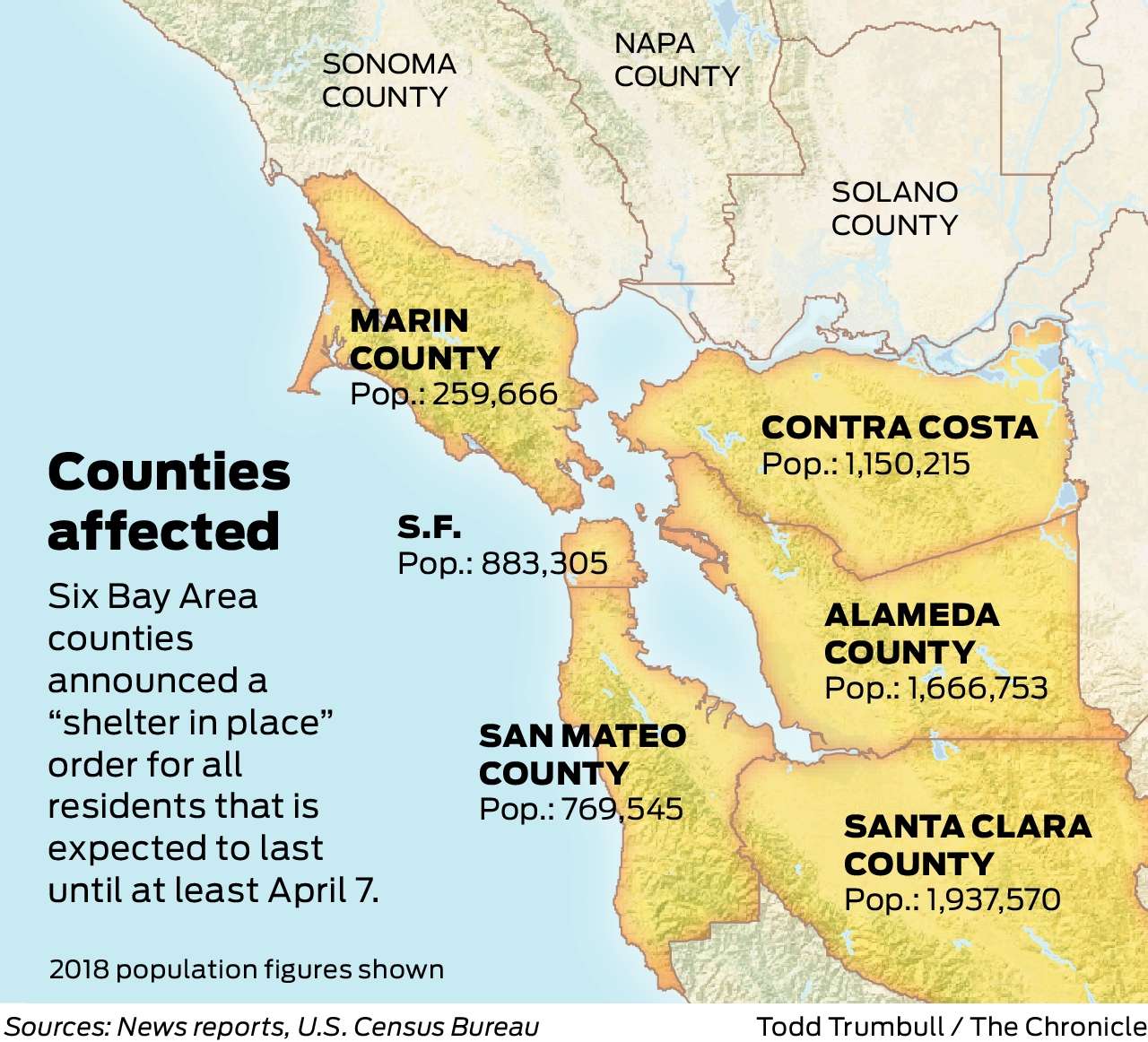

Sheltering in Place

My wife, Michelle, and I have obeyed the order to “shelter in place” by staying at home except for walks outside (avoiding going within 6 feet of anyone). The order started in San Mateo County at 12:01 AM on March 17. Our last time being in close proximity with anyone was Friday March 13, so we’re getting close to knowing we are virus free. We stocked up on food a day before the order began and have already had one “Instacart” delivery as well. Not sure what you are all doing but we have called a number of family members and friends to make sure they are ok – times like this make you want to verify the health of others! We also had to cancel vacation plans – which happened in steps as fear of the virus increased. We had scheduled a trip that included visiting Cabo followed by some time with good friends/cousins in Arizona.

I was scheduled to have my annual checkup before the trip, but 2 days before my doctor called to tell me not to come. It seems that the building he is located in is a center for virus testing and he thought it made no sense to have unneeded exposure. During the course of the conversation I mentioned we would be leaving for Cabo on Thursday, March 19 and he immediately warned me not to go. While I don’t want to be compared to the premier of Italy who initially told people to ignore the risk, at the time I felt the risk was overblown (as long as I was careful in Cabo). My doctor made an impossible to refute point saying: “What if you couldn’t get back because of a lockdown. Wouldn’t you rather be in the vicinity of Stanford Hospital if anything happened instead of in Mexico?” Hard to argue with that, so we decided to fly directly to Arizona instead. As flying became a risky option, we next thought we might drive to Arizona. Finally, we decided it was best to postpone the vacation. I’m guessing some of you went through a similar gradual awakening to the degree of risk.

Still Partying

Michelle and I truly enjoy the company of others. Staying at home precludes that, at least in the normal way…but then Zoom came to the rescue! We have had two “Zoom cocktail parties.” The first was more formal so everyone dressed up (I wore a wild Shinesty tuxedo and Michelle a matching outfit). Each couple at this virtual party had their drink of choice in front of them as well as appetizers. A few days later, Michelle and I hosted a similar party after becoming paying subscribers for Zoom. At our party we asked people to dress business casual. The benefit of requiring some higher level of dress than jeans is that it makes one feel (almost) like they are out partying. Each party lasted a little over one hour and the conversation was pretty lively. Of course, the first 10-15 minutes were all about the impact of the virus, but then the conversation rotated through a number of less depressing subjects.

We now have been invited to a virtual dinner party by the first group host and we are planning a winery hosted party for the second group. Not sure, but in all likelihood, we’ll also work on setting up a third group. If we are still in this situation when Passover arrives, we will have our traditional seder (for 20 people) via Zoom.

