It’s been a while since I posted, so I’m going to try to get 2 new ones out over the next 30 days. This one will be a return to my favorite sports team: The Warriors (or simply “Dubs”). It addresses several topics that have been heavily discussed in the media:

- Should The Dubs trade Kuminga?

- Have the The Dubs have abandoned their “2-track timeline (2TT)”?

- Why did The Dubs trade Poole and others for Chris Paul?

- What are the chances that The Dubs will win the title this upcoming season?

Should The Dubs trade Kuminga: Why Suggested Kuminga Trades Don’t Make Sense

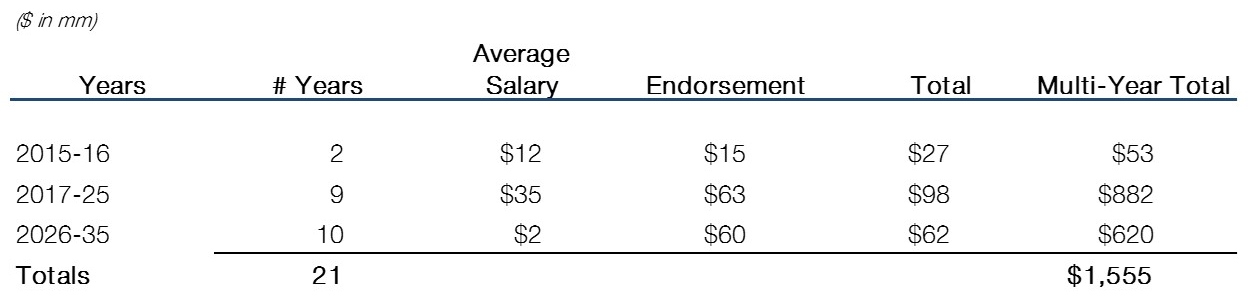

A number of suggested trades that include Kuminga (and often Chris Paul) have been suggested in the media. We regard all the ones we’ve seen as substantially sub-optimal. First, any suggested trade that includes Paul would likely prevent the team from getting to their financial target (of under the luxury tax second apron) in the 24-25 season. If they don’t get under that apron, they will be heavily restricted in signing free agents and in what types of trades they can do.

Kuminga has progressed substantially. He was especially good in the final part of last season and should be better this year. He appears on the road to being a star in the NBA. Most of the suggested trades were for players who have been in the league a lot longer, are on larger contracts that were not about to expire (defeating the Dubs ability to get under the second apron penalty level in 2024-25), or for players that I believe Kuminga is already as good as or better then. Given that he is still early in his career we believe that he is likely to significantly improve from here. The fact that Kerr barely played him in last year’s playoffs is the reason trades are being suggested. The “experts” who are suggesting them are ignoring how good he was defensively and offensively in the second half of last season. I think Kerr not using him in the playoffs was an error but motivated by the fact he is still very young, and Kerr wanted to add motivation for him to improve his rebounding.

All statistics from the Basketball Reference Guide

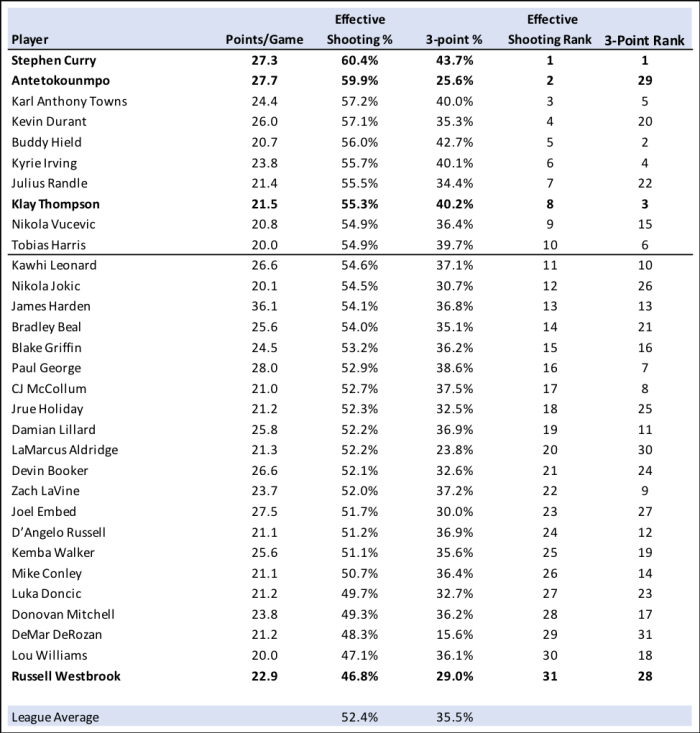

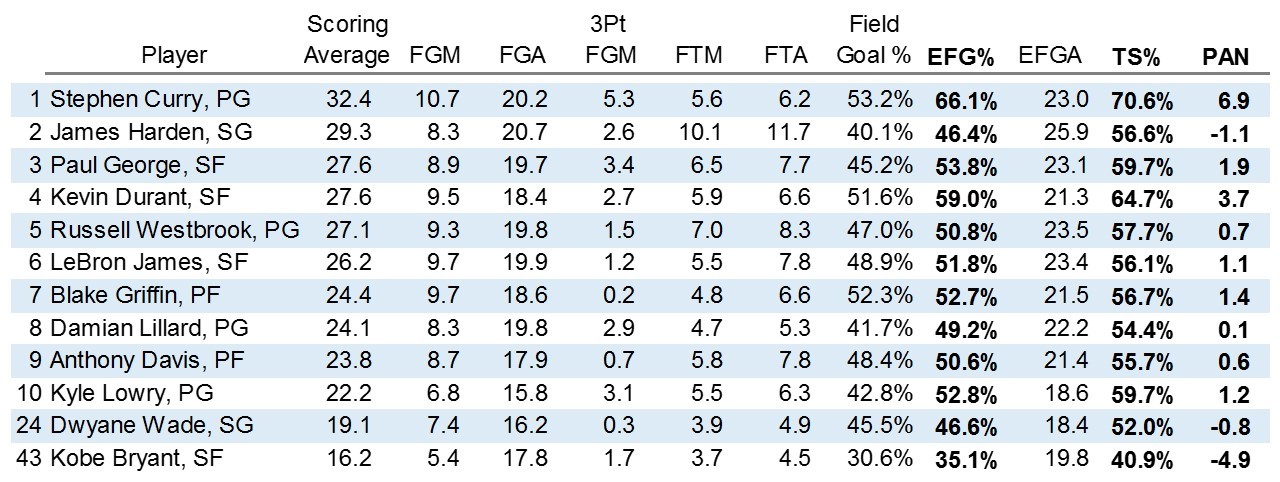

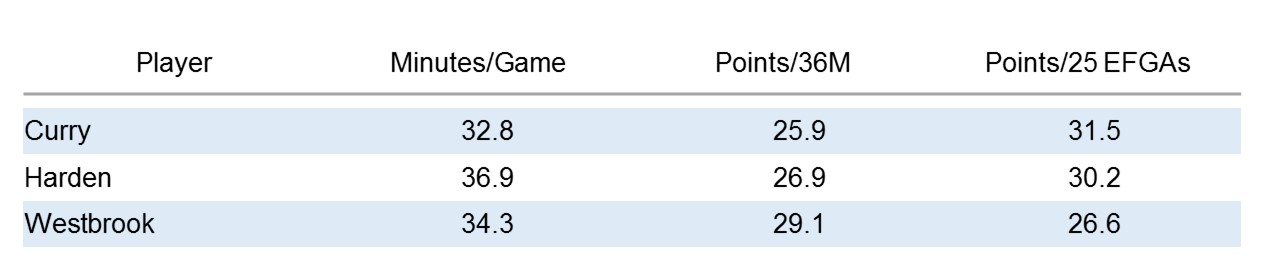

There are so many suggestions to trade Kuminga that it’s impossible to review them all. Instead, I’ll provide 2 typical examples to illustrate why they don’t make sense for the Warriors. One example is a proposed trade for Anunoby. Since Anunoby will make $12M more than Kuminga next season, the Warriors would also need to give up Moody and Payton (to match salaries). If they do that the cap rules would require signing minimum salary replacements who likely would be of lower quality than Moody and Payton, a major negative of such a trade. But even comparing Kuminga to Anunoby straight up is interesting. Since Anunoby played almost 36 minutes per game last year and Kuminga less than 21, the fairest comparison is to use stats per 36 minutes. Assuming they played the same amount of time each game, Kuminga would have averaged more points, rebounds and assists than Anunoby despite being 6 years younger and only in his second season (whereas Anunoby was in his 6th ). Since most young players improve dramatically between their 2nd and 6th seasons, Kuminga likely has significantly more upside than Anunoby. Kuminga also had a higher effective field goal average, trailed Anunoby slightly in 3-point % for the season but shot a much higher 49% from 3 in his last 19 games (and increased his rebounds and overall shooting as well). The one area where Anunoby is currently better is on defense (he was named to the NBA’s second team All-Defensive Team last season). But Kuminga, while not yet at an All-NBA level, became an outstanding defensive player in the latter part of last season. The statistics show that Kuminga is already a more efficient scorer, a better rebounder and better passer. Since Anunoby is ahead as a defensive player, they appear pretty equal already with Kuminga likely to surpass Anunoby this season or next.

A second example is a proposed trade for Thybulle. The suggestion includes the Warriors also giving up Cory Joseph and Tryce Jackson-Davis plus the teams swapping first round picks in 2029. The swap is so far out that it is hard to tell who would benefit so I think of it as the Warriors giving up Kuminga plus some extra for Thybulle. While Thybulle is a very strong defensive presence, that is a minor plus since Kuminga is already very strong defensively and should improve. On offense there is no comparison. Kuminga scores over 90% more points per 36 minutes, garners 30% more rebounds, generates over 75% more assists and maintains a higher shooting %. Combine this with a lower salary and how much better Kuminga was in the latter part of last season, this suggestion seems ludicrous as are most others that have been made by so-called “experts”.

I have used these examples as they typify how under-valued Kuminga is in speculated trades. That does not mean the Warriors would never trade him but at this point in time it seems to me to be extremely unlikely as he represents a high-quality player with unlimited potential at a low salary cost for the next 2 years. I view Moody as another potentially high-quality player (at a low cost) with strong upside but probably not quite as much upside potential as Kuminga. Unlike the beginning of last season, they both seem ready to emerge and become important cogs in a possible title run this year.

Have the The Dubs have abandoned their “2-track timeline (2TT)”: Two Track Timeline Very Much Alive!

Trading both Wiseman and Poole as well as several of last year’s rookie class has stirred a hornet’s nest of comments that the 2TT has been abandoned. We disagree and believe that it is still in play but modified to a more realistic timing for Track 2. Instead of thinking 8-10 years out, why not have:

Track 1 be the next 3 years (remainder of Curry contract).

Track 2 be the subsequent 3 years.

Let’s face it, even 6 years is a lifetime for the NBA as every one of the players below will have the opportunity to be a free agent within that period. And after 6 years all of them will have a second opportunity for free agency. So, trying to think beyond that is unrealistic as too many things can happen. With that in mind, here are the key players for track 2. Bear in mind this assumes everyone mentioned below will sign at least one new contract with the Warriors. Curry, Thompson, and Green will be 38, 36 and 36, respectively, at the start of the 2026-27 season. They are not included below but, of course, it’s somewhat likely that one or more of those 3 will still be a solid player that contributes to Track 2.

Track 2 – Potential Players from Current Roster (ages at beginning of 2026-27 season)

- Andrew Wiggins (31)

- Kevin Looney (30)

- Gary Payton II (33)

- Jonathan Kuminga (24)

- Moses Moody (24)

- Lester Quinones (25)

- Brandin Podziemski (23)

- Trayce Jackson-Davis (26)

- Gui Santos (24)

- Subsequent draft picks ?

Including Wiggins, Looney and Payton is quite realistic as they will all be in their peak years. In addition, the Dubs currently have 6 players that would be between 23 and 26 when we reach Track 2. Santos and Quinones are included because the high quality of their play in the G League indicates that they are currently better than last year’s rookies that were traded. But while both are under contract, neither is currently on the roster. Much has been made of the trades of Wiseman and Poole, but I believe that neither trade signifies abandoning the future as long as the Dubs keep Kuminga and Moody on the team. Wiseman was traded because he was a disappointment. Poole became a liability after signing a very rich 4-year contract a year ago (that would begin in the 2023-24 season) and then regressed significantly during last season.

In addition to improving the Track 1 team by trading Poole for Chris Paul (who is currently better), the Dubs also put themselves in a stronger position to acquire additional talent after the 2023-2024 season as they can get under the salary cap second apron in the 2024-25 season since Paul’s contract of $30M is not guaranteed for that year. The benefit of this is quite obvious when we consider the fact that the team might have kept DiVincenzo or signed a high-quality free agent if they had the flexibility that being under the second apron provides. Additionally, assuming several of the 6 players emerge as stars, the timetable for when they would need to be paid has a better spread than before since 4 of the 6 are rookies this year or next. The other 2, Moody and Kuminga, won’t be eligible for a contract extension until the 25-26 season giving the Warriors the opportunity for a cap reset in 24-25. When this is combined with the jump in cap expected in 2025 (due to a new TV contract) the Dubs can remain under the second apron in the 2025-26 season even if they need to substantially increase what they pay the two of them.

We are not suggesting that all 9 of these players will be on the team for Track 2 but rather that there is a strong potential available young core. While I firmly believe Kuminga and Moody can be stars this is not a given. If they fail to emerge then Track 2 may require the signing of a star free agent.

Why did The Dubs trade Poole and others for Chris Paul? We believe the Chris Paul for Poole trade was a positive for the Warriors this season.

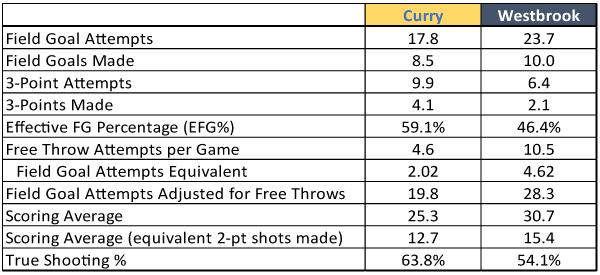

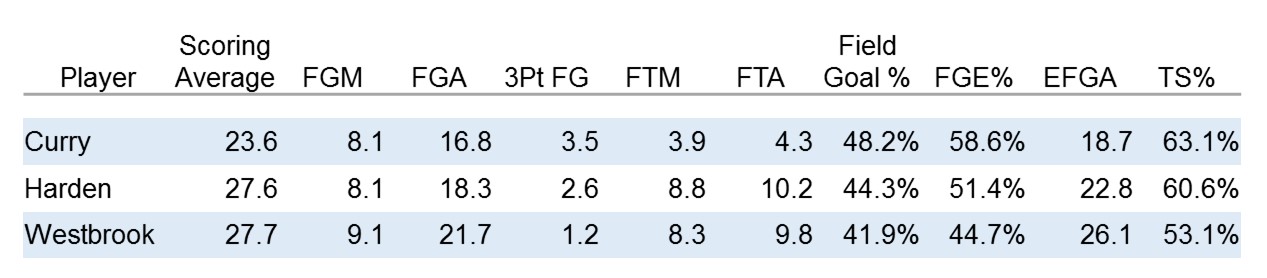

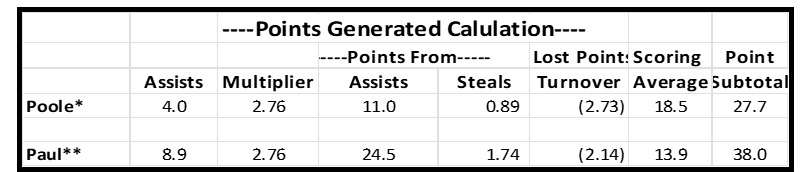

One way to compare the offensive value of each player is to compare Poole (in the 21-22 championship season) to Chris Paul last year using “net points generated” shown in the table below. It adds together the point value of assists and steals to the player’s scoring average and then subtracts the lost opportunity from turnovers to establish one overall number. While this will certainly be far from exact, using Chris Paul’s averages from last season in the comparison seems the best approximation of what he might do this season. We used the numbers from Poole in the championship season so we have a basis of comparison of the current team to the one that year, but it should be noted that while Poole scored more last season than the year before, it was due to taking more shots since his field goal efficiency declined (to below the league average) and he also had less rebounds and more turnovers last year.

In this past season, 38.5% of Dubs-made field goals were 3- point shots. That means an average field goal was worth 2.385 points. They also made .371 foul shots for every field goal made. Assuming passes generate .371 made foul shots for every assist that would mean an assist would generate an average total of 2.385 + .371 (2.756) points for the Warriors. The foul shots would come from passes where the recipient made the shot and was fouled plus those where the recipient missed the shot but was fouled. We believe the passer helped generate the foul shots in both cases and that there is a strong correlation between assists and passes that resulted in a missed assist because the recipient was fouled. We believe the points generated per assist are more valuable than unassisted field goals as it seems logical that an assist, on average would lead to a higher shooting percentage than unassisted shots and there would be more frequent times that no assist was recorded because the player was fouled.

*Poole stats for the 21-22 championship season **Paul stats for 22-23 season. Base Data from Basketball Reference guide

In this past season the Warriors averaged 118.94 points per game and had about 105.6 possessions per game. This means they score 1.126 points per possession. If we assume a steal generates an average possession, then each steal would be worth 1.126 extra points to a team (we think it actually generates more than 1.126 points as many steals lead to uncontested shots – a higher number favors Paul). Using this value in points per steal provides the points from steals in the above table. Finally, every turnover takes away a possession from your team. So, using the same logic the above table subtracts the point value of those lost possessions. Summing the numbers shows that Chris Paul generated over 10 more points per game last year than Jordan Poole did in the championship year.

Paul shot a higher percentage from 3-point range and is a better defender than Poole. The main advantage Poole has over him is his explosive ability to get by defenders resulting in a higher 2-point field goal percentage. This analysis shows that Paul generates over 10 more points of offense than Poole per game. Even if that number turns out to be off by half when he joins the Warriors, the extra 5 points should mean a lot more wins! To me, it seems clear that the Dubs will be a better team with Paul this coming season. The risk to the trade is that Poole has a lot of talent and if he improves his defense and becomes more disciplined on offense, he could become a star in the future whereas Chris Paul is at the tail end of his career.

Can The Warriors make a Title run?

Let me start by saying this Warriors team appears better than the 21-22 title team. Comparing:

- Klay was finding his legs when he returned mid-season in 21-22 from a 2 ½ year absence.

- Kuminga and Moody were rookies, and they are both significantly better now.

- Gary Payton II was just emerging, and the team had to learn how to maximize his value.

- Kevin Looney is better now than he was in the Championship season and Kerr also is better at how to use him.

- Wiggins missed a major part of last season but is reaching the peak years of his career. He should be as good or better than the 21-22 season on both offense and defense.

- In the championship year, Jordan Poole was excellent on offense but was quite weak on defense and had a lot of turnovers.

- This season Chris Paul will replace Poole and will likely generate more points of offense due to his assists, steals, rebounds, and fewer turnovers. Despite his no longer being at his peak on defense he still should provide better defense than Poole.

- A key player in 21-22 was Otto Porter Jr. I believe Saric is as good.

- While other role players matter, they will get little court time in the playoffs, so if Curry and Green are as good this coming season as they were in the championship year then the Warriors will be much better. Last season Curry and Green were both better than the 2021-22 season. Curry scored more, had a higher 2-point and 3-point shooting percent, garnered more rebounds, and had roughly the same average number of assists per game. He also was a better defensive player than the year earlier. Last year, Green improved his scoring, had higher 2-point and 3-point shooting percentages and almost the same rebounds and assists per game while finishing 4th in the voting for Defensive player of the year.

Putting the above together leads me to believe the Warriors are better equipped to win the championship than in the 21-22 season. However, the competition is stronger this coming season than in the 21-22 season.

In the West:

- Denver was missing Jamal Murray in 21-22 but had him back last year when they won.

- Arizona now has Durant and Beale, 2 great players to go along with Booker and Ayton.

- The Lakers added Gabe Vincent and Cam Reddish to a solid roster.

In the East:

- The Celtics added Porzingis but gave up Smart – still probably makes them better.

- The Bucks added Malik Beasley and Robin Lopez plus kept every one of their core 7 players.

Sacramento is a young team on the rise and could also contend. If the competition had not improved, I’d be picking the Warriors outright to win this year. Even with improved competition, I believe the Warriors can win this year (I didn’t think so last year) but they will need to be healthy come playoffs and playing their best ball.

Soundbytes

Just a quick reminder that I will be posting again within 30 days. The topic will be a deep dive into electric vehicles with mostly an emphasis on Tesla and some thoughts on Rivian and Lucid.