Consumers have more money available to spend – not less

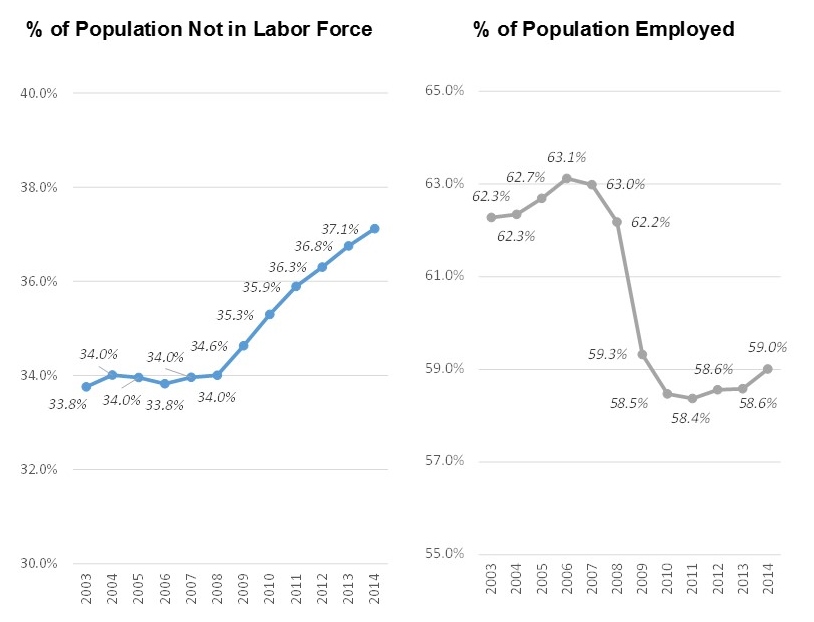

Much of the public dialogue concerning the economic effect of Covid19 has centered around the large number of people who have lost income, with the conclusion that the US will potentially experience a continued recession going forward. What seems to be lost in the discussion is that the 90% of the labor force that is employed is saving money at an unprecedented rate. This has occurred partly through fear of future loss of income but mostly by a reduction in spending caused by the virus. For myself and my family, our spending has been involuntarily reduced in the following areas:

- Personal care: haircuts, beauty parlor, nail treatments, massages, etc.

- Cleaning services: we are wearing very casual clothes that get washed instead of going to the cleaner (who has mostly been unavailable anyway).

- Vacations: our last vacation was in December. We haven’t been on a plane since the pandemic started and cancelled two vacation trips.

- Purchasing clothes: I have bought some items online for future use (because they were at major discounts) but being at home means I don’t really need any new clothes.

- Restaurants: before the pandemic I was eating breakfast and lunch out every weekday at or near my office and my wife and I ate out lunch and dinner on weekends. Additionally, I normally have additional business dinners several times a month. Instead, we are ordering food in on weekends from local restaurants we wish to support, but the cost is much lower than when we ate at the restaurant. Many of the people we know haven’t even ordered in from a restaurant.

- Transportation: these expenses have been virtually eliminated as I am not commuting to my office, take no Ubers and rarely drive anywhere other than to pick up local takeout food.

- Entertainment: such expenses have been close to eliminated other than occasionally purchasing a movie for home consumption.

- Medical/Dental/Optical Services: In my case medical and dental expenses have remained the same but many others have seen them reduced as access to doctors and dentists has been curtailed.

The only expenses that have increased are paying for delivery of food instead of picking it up ourselves at a supermarket and our new Zoom subscription…but at $12/month that hardly counts. I believe my family is representative of the 90% of people who still have their jobs at no reduction of pay. In fact, according to Statista, the savings rate in March through June increased to an average of 22% versus 7.9% in 2019. Using this data, I estimate that by the end of August this amounted to approximately $1.2 trillion in above normal savings as compared to last year’s “normal” savings rate. Since stay at home is unlikely to end in many places by the end of August, this number is likely to grow.

Post Pandemic: will some areas of savings persist?

Survey data of companies indicates that there is likely to be an increase in the number of people who work from home once the pandemic ends A recent survey by Global Workplace Analytics estimates that the U.S. will see between 25-30% of the workforce working from home multiple days a week by the end of 2021, up from less than 5% who were working from home at least half-time or more before the pandemic. Since working from home will continue to offer some savings in spending this could add to the “pot” of available dollars to be redeployed. There also may be some people who remain reluctant to fly or go on a cruise. We don’t expect these incremental cost savings to be removed from commerce but rather to be redeployed.

What I believe will occur post-pandemic

While some people will take advantage of their lower cost during the pandemic to pad their savings, it seems likely to me that a substantial portion of the “above normal” accumulated savings will be spent. I believe that such spending will be divided between satisfying pent up demand for items like clothing and vacations and new demand for luxury items. The pent-up demand will start with numerous parties as people are able to once again have human contact, but it also is likely to consist of increased purchases of clothes, more visits to restaurants and rescheduling of missed vacations.

I think that some portion of these savings will also be used on furniture (and perhaps even full remodels), art, and increased purchases of luxury items. After all, people can easily feel they deserve a reward for all these months of suffering. It is apparent that many people are already adding to their online budgets for furniture, décor and art as Wayfair has seen a large spike in revenue. While Wayfair results may be due to increased marketing spend, Azure portfolio company Chairish, has also had a very large spike in revenue without such an increase in marketing.