Our Crossword Puzzle Tradition Continues

My family has been jointly solving the NY Times crossword puzzles for many years. More recently our grandson has not only joined in but become pretty prolific. On a typical Sunday we meet our daughter, son-in-law and their two kids for brunch and do the famous NY Times Sunday puzzle. If our son is in town, he also joins us. The only difficulty is that we each have our own copy, either on an iPhone or physical printout, so coordinating is a bit more difficult. This past weekend that tradition was replaced by doing it together over brunch at each of our homes. Once again, a Zoom conference call was the method of joining together. An added benefit was that, using Zoom, the puzzle was up on each of our large screens for all of us to share one version, and we actually finished in one of our fastest times ever!

The Wild Stock Market

As you know, at the beginning of each year I select stocks to invest in. One point I continue to make is that my picks tend to be high beta stocks so they might depreciate disproportionately in a down market. With the S&P down about 25%, this is certainly bear territory, but this is not your ordinary down market as the virus impacts different companies in different ways. I have been most fortunate in that 3 of my 6 selections, Zoom, Amazon and Docusign, should benefit from the virus. Zoom is the most obvious and this has not been lost on investors, as the stock as of this writing (March 24) is up almost 90% year to date. Of course, given the substantial day to day fluctuations this might not be the case by the time this blog is posted. Docusign should also be a major beneficiary of an increase in the number of people who work at home as its electronic document signing technology increases in importance (I’ve already had a major increase in e-signing in this past week at home). Amazon is having trouble keeping up with demand since most people have decided to rely on home delivery for fulfilling their needs. A fourth stock, Tesla is also ahead 21% year to date, but its stock has been impacted by the virus as it was up over 100% before the virus impact was felt. The other 2 stocks in my picks, Facebook and Stitch Fix, are down quite a bit but I still expect them to recover by year end despite the fact that Facebook should have lower revenue than previously forecast (advertising budgets will be cut) and Stitch Fix likely will also miss prior forecasts since people not leaving their homes are less likely to be buying a lot of new clothes – but whatever they do buy will be online (partly offsetting a reduction of total spending on new clothes).

Is it a good time to be buying stocks and/or munis?

In my last post I reminded you that the best strategy for making money in the stock market is to “Buy Low Sell High”. While this seems silly to even say, people have difficulty buying low as that is when the most fear exists (or the market wouldn’t be low). While there is danger that the impact of the virus could trigger a weak economy for at least this year, I still believe this is now mostly factored into the market and have been buying after days of large market declines. Don’t do this indiscriminately, as some companies (think physical retailers for example) may be permanently impaired, but others may also benefit from what is taking place. Still others will recover and their stocks are now trading at attractive prices. What has surprised me is there has also been an opportunity to buy munis at good rates of return (3.8% to over 4% for A or better rated bonds with 8 or more years to call/maturity). But this was only available to me on Schwab (not on several large well-known brokerage houses I use). It seems the panic for liquidity has led to better than expected returns despite 10-year Treasuries dropping to 1.02% from 2.41% a year ago. However, it also seems that several of the larger brokerage firms are not passing these returns through to their customers. Once the current “panic” situation passes (say 3 months from now) tax-free bonds with 10 years or less to call should be yielding under 2% annualized return to call leading to substantial appreciation of munis acquired at a much higher rate.

We need a Sports Interlude

Since sports are at a standstill my usual analysis of performance seems out of context. Instead I wanted to suggest something I have been thinking about for the last few months – how to punish the Houston Astros for their cheating. Given the mounting disapproval of the Baseball Commissioners lack of action perhaps he will even adopt my suggestion (of course he may never even hear of it). It’s a simple one that is the mirror image of the advantage the Astros created by stealing signs (through use of technology) in their home playoff games for about 3 years. My answer is to take away at least one home game from them in every playoff series they are in (including the World Series) for the next 3 years. If it’s a one game series, they would always play at the other team’s park. If it’s a 5-game series, they would at most have one home game, and in a 7-game series at most 2 home games. While this would not totally make up for what they did, it would at least somewhat even the playing field (no pun intended).

Back to the Virus

Given all the sacrifices many are making by sheltering in place, it should be easy to expect an immediate decline in the number of new cases. Unfortunately, the incubation period for the virus is estimated to be up to 14 days. We also have under-tested so there are more people who have it than the statistics show. With increased testing more of the actual cases will be detected. When these two factoids are combined, even if there was zero spread of the virus once the stringent asks were put in place, we would still continue to see many new cases during the 14-day period and the number would be further increased by improved testing. Unfortunately, not everyone is behaving perfectly so while I would expect (hope) that in each geography we would see substantial reduction in the number of new cases after 2 weeks of sheltering in place, the number won’t get to zero. It should take a drop but getting to zero could take much longer especially considering that part of the process to fix things still exposes medical professionals, delivery people, and more to becoming carriers of the virus.

What should Companies do to Protect their Futures?

There are a number of steps every company needs to consider in reacting to the threat posed by the virus to both health and the economy. At Azure we have been advising our portfolio companies to consider all of them. They include:

First and foremost, make sure you protect your employee’s health by having them work remotely if at all possible.

Draw down bank lines completely to increase liquidity in the face of potential reduced revenue and earnings.

Create new forecast models based on at least 3 scenarios of reduced revenue for varying periods of time. If you were anticipating a fundraise assume it will take longer to close.

If modeling indicates additional risk, consider cutting whatever costs you possibly can including:

A potential reduction in workforce – while this is unpleasant you need to think about insuring survival which means the remaining employees will have jobs

Reduced compensation for founders and top executives possibly in exchange for additional options

Negotiating with your landlord (for reduced or delayed rent) as well as other vendors

Eliminating any unnecessary discretionary spending

Evaluating the near-term ROAS (return on advertising spend). On the one hand, preserving capital may mean the need to cut if the payback period is more than a few months. On the other hand, since advertising cost is likely to be lower given reduced demand (for example the travel industry likely will completely shut down advertising as will physical retail) it is possible you may find that increasing marketing adds to cash flow!

Think about how you might play offense – are there things you can offer new and/or existing customers to induce them to spend more time on your site or app (and perhaps increase buying) in this environment?

Stay Safe

While I was a sceptic regarding how pandemic this pandemic would be, I eventually realized that there was little downside in being more cautious. So please follow the guidelines in your area. It is easy to order just about anything online so going out to shop is an unnecessary risk. As they said in the Hunger Games: “May the odds be ever in your favor!” But, unlike the Hunger Games you can improve the odds.

I wanted to start this post by repeating something I discussed in my top ten lists in 2017 and 2018 which I learned while at Sanford Bernstein in my Wall Street days: “Owning companies that have strong competitive advantages and a great business model in a potentially mega-sized market can create the largest performance gains over time (assuming one is correct).” It does make my stock predictions somewhat boring (as they were on Wall Street where my top picks, Dell and Microsoft each appreciated over 100X over the ten years I was recommending them).

Let’s do a little simple math. Suppose one can generate an IRR of 26% per year (my target is to be over 25%) over a long period of time. The wonder of compounding is that at 26% per year your assets will double every 3 years. In 6 years, this would mean 4X your original investment dollars and in 12 years the result would be 16X. For comparison purposes, at 5% per year your assets would only be 1.8X in 12 years and at 10% IRR 3.1X. While 25%+ IRR represents very high performance, I have been fortunate enough to consistently exceed it (but always am worried that it can’t keep up)! For my recommendations of the past 6 years, the IRR is 34.8% and since this exceeds 26%, the 6-year performance is roughly 6X rather than 4X.

What is the trick to achieving 25% plus IRR? Here are a few of my basic rules:

Start with companies growing revenue 20% or more, where those closer to 20% also have opportunity to expand income faster than revenue

Make sure the market they are attacking is large enough to support continued high growth for at least 5 years forward

Stay away from companies that don’t have profitability in sight as companies eventually should trade at a multiple of earnings.

Only choose companies with competitive advantages in their space

Re-evaluate your choices periodically but don’t be consumed by short term movement

As I go through each of my 6 stock picks I have also considered where the stock currently trades relative to its growth and other performance metrics. With that in mind, as is my tendency (and was stated in my last post), I am continuing to recommend Tesla, Facebook, Amazon, Stitch Fix and DocuSign. I am adding Zoom Video Communications (ZM) to the list. For Zoom and Amazon I will recommend a more complex transaction to achieve my target return.

2020 Stock Recommendations:

1. Tesla stock appreciation will continue to outperform the market (it closed last year at $418/share)

Tesla is likely to continue to be a volatile stock, but it has so many positives in front of it that I believe it wise to continue to own it. The upward trend in units and revenue should be strong in 2020 because:

The model 3 continues to be one of the most attractive cars on the market. Electric Car Reviews has come out with a report stating that Model 3 cost of ownership not only blows away the Audi AS but is also lower than a Toyota Camry! The analysis is that the 5-year cost of ownership of the Tesla is $0.46 per mile while the Audi AS comes in 70% higher at $0.80 per mile. While Audi being more expensive is no surprise, what is shocking is how much more expensive it is. The report also determined that Toyota Camry has a higher cost as well ($0.49/mile)! Given the fact that the Tesla is a luxury vehicle and the Camry is far from that, why would anyone with this knowledge decide to buy a low-end car like a Camry over a Model 3 when the Camry costs more to own? What gets the Tesla to a lower cost than the Camry is much lower fuel cost, virtually no maintenance cost and high resale value. While the Camry purchase price is lower, these factors more than make up for the initial price difference

China, the largest market for electronic vehicles, is about to take off in sales. With the new production facility in China going live, Tesla will be able to significantly increase production in 2020 and will benefit from the car no longer being subject to import duties in China.

European demand for Teslas is increasing dramatically. With its Chinese plant going live, Tesla will be able to partly meet European demand which could be as high as the U.S. in the future. The company is building another factory in Europe in anticipation. The earliest indicator of just how much market share Tesla can reach has occurred in Norway where electric cars receive numerous incentives. Tesla is now the best selling car in that country and demand for electric cars there now exceeds gas driven vehicles.

While 2020 is shaping up as a stairstep uptick in sales for Tesla given increased capacity and demand, various factors augur continued growth well beyond 2020. For example, Tesla is only partway towards having a full lineup of vehicles. In the future it will add:

Pickup trucks – where pre-orders and recent surveys indicate it will acquire 10-20% of that market

A lower priced SUV – at Model 3 type pricing this will be attacking a much larger market than the Model X

A sports car – early specifications indicate that it could rival Ferrari in performance but at pricing more like a Porsche

A refreshed version of the Model S

A semi – where the lower cost of fuel and maintenance could mean strong market share.

2. Facebook stock appreciation will continue to outperform the market (it closed last year at $205/share)

Facebook, like Tesla, continues to have a great deal of controversy surrounding it and therefore may sometimes have price drops that its financial metrics do not warrant. This was the case in 2018 when the stock dropped 28% in value during that year. While 2019 partly recovered from what I believe was an excessive reaction, it’s important to note that the 2019 year-end price of $205/share was only 16% higher than at the end of 2017 while trailing revenue will have grown by about 75% in the 2-year period. The EPS run rate should be up in a similar way after a few quarters of lower earnings in early 2019. My point is that the stock remains at a low price given its metrics. I expect Q4 to be quite strong and believe 2020 will continue to show solid growth.

The Facebook platform is still increasing the number of active users, albeit by only about 5%-6%. Additionally, Facebook continues to increase inventory utilization and pricing. In fact, given what I anticipate will be added advertising spend due to the heated elections for president, senate seats, governorships etc., Facebook advertising inventory usage and rates could increase faster (see prediction 7 on election spending).

Facebook should also benefit by an acceleration of commerce and increased monetization of advertising on Instagram. Facebook started monetizing that platform in 2017 and Instagram revenue has been growing exponentially and is likely to close out 2019 at well over $10 billion. A wild card for growth is potential monetization of WhatsApp. That platform now has over 1.5 billion active users with over 300 million active every day. It appears close to beginning monetization.

The factors discussed could enable Facebook to continue to grow revenue at 20% – 30% annually for another 3-5 years making it a sound longer term investment.

3. DocuSign stock appreciation will continue to outperform the market (it closed last year at $74/share)

DocuSign is the runaway leader in e-signatures facilitating multiple parties signing documents in a secure, reliable way for board resolutions, mortgages, investment documents, etc. Being the early leader creates a network effect, as hundreds of millions of people are in the DocuSign e-signature database. The company has worked hard to expand its scope of usage for both enterprise and smaller companies by adding software for full life-cycle management of agreements. This includes the process of generating, redlining, and negotiating agreements in a multi-user environment, all under secure conditions. On the small business side, the DocuSign product is called DocuSign Negotiate and is integrated with Salesforce.

The company is a SaaS company with a stable revenue base of over 560,000 customers at the end of October, up well over 20% from a year earlier. Its strategy is one of land and expand with revenue from existing customers increasing each year leading to a roughly 40% year over year revenue increase in the most recent quarter (fiscal Q3). SaaS products account for over 95% of revenue with professional services providing the rest. As a SaaS company, gross margins are high at 79% (on a non-GAAP basis).

The company has now reached positive earnings on a non-GAAP basis of $0.11/share versus $0.00 a year ago. I use non-GAAP as GAAP financials distort actual results by creating extra cost on the P&L if the company’s stock appreciates. These costs are theoretic rather than real.

My only concern with this recommendation is that the stock has had a 72% runup in 2019 but given its growth, move to positive earnings and the fact that SaaS companies trade at higher multiples of revenue than others I still believe it can outperform this year.

4. Stitch Fix Stock appreciation will continue to outperform the market (it closed last year at $25.66/share)

Stitch Fix offers customers, who are primarily women, the ability to shop from home by sending them a box with several items selected based on sophisticated analysis of her profile and prior purchases. The customer pays a $20 “styling fee” for the box which can be applied towards purchasing anything in the box. The company is the strong leader in the space with revenue approaching a $2 billion run rate. Unlike many of the recent IPO companies, it has shown an ability to balance growth and earnings. The stock had a strong 2019 ending the year at $25.66 per share up 51% over the 2018 closing price. Despite this, our valuation methodology continues to show it to be substantially under valued and it remains one of my picks for 2020. The likely cause of what I believe is a low valuation is a fear of Amazon making it difficult for Stitch Fix to succeed. As the company gets larger this fear should recede helping the multiple to expand.

Stitch Fix continues to add higher-end brands and to increase its reach into men, plus sizes and kids. Its algorithms to personalize each box of clothes it ships keeps improving. Therefore, the company can spend less on acquiring new customers as it has increased its ability to get existing customers to spend more and come back more often. Stitch Fix can continue to grow its revenue from women in the U.S. with expansion opportunities in international markets over time. I believe the company can continue to grow by roughly 20% or more in 2020 and beyond.

Stitch Fix revenue growth (of over 21% in the latest reported quarter) comes from a combination of increasing the number of active clients by 17% to 3.4 million, coupled with driving higher revenue per active client. The company accomplished this while generating profits on a non-GAAP basis.

5. Amazon stock strategy will outpace the market (it closed last year at $1848/share).

Amazon shares increased by 23% last year while revenue in Q3 was up 24% year over year. This meant the stock performance mirrored revenue growth. Growth in the core commerce business has slowed but Amazon’s cloud and echo/Alexa businesses are strong enough to help the company maintain roughly 20% growth in 2020. The company continues to invest heavily in R&D with a push to create automated retail stores one of its latest initiatives. If that proves successful, Amazon can greatly expand its physical presence and potentially increase growth through the rollout of numerous brick and mortar locations. But at its current size, it will be difficult for the company to maintain over 20% revenue growth for many years (excluding acquisitions) so I am suggesting a more complex investment in this stock:

Buy X shares of the stock (or keep the ones you have)

Sell Amazon puts for the same number of shares with the puts expiring on January 15, 2021 and having a strike price of $1750. The most recent sale of these puts was for over $126

So, net out of pocket cost would be reduced to $1722

A 20% increase in the stock price (roughly Amazon’s growth rate) would mean 29% growth in value since the puts would expire worthless

If the stock declined 226 points the option sale would be a break-even. Any decline beyond that and you would lose additional dollars.

If the options still have a premium on December 31, I will measure their value on January 15, 2021 for the purposes of performance.

6. I’m adding Zoom Video Communications to the list but with an even more complex investment strategy (the stock is currently at $72.20)

I discussed Zoom Video Communications (ZM) in my post on June 24, 2019. In that post I described the reasons I liked Zoom for the long term:

Revenue retention of a cohort was about 140%

It acquires customers very efficiently with a payback period of 7 months as the host of a Zoom call invites various people to participate in the call and those who are not already Zoom users can be readily targeted by the company at little cost

Gross Margins are over 80% and could increase

The product has been rated best in class numerous times

Its compression technology (the key ingredient in making video high quality) appears to have a multi-year lead over the competition

Adding to those reasons it’s important to note that ZM is improving earnings and was slightly profitable in its most recent reported quarter

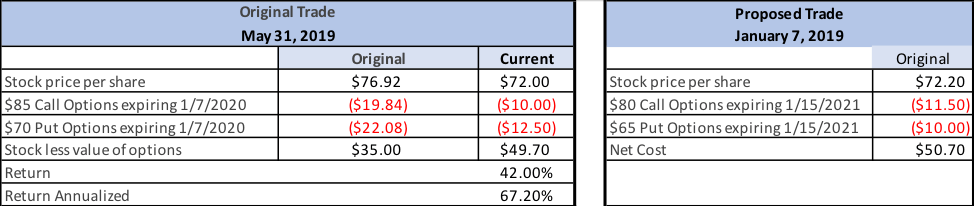

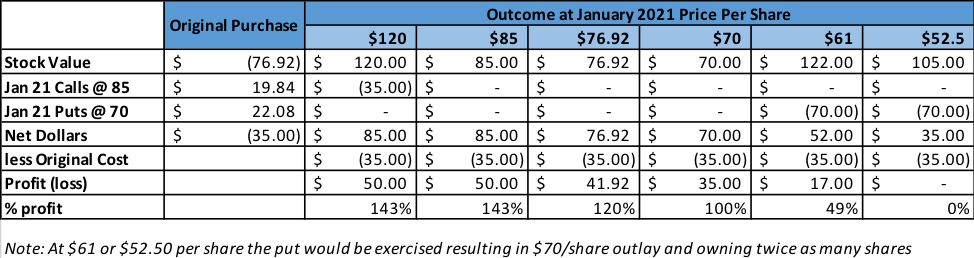

The fly in the ointment was that my valuation technology showed that it was overvalued. However, I came up with a way of “future pricing” the stock. Since I expected revenue to grow by about 150% over the next 7 quarters (at the time it was growing over 100% year over year) “future pricing” would make it an attractive stock. This was possible due to the extremely high premiums for options in the stock. So far that call is working out. Despite the company growing revenue in the 3 quarters subsequent to my post by over 57%, my concern about valuation has proven correct and the stock has declined from $76.92 to $72.20. If I closed out the position today by selling the stock and buying back the options (see Table 1) my return for less than 7.5 months would be a 42% profit. This has occurred despite the stock declining slightly due to shrinkage in the premiums.

Table 1: Previous Zoom trade and proposed trade

I typically prefer using longer term options for doing this type of trade as revenue growth of this magnitude should eventually cause the stock to rise, plus the premiums on options that are further out are much higher, reducing the risk profile, but I will construct this trade so that the options expire on January 15, 2021 to be able to evaluate it in one year. In measuring my performance we’ll use the closing stock price on the option expiration date, January 15, 2021 since premiums in options persist until their expiration date so the extra 2 weeks leads to better optimization of the trade.

So, here is the proposed trade (see table 1):

Buy X shares of the stock at $72.20 (today’s price)

Sell Calls for X shares expiring January 15, 2021 at a strike of $80/share for $11.50 (same as last price it traded)

Sell puts for X shares expiring January 15, 2021 with strike of $65/share for $10.00 (same as last price it traded)

I expect revenue growth of 60% or more 4 quarters out. I also expect the stock to rise some portion of that, as it is now closer to its value than when I did the earlier transaction on May 31, 2019. Check my prior post for further analysis on Zoom, but here are 3 cases that matter at December 31, 2020:

Stock closes over $80/share (up 11% or more) at end of the year: the profit would be 58% of the net cost of the transaction

This would happen because the stock would be called, and you would get $80/share

The put would expire worthless

Since you paid a net cost of $50.70, net profit would be $29.30

Stock closes flat at $72.20: your profit would be $21.50 (42%)

The put and the call would each expire worthless, so you would earn the original premiums you received when you sold them

The stock would be worth the same as what you paid

Stock closes at $57.85 on December 31: you would be at break even. If it closed lower, then losses would accumulate twice as quickly:

The put holder would require you to buy the stock at the put exercise price of $65, $7.15 more than it would be worth

The call would expire worthless

The original stock would have declined from $72.20 to $57.85, a loss of $14.35

The loss on the stock and put together would equal $21.50, the original premiums you received for those options

Outside of my stock picks, I always like to make a few non-stock predictions for the year ahead.

7. The major election year will cause a substantial increase in advertising dollars spent

According to Advertising Analytics political spending has grown an average of 27% per year since 2012. Both the rise of Super PACs and the launch of online donation tools such as ActBlue have substantially contributed to this growth. While much of the spend is targeted at TV, online platforms have seen an increasing share of the dollars, especially Facebook and Google. The spend is primarily in even years, as those are the ones with senate, house and gubernatorial races (except for minor exceptions). Of course, every 4th year this is boosted by the added spend from presidential candidates. The Wall Street Journal projects the 2020 amount will be about $9.9 billion…up nearly 60% from the 2016 election year. It should be noted that the forecast was prior to Bloomberg entering the race and if he remains a viable candidate an additional $2 billion or more could be added to this total.

The portion targeted at the digital world is projected to be about $2.8 billion or about 2.2% of total digital ad spending. Much of these dollars will likely go to Facebook and Google. This spend has a dual impact: first it adds to the revenue of each platform in a direct way, but secondly it can also cause the cost of advertising on those platforms to rise for others as well.

8.Automation of Retail will continue to gain momentum

This will happen in multiple ways, including:

More Brick & Mortar locations will offer some or all the SKUs in the store for online purchase through Kiosks (assisted by clerks/sales personnel). By doing this, merchants will be able to offer a larger variety of items, styles, sizes and colors than can be carried in any one outlet. In addition, the consolidation of inventory achieved in this manner will add efficiency to the business model. In the case of clothing, such stores will carry samples of items so the customer can try them on, partly to optimize fit but also to determine whether he or she likes the way it looks and feels on them. If one observes the massive use of Kiosks at airports it becomes obvious that they reduce the number of employees needed and can speed up checking in. One conclusion is this will be the wave of the future for multiple consumer-based industries.

Many more locations will begin incorporating technology to eliminate the number of employees needed in their stores. Amazon will likely be a leader in this, but others will also provide ways to reduce the cost of ordering, picking goods, checking out and receiving information while at the store.

9. The Warriors will come back strong in the 2020/21 season

Let me begin by saying that this prediction is not being made because I have been so humbled by my miss in the July post where I predicted that the Warriors could edge into the 2020 playoffs and then contend for a title if Klay returned in late February/early March. Rather, it is based on analysis of their opportunity for next season and also an attempt to add a little fun to my Top Ten List! The benefit of this season:

Klay and Curry are getting substantial time off after 5 seasons of heavy stress. They should be refreshed at the start of next season

Russell, assuming he doesn’t keep missing games with injuries, is learning the Warriors style of play

Because of the injuries to Klay, Curry, Looney, and to a lesser extent Green and Russell, several of the younger members of the team are getting experience at a much more rapid rate than would normally be possible and the Warriors are able to have more time to evaluate them as potential long-term assets

If the Warriors continue to lose at their current rate, they will be able to get a high draft choice for the first time since 2012 when they drafted Harrison Barnes with the 7th pick. Since then their highest pick has been between the 28th and 30th player chosen (30 is the lowest pick in the first round)

The Warriors will have more cap space available to sign a quality veteran

Andre Iguodala might re-sign with the team, and while this is not necessary for my prediction it would be great for him and for the team

The veterans should be hungry again after several years of almost being bored during the regular season

I am assuming the Warriors will be relatively healthy next season for this to occur.

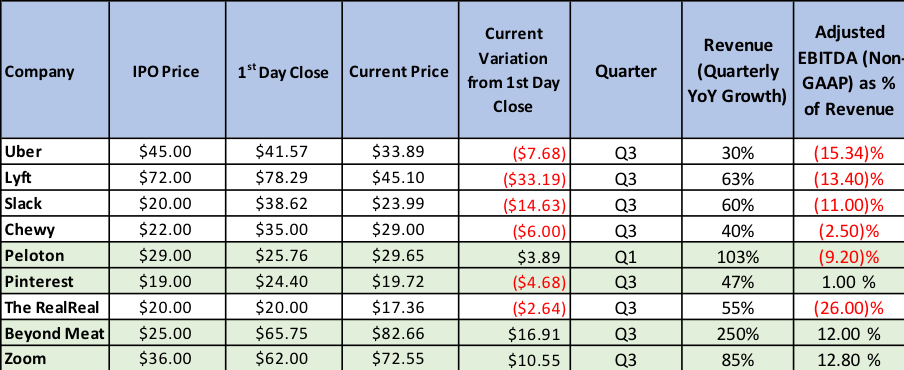

10. At least one of the major Unicorns will be acquired by a larger player

In 2019, there was a change to the investing environment where most companies that did not show a hint of potential profitability had difficulty maintaining their market price. This was particularly true of highly touted Unicorns, which mostly struggled to increase their share price dramatically from the price each closed on the day of their IPO. Table 2 shows the 9 Unicorns whose IPOs we highlighted in our last post. Other than Beyond Meat, Zoom and Pinterest, they all appear some distance from turning a proforma profit. Five of the other six are below their price on the first day’s close. A 6th, Peloton, is slightly above the IPO price (and further above the first days close). Beyond Meat grew revenue 250% in its latest quarter and moved to profitability as well. Its stock jumped on the first day and is even higher today. While Pinterest is showing an ability to be profitable it is still between the price of the IPO and its close on the first day of trading. Zoom, which is one of our recommended buys, was profitable (on a Non-GAAP basis) and grew revenue 85% in its most recent quarter. A 10th player, WeWork, had such substantial losses that it was unable to have a successful IPO.

Something that each of these companies have in common is that they are all growing revenue at 30% or more, are attacking large markets, and are either in the leadership position in that market or are one of two in such a position. Because of this I believe one or more of these (and comparable Unicorns) could be an interesting acquisition for a much larger company who is willing to help make them profitable. For such an acquirer their growth and leadership position could be quite attractive.

Apple’s progress from a company in trouble

to becoming the first company to reach a trillion dollar market cap meant over

400X appreciation in Apple stock. The metamorphosis began when the company

hired Fred Anderson as an Executive VP and CFO in 1996. Tim Cook joined the

company as senior VP of worldwide operations in 1998. Fred and Tim improved the

company operationally, eliminating wasteful spending that preceded their

tenure. Of course, as most of you undoubtedly know, bringing back Steve Jobs by

acquiring his company, NeXT Computer in early 1997 added a strategic genius and

great marketer to an Apple that now had an improved business model. Virtually

every successful current Apple product was conceived while Steve was there.

After Fred retired in 2004, Tim Cook assumed even more of a leadership role

than before and eventually became CEO shortly before Jobs’ death in 2011.

Apple post Steve Jobs

Tim Cook is a great operator. In the years

following the death of Steve Jobs he squeezed every bit of profit that is possible

out of the iPad, iPod, iMacs, music content, app store sales and most of all

the iPhone. Because great products have a long life cycle they can increase in

sales for many years before flattening out and then declining.

Table 1: Illustrative Sales Lifecycle for Great Tech Product

Cook’s limit is that he cannot

conceptualize new products in the way Steve Jobs did. After all, who, besides

an Elon Musk, could? The problem for Apple is that if it is to return to double

digit growth, it needs a really large, successful new product as the iPhone is

flattening in sales and the Apple Watch and other new initiatives have not sufficiently

moved the needle to offset it. Assuming Q4 revenue growth in FY 2019 is

consistent with the first 9 months, then Apple’s compound growth over the 4

years from FY 15 to FY 19 will be 3.0% (see Table 2) including the benefit of

acquisitions like Beats.

iPhone sales have flattened

The problem for Apple is that the iPhone is

now in the mature part of its sales life cycle. In fact, unit sales appear to

be declining (Graph 1) but Apple’s near monopoly pricing power has allowed it

to defy the typical price cycle for technology products where average selling

prices decline over time. The iPhone has gone from a price range of $99 to $299

in June 2009 to $999 to $1449 for the iPhoneX, while the older iPhone 7 is

still available with minimal storage for $449. That’s a 4.5X price increase at

the bottom and nearly 5X at the high end! This defies gravity for technology

products.

Graph 1: iPhone Unit Sales (2007-2018)

In the many years I followed the PC market,

it kept growing until reaching the following set of conditions (which the

iPhone now also faces):

Improvements in features were

no longer enough to drive rapid replacement cycles

Pricing was under pressure as

component costs declined and it became more difficult to convince buyers to add

capacity or capability sufficient to hold prices where they were

The number of first time users

available to buy product was no longer increasing each year

Competition from lower priced

suppliers created pricing pressure

Prior to that time PC pricing could be

maintained by convincing buyers that they needed one or more of:

The next generation of

processor

A larger or thinner screen

Next generation storage

technology

What is interesting when we contrast this

with iPhones is that PC manufacturers struggled to maintain average selling

prices (ASPs) until they finally began declining in the early 2000s. Similarly,

products like DVD players, VCRs, LCD TVs and almost every other technology

driven product had to drop dramatically in price to attract a mass market. In

contrast to that, Apple has been able to increase average prices at the same time that the iPhone became a mass

market product. This helped Apple postpone the inevitable revenue flattening

and subsequent decline due to lengthening replacement cycles and fewer first

time buyers. In the past few years, other then the bump in FY 2018 from the

launch of the high priced Model X early that fiscal year, iPhone revenue has

essentially been flat to down. Since it is well over 50% of Apple revenue, this

puts great pressure on overall revenue growth.

To get back to double digit growth Apple needs to enter a really large market

To be clear, Apple is likely to continue to

be a successful, highly profitable company for many years even if it does not

make any dramatic acquisitions. While its growth may be slow, its after tax

profits has been above 20% for each of the past 5 years. Strong cash flow has

enabled the company to buy back stock and to support increasing dividends every

year since August 2014.

Despite this, I think Apple would be well

served by using a portion of their cash to make an acquisition that enables

them to enter a very large market with a product that already has a great

brand, traction, and superior technology. This could protect them if the iPhone

enters the downside of its revenue generating cycle (and it is starting to feel

that will happen sometime in the next few years). Further, Apple would benefit

if the company they acquired had a visionary leader who could be the new “Steve

Jobs” for Apple.

There is no better opportunity than autos

If Apple laid out criteria for what sector

to target, they might want to:

Find a sector that is at least

hundreds of billions of dollars in size

Find a sector in the midst of major

transition

Find a sector where market

share is widely spread

Find a sector ripe for

disruption where the vast majority of participants are “old school”

The Automobile industry matches every criterion:

Matching 1. It is well over $3 trillion in size

Matching 2. Cars are transitioning to

electric from gas and are becoming the next technology platform

Matching 3. Eight players have between 5%

and 11% market share and 7 more between 2% and 5%

Matching 4. The top ten manufacturers all

started well over 50 years ago

And no better fit for Apple than Tesla

Tesla reminds me of Apple in the late

1990s. Its advocates are passionate about the company and its products. It can

charge a premium versus others because it has the best battery technology

coupled with the smartest software technology. The company also designs its

cars from the ground up, rather than retrofitting older models, focusing on

what the modern buyer would most want. Like Jobs was at Apple, Musk cares about

every detail of the product and insists on ease of use wherever possible. The

business model includes owning distribution outlets much like Apple Stores have

done for Apple. By owning the outlets, Tesla can control its brand image much

better than any other auto manufacturer. While there has been much chatter

about Google and Uber in terms of self-driving cars, Tesla is the furthest

along at putting product into the market to test this technology.

Tesla may have many advantages over others,

but it takes time to build up market share and the company is still around 0.5%

of the market (in units). It takes several years to bring a new model to market

and Tesla has yet to enter several categories. It also takes time and

considerable capital to build out efficient manufacturing capability and Tesla

has struggled to keep up with demand. But, the two directions that the market

is moving towards are all electric cars and smart, autonomous vehicles. Tesla

appears to have a multi-year lead in both. What this means is that with enough

capital and strong operational direction Tesla seems poised to gain significant

market share.

Apple could accelerate Tesla’s growth

If Apple acquired Tesla it could:

Supply capital to accelerate

launch of new models

Supply capital for more

factories

Increase distribution by

offering Tesla products in Apple Stores (this would be done virtually using

large computer screens). An extra benefit from this would be adding buzz to

Apple stores

Supply operational knowhow that

would increase Tesla efficiency

Add to the luster of the Tesla

brand by it being part of Apple

Integrate improved

entertainment product (and add subscriptions) into Tesla cars

These steps would likely drive continued

high growth for Tesla. If, with this type of support, it could get to 5% share

in 3-5 years that would put it around $200 billion in revenue which would be

higher than the iPhone is currently. Additionally, Elon Musk is possibly the

greatest innovator since Steve Jobs. As a result, Tesla would bring to Apple the

best battery technology, the strongest power storage technology, and the

leading solar energy company. More importantly, Apple would also gain a great

innovator.

The Cost of such an acquisition is well within Apple’s means

At the end of fiscal Q3, Apple had about

$95 billion in cash and equivalents plus another $116 billion in marketable

securities. It also has averaged over $50 billion in after tax profits annually

for the past 5 fiscal years (including the current one). Tesla market cap is

about $40 billion. I’m guessing Apple could potentially acquire it for less

than $60 billion (which would be a large premium over where it is trading).

This would be easy for Apple to afford and would create zero dilution for Apple

stockholders.

If the Fit is so strong and the means are there, why won’t it happen?

I can sum up the answer in one word – ego. I’m not sure Tim Cook is willing to admit that

Elon would be a far better strategist for Apple than him. I’m not sure he would

be willing to give Elon the role of guiding Apple on the product side. I’m not

sure Elon Musk is willing to admit he is not the operator that Tim Cook is

(remember Steve Jobs had to find out he needed the right operating/financial

partners by getting fired by Apple and essentially failing at NeXT). I’m not

sure Elon is willing to give up being the CEO and controlling decision-maker

for his companies.

So, this probably will never happen but if

it did, I believe it would be the greatest business powerhouse in history!

Soundbytes

USA Today just published a story that agreed with our last Soundbytes analysis of why Klay Thompson is underrated.

I expect Zoom Video to beat revenue estimates of $129 million to $130 million for the July Quarter by about $5 million or more

Applying Private Investment Analysis to the Rash of Mega-IPOs Occurring

The

first half of 2019 saw a steady stream of technology IPOs. First Lyft, then

Uber, then Zoom, all with different business models and revenue structures. As

an early investor in technology companies, I spend a lot of time evaluating

models for Venture Capital, but as a (recovering) investment analyst, I also

like to take a view around how to structure a probability weighted investment once

these companies have hit the public markets. The following post outlines a

recent approach that I took to manage the volatility and return in these growth

stocks.

Question: Which of the Recent technology IPOs Stands out as a Winning

Business Model?

Investing in Lyft and Uber, post IPO, had

little interest for me. On the positive side, Lyft revenue growth was 95% in Q1,

2019, but it had a negative contribution margin in 2018 and Q1 2019. Uber’s growth was a much lower 20% in Q1, but it

appears to have slightly better contribution margin than Lyft, possibly even as

high as 5%. I expect Uber and Lyft to improve their contribution margin, but it

is difficult to see either of them delivering a reasonable level of

profitability in the near term as scaling revenue does not help profitability

until contribution margin improves. Zoom Video, on the other hand, had

contribution margin of roughly 25% coupled with over 100% revenue growth. It also

seems on the verge of moving to profitability, especially if the company is

willing to lower its growth target a bit.

Zoom has a Strong Combination of Winning Attributes

There is certainly risk in Zoom but based

on the momentum we’re seeing in its usage (including an increasing number of

startups who use Zoom for video pitches to Azure), the company looks to be in

the midst of a multi-year escalation of revenue. Users have said that it is the

easiest product to work with and I believe the quality of its video is best in

class. The reasons for Zoom’s high growth include:

Revenue retention of a cohort is currently 140% – meaning that the same set of customers (including those who churn) spend 40% more a year later. While this growth is probably not sustainable over the long term, its subscription model, based on plans that increase with usage, could keep the retention at over 100% for several years.

It is very efficient in acquiring customers – with a payback period of 7 months, which is highly unusual for a SaaS software company. This is partly because of the viral nature of the product – the host of the Zoom call invites various people to participate (who may not be previous Zoom users). When you participate, you download Zoom software and are now in their network at no cost to Zoom. They then offer you a free service while attempting to upgrade you to paid.

Gross Margins (GMs) are Software GMs – about 82% and increasing, making the long-term model likely to be quite profitable

Currently the product has the reputation of being best in class (see here) for a comparison to Webex.

Zoom’s compression technology is well ahead of any competitor according to my friend Mark Leslie (a superb technologist and former CEO of Veritas).

The Fly in the Ointment: My Valuation Technique shows it to be Over

Valued

My valuation technique, published in one of our blog posts, provides a method of valuing companies based on revenue growth and gross margin. It helps parse which sub-scale companies are likely to be good investments before they reach the revenue levels needed to achieve long term profitability. For Zoom Video, the method shows that it is currently ahead of itself on valuation, but if it grows close to 100% (in the January quarter it was up 108%) this year it will catch up to the valuation suggested by my method. What this means is that the revenue multiple of the company is likely to compress over time.

Forward Pricing: Constructing a Way of Winning Big on Appreciation of

Even 10%

So instead of just buying the stock, I constructed

a complex transaction on May 29. Using it, I only required the stock to

appreciate 10% in 20 months for me to earn 140% on my investment. I essentially

“pre-bought” the stock for January 2021 (or will have the stock called at a

large profit). Here is what I did:

Bought shares of stock at $76.92

Sold the same number of shares of call options at $85 strike price for $19.84/share

Sold the same number of shares of put options at $70 strike for $22.08/share

Both sets of options expire in Jan 2021 (20 months)

Net out of pocket was $35/share

Given the momentum I think there is a high

probability (75% or so) that the revenue run rate in January 2021 (when options

mature) will be over 2.5x where it was in Q1 2019. If that is the case, it seems

unlikely that the stock would be at a lower price per share than the day I made

the purchase despite a potential for substantial contraction of Price/Revenue.

In January 2021, when the options expire, I will either own the same shares, or double the number of shares or I will have had my shares “called” at $85/share.

The possibilities are:

If the stock is $85 or more at the call date, the stock would be called, and my profit would be roughly 140% of the net $35 invested

If the stock is between $70 and $85, I would net $42 from the options expiring worthless plus or minus the change in value from my purchase price of $76.92. The gain would exceed 100%

If the stock is below $70, I’ll own 2x shares at an average price of $52.50/share – which should be a reasonably good price to be at 20 months out.

Of course, the options can be repurchased, and new options sold during the time period resulting in different outcomes.

Break-Even Point for the Transaction Is a 32% Decline in Zoom Video Stock

Price

Portfolio Managers that are “Value

Oriented” will undoubtedly have a problem with this, but I view this

transaction as the equivalent of a value stock purchase (of a high flyer) since

the break-even of $52/share should be a great buy in January 2021. Part of my

reasoning is the downside protection offered: where my being forced to honor

the put option would mean that in January 2021, I would own twice the number of

shares at an average price of $52.50/share. If I’m right about the likelihood

of 150% revenue growth during the period, it would mean price/revenue had

declined about 73% or more. Is there some flaw in my logic or are the premiums

on the options so high that the risk reward appears to favor this transaction?

I started writing this before Zoom reported

their April quarter earnings, which again showed over 100% revenue growth

year/year. As a result, the stock jumped and was about $100/share. I decided to

do a similar transaction where my upside is 130% of net dollars invested…but

that’s a story for another day.

Estimating the “Probabilistic” Return Using My Performance Estimates

Because I was uncomfortable with the

valuation, I created the transaction described above. I believe going almost 2

years out provides protection against volatility and lowers risk. This can

apply to other companies that are expected to grow at a high rate. As to my

guess at probabilities:

75% that revenue

run rate is 2.5x January 2019 (base) quarter in the quarter ending in January

2021. A 60% compound annual growth (CAG) for 2 years puts the revenue higher

(they grew over 100% in the January 2019 quarter to revenue of $105.8M)

95% that revenue

run rate is over 2.0X the base 2 years later (options expire in January of that

year). This requires revenue CAG of 42%. Given that the existing customer

revenue retention rate averaged 140% last year, this appears highly likely.

99% that revenue

is over 1.5X the base in the January 2021 quarter (requires slightly over 22% CAG)

1% that revenue is

less than 1.5X

Assuming the above is true, I believe that

when I did the initial transaction the probabilities for the stock were (they

are better today due to a strong April quarter):

50% that the stock

trades over 1.5X today by January 2021 (it is almost there today, but could hit

a speed bump)

80% that the stock

is over $85/share (up 10% from when I did the trade) in January 2021

10% that the stock

is between $70 and $85/share in January 2021

5% that the stock

is between $52 and $70 in January 2021

5% that the stock is

below $52

Obviously, probabilities are guesses since

they heavily depend on market sentiment, whereas my revenue estimates are more

solid as they are based upon analysis, I’m more comfortable with. Putting the

guesses on probability together this meant:

80% probability of

140% profit = 2.4X

10% probability of

100% profit = 2.0X

5% probability of

50% profit (this assumes the stock is in the middle at $61/share) = 1.5X

5% probability of

a loss assuming I don’t roll the options and don’t buy them back early. At

$35/share, loss would be 100% = (1.0X)

If I’m right on these estimates, then the

weighted probability is 120% profit. I’ve been doing something similar with Amazon

for almost 2 years and have had great results to date. I also did part of my DocuSign

buy this way in early January. Since then, the stock is up 27% and my trade is

ahead over 50%. Clearly if DocuSign (or Amazon or Zoom) stock runs I won’t make

the same money as a straight stock purchase would yield given that I’m capped

out on those DocuSign shares at slightly under 100% profit, but the trade also

provides substantial downside protection.

Conclusion: Investing in Newly Minted IPOs of High Growth Companies with

Solid Contribution Margins Can be Done in a “Value Oriented” Way

When deciding whether to invest in a

company that IPOs, first consider the business model:

Are they growing at a high rate

of at least 30%?

Experiencing increasing

contribution margins already at 20% or more?

Is there visibility to profitability

without a landscape change?

Next, try to get the stock on the IPO if

possible. If you can’t, is there a way of pseudo buying it at a lower price? The

transaction I constructed may be to complex for you to try and carries the

additional risk that you might wind up owning twice the number of shares. If

you decide to do it make sure you are comfortable with the potential future

cash outlay.