I promised a new post within 3 weeks of the last one. It’s here…but is different than originally planned! Several recent M&A events have motivated me to try to explain some basics on what happens to associated stocks in such a situation, the most recent being the Zoom acquisition of Five9. If the acquisition is a stock for stock transaction (as the Zoom one is), the acquirors stock will usually decline in price right after the announcement of the deal. The reason for the inevitable next day decline of the acquirer’s stock can be misunderstood. In this post I will explain why the decline has little to do with investors reaction to the quality of the acquisition.

What happens when a stock for stock acquisition of a public company is announced?

When a public company offers to acquire another, it is quite usual for the offer to be at a premium to the current stock price of the target company. Without a premium there is little motivation for the target company to accept the offer, and it can create a legal issue – as class action attorneys are vigilant to find opportunities to sue and can claim that the target sold out too “cheaply”.

Assuming the number of shares involved is a material amount, then once the deal is made public, the stock of the acquirer will almost always decline the next day while the target’s price rises. The press often interprets this as “The Street” being negative on the acquisition, when in fact it has little to do with a critique of the deal. Instead, it stems from “Risk Arbitrage” where arbitragers will short the acquirer’s stock and buy the target’s stock to create a certain profit if the acquisition is consummated. To illustrate this, I will use an easy-to-understand example:

Suppose Company A is trading at $100/share and then offers to acquire Company B (trading at $60/share). Suppose the offer is one share of Company A stock for each share of Company B stock. At these prices an arbitrager can:

- Buy Company B stock at $60/share – this equates to buying Company A stock at a discount if and when the deal closes since each share of B will then convert to one share of A

- Short Company A stock and receive $100/share

The net result is a gain of $40/share assuming the deal consummates. This occurs because when the share of B is converted to a share of A it can be used to cover the short position without the arbitrager spending any money. The Arbitrager will continue to do this as long as there is a gap between the prices of the shares. Given the number of shares being sold, A’s stock price will usually fall (the next day) and B’s will rise until it is virtually equal to A’s price on an as converted basis. The difference once this reaches equilibrium is the “risk premium”.

The reason it’s called “Risk Arbitrage” is that if the deal falls apart money could be lost. Therefore, a smart arbitrager will assign a risk premium based on his or her assessment of the probability that the deal will break. Once the 2 stocks are in sync, they will continue to trade in sync with the difference in prices being the risk premium. This will probably mean that the acquirer’s stock will return to around its prior price a few days later plus or minus its normal fluctuation, and the premium or discount assigned by investors to the deal.

Using Zoom Acquisition of Five9 as a Real Example

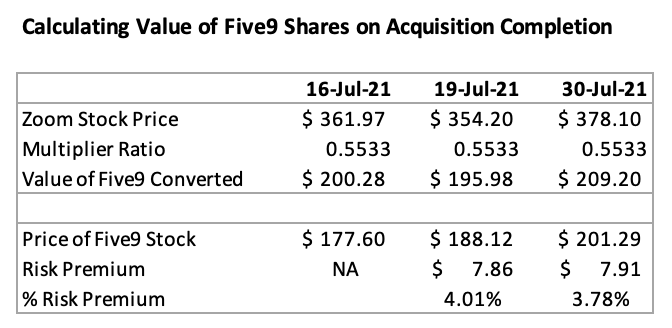

For an actual example, lets review the Zoom acquisition of Five9 announced on Sunday July 18, 2021. The agreement was to exchange each share of Five9 for 0.5533 shares of Zoom. At the close of the market on Friday, July 16 (just before the announcement):

- Zoom shares were at $361.97 and Five9 shares were at $177.60

- The theoretic value of a Five9 share based on 0.5533 of a Zoom share was $200.28 a 13% premium to the July 16 Five9 share price.

By the close on Monday July 19, Zoom shares had declined to $354.20 and Five9 shares had increased in price to $188.12. I saw many articles interpreting the Zoom drop in price as investors being negative on the deal. However, I believe it was the result of the volume of Zoom stock shorted by arbitragers.

Since 0.5533 times the Zoom price of $354.20 is $195.98 there was still a discrepancy in the ratio between the two stocks versus the ultimate conversion multiple of 0.5533 since Five9 was trading at 4.01% lower than the exchange ratio implied it was worth. This meant that Arbitragers were initially assigning a 4.01% risk factor based on the odds the deal would close. Once the two stocks settled into the appropriate ratio they have traded in sync since (less the Risk Premium). The risk premium has declined slightly in the two weeks since the deal was announced as arbitragers began to assess a lower risk factor to the odds the deal would break.

This same pattern usually occurs each time a stock for stock transaction is announced. There is too much money to be made from the arbitrage if the two stocks don’t adjust based on the conversion ratio. Any time they get out of sync arbitragers will step in again. When they initiate a pair of transactions the combination of buying stock in the target and shorting stock in the acquirer generates an immediate profit in cash. In our example of Zoom if the stocks were still at the July 16 price a transaction could be:

- Buy 10,000 shares of Five9 at $177.60 at a cost of $1,776,000

- These shares would convert to 5,533 shares of Zoom when the acquisition closes

- Sell short 5,533 shares of Zoom at $361.97/share to receive $2,002,780

- Immediate cash to arbitrager = $2,002,780 – $1,776,000 = $226,780

- If and when the acquisition closes the arbitrager would net a profit of $226,780

- If the deal breaks there could be a loss as the Zoom share short would need to be covered and the Five9 shares sold. This is why there is a risk premium involved.

Of course, the July 16 prices disappeared quickly when the stocks opened on July 19 as the arbitragers begin to execute their transactions. But as long as the difference exceeded the risk premium, they continued to transact to realize an immediate cash return. Once equilibrium was reached arbitragers ceased transacting (unless the stocks were to get out of sync again).

Conclusion

If you own a stock making a major acquisition and its stock price drops the day after the transaction is announced, the drop is likely to be temporary. Of course, there are situations where investors actually are so negative towards the transaction that the acquirer stock does not recover, but the first day drop usually has little to do with that.