Has the pandemic caused temporary changes in buying habits or merely accelerated trends that were already in place?

The pandemic caused a number of radical changes in behavior, including:

- Most people working from home and rarely, if ever, going to their office.

- The vast majority of people ordering almost everything online instead of visiting a store.

- Shifting to video calls with coworkers, friends and relatives as opposed to regular phone calls or face to face interactions.

- Working out at home instead of at a gym, where possible.

- Education moving to at home via Zoom.

These shifts favored eCommerce sites, delivery services, providers of video conferencing, home equipment providers, Telemedicine, web services providers, and many others. They devastated physical stores, especially large department stores, restaurants, local transportation services (like subway systems, busses, ride services), service providers like cleaners, beauty parlors, spas, and gyms, airlines, hotels, theaters and arenas, and sports leagues (including college sports). There was also a lesser negative secondary impact on the advertising and marketing sectors as companies with major demand losses curtailed their spend.

How Ya Gonna Keep ‘em Down on the Farm After They’ve Seen Paree?

This was a song in the aftermath of World War I highlighting the fact that farm boys, once experiencing a more sophisticated life and culture would find it hard to return to their old way of life. It could not be more appropriate for the current situation. The leap in how much nearly everyone in society is using eCommerce, video conferencing, schooling and working at home is accelerating trends that were already in place. In fact, for me:

- Phone calls to friends that used to be audio calls are often Zoom video calls;

- While my wife and I already were buying a great deal online, its now pretty much everything and when the pandemic ends our portion of purchases online will remain at an elevated level given the convenience and the availability of a larger choice of items

- While I already had a home gym, many others are now substituting this for a gym membership

- In the 25+ weeks I’ve been “sheltering in place” I visited my Menlo office for 2-3 hours on about 5 separate occasions. While I look forward to more in person meetings once we are back to normal, working at home is an option that I expect to continue to use with some frequency once the pandemic ends. I also believe that several Azure portfolio companies can reduce the number of in-person board meetings by alternating them with Zoom board meetings.

I honestly find it hard to believe that our society will not shift behavior in the same way as my wife, myself and companies in the Azure portfolio. After all, while most of us have suffered from lack of interaction with others, the pandemic has introduced many shifts that people find positive. With this, and keeping the larger available funds mentioned earlier in mind, here are some of my post pandemic predictions:

- Ecommerce share of the consumer wallet will be much higher than before Covid, but not as high as currently.

- Consumer spending for the near term will grow to a much larger amount than pre-pandemic days (by perhaps as much as 15-20%).

- Online Advertising Companies will have a banner year in 2021 as Ad spending resumes for industries that were impacted by Stay at Home. These include airlines, cruise lines, hotels, live events (sports, concerts, etc.), ticket sellers, physical retailers. As their spend resumes, players like Facebook, Google, Pinterest, Twitter and Snapchat will have elevated revenue versus comps from the depressed 2020 numbers.

- Video calls will INCREASE SHARE even compared to during the pandemic as the people who have experienced its benefits will find it hard to go back to plain audio, companies will see the economics of reducing travel by increasing the number of video meetings and about 25-30% of the workforce will continue to spend 2 or more days working at home. Additionally, companies will be more comfortable hiring IT staff in less expensive locations as they have seen the effectiveness of video vs in-person communication, and some colleges that previously only offered in-person education will augment their income by adding students that are taught remotely using video conferencing.

- Home remodels will have a renaissance from simply buying a new couch to completely redoing rooms or even the entire house.

- Suburban homes will increase in value (this appears to be already happening) as people value having outside space in case of a pandemic recurrence.

- Working from home will be at an elevated level vs pre-Covid but demand for office space will resume as workplaces will require more space per employee.

- More shopping malls will close as Big Box retailers close more stores (or in some cases cease to exist).

- The ability to sign and even notarize documents using the web will continue to see high growth in demand

- Vacations will resume, but for about a year or more there will be an increase in driving vacations

- More people than pre-Covid will take to wearing masks on a regular basis

- There will be a one year above normal bump in purchasing of luxury items like more expensive cars, expensive watches, new state of the art TVs

The Stock Market is already at Least Partly Discounting a Number of the Above Items

Many have been surprised at the resilience of the stock market during this crisis. It is important to remember that the Market discounts future results rather than past ones. So, I believe, many investors are looking at some of the above and factoring it into how to value stocks. The trickier issues involve stocks that have been beneficiaries of the pandemic but I’ll leave that for another time.

Soundbytes

- In our January post of the top ten for the year we included Zoom as a stock buy in 2 ways. One was to simply buy the stock and the other was to buy the stock and sell both calls and puts. By June 30 the stock was at $253.54 per share and the call options (with a strike price of $80) was at $175 per share. Since the option premium was down to sub $2, I would have bought back the stock and the call options as there was little benefit to letting them ride as the IRR could not increase. But since I didn’t publish that then we can just assume I did that on September 1 where the premium was down to about $0.50. I can also buy back the puts at $0.40. That would mean I initially spent a net of $50.70 and received back $79.10, 8 months later. This translates to an annualized IRR of about 100% (on June 30 it would have been over 120%). Make no mistake, if you bought the stock and did not sell calls, I would continue to hold it as I expect another very strong (above analyst consensus forecast) quarter in Q3 which will be reported in early December